Position Journal@PositionJournal

As promised here's the $CRSR story.

The bull and bear cases and why I think Corsair is mispriced at $5 a share (0.4x P/S) and 600M market cap.

I hold about 2% of port in Corsair.

WHAT THEY DO

Corsair provides performance components, peripherals, and computing solutions across consumer, education, government and engineering/manufacturing segments.

Corsair splits its business into two segments: peripherals and components.

The peripherals segment covers everything a gamer or creator touches directly, including keyboards, mice, headsets, controllers, capture cards, Stream Decks, microphones, cameras, and sim racing gear.

This segment captures 33%, or $492M for FY25 total revenues.

The components segment covers the hardware inside and around the machine, including PSUs (power supply unit), cooling, cases, DRAM, prebuilt gaming PCs, laptops, and AI workstations.

This captures 67% of their total revenues, or $980M FY25 revenue.

Before we go further, let's address the elephant in the room. Corsair is down -83% in the last 5 years, from $33 to just $5 a share.

SO WHAT IN THE WORLD HAPPENED?

In short, they could not sustain a positive operating income.

FY22: -$55M loss

FY23: +$9.7M profit

FY24: -$50M loss

2023 saw strong demand for gaming following post-pandemic recovery and 2024 saw regression to the mean.

If you can't sustain net-positive operating income, then it signals operational weakness either due to execution or cyclical demand, and raises doubts about the company's long-term viability, signalling if this company will even exist in the future.

WHAT HAPPENED IN 2025?

Corsair achieved positive GAAP operating income of $2.1M, that's a +104% YoY swing to positive.

They achieved this through a combination of operational efficiency improvements, better inventory holding, improved supply chain management and aided by a tailwind of increasing demand by consumers.

Internally it's likely they cut down on bureaucracy, accelerated decision making, reduced weeks of cover for their inventory and held their vendors or logistics team to a higher bar.

Many reasons hide behind "operational efficiency" and "strategic inventory" which is why I don't like to focus on it if management themselves aren't clear about it.

But let's move on to something that management IS clear about:

Product innovation.

They launched over 100 products in 2025 including new PC cases, pre-built desktops, controllers, voice focus software and their Galleon 100 SD Keyboard with built-in stream deck.

This is a company that is focused on leading not with accounting gimmicks but with value added products.

But let's not butter them up completely and address some meaningful tailwinds that was out of Corsair's control, but benefited Corsair.

Demand is picking up again.

A critical component in gaming is GPUs, and the two biggest players, AMD and NVIDIA have confirmed that the gaming segment is ramping back up:

-AMD: "Gaming business revenue was $843 million, up 50% year-over-year, primarily driven by higher semi-custom revenue and strong demand for AMD Radeon GPUs."

-NVIDIA: "Gaming revenue $3.7 billion, up 47% YoY, driven by strong Blackwell demand"

Now that we know what happened in 2025, let's move on to

BULL CASE🐂

Gaming segment is cyclical, we see accelerated in demand and Corsair has both the branding, distribution and inventory to deliver the demand and maximize this cycle.

Additionally, from a product perspective, they want to shift the focus to the Elgato brands Stream Deck:

Thi La (CEO): "Stream Deck is a central component of our plan, evolving from a creator tool into a shared control layer across productivity, gaming and sim racing. The successful launch of our Galleon keyboard at CES 2026, one of the most awarded product launches in our history"

Stream deck has a broad appeal:

-Content creators and streamers (switch scenes, trigger sound effects, better overlays)

-Podcast and radio hosts

-Video editors

-Corporate presentors

They're trying to decouple themselves from the tight cyclical grasp of the gaming segment.

Additionally, they authorized a $50M stock repurchase program. Its first in history. If executed at today's prices would be almost 10% of their market cap. But unfortunately, this only gives about 1.5 years benefit since stock-based-compensation (SBC) was about 33M in 2025.

Further, they are guiding to $1.3 to $1.5B revenue and $100-115M adjusted EBITDA for 2026.

This translates to: -5% revenue YoY driven from global semiconductor shortages and +6.9% growth YoY from the midpoint $107M.

It's important to note that the +6.9% YoY growth comes at the backdrop of an already +84% improvement in adjusted EBITDA.

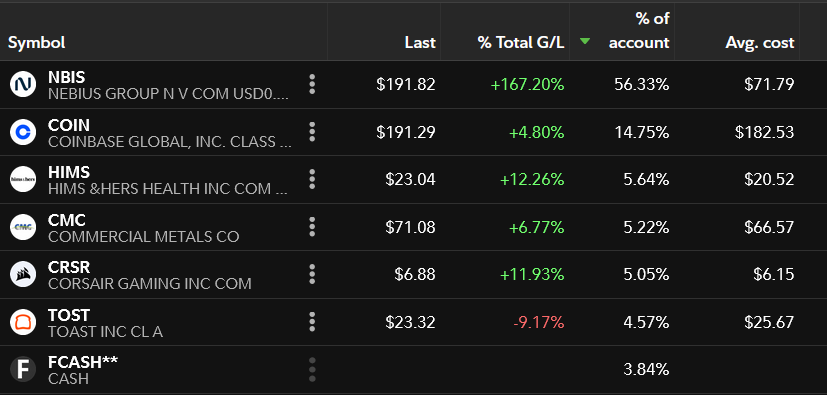

Finally, institutions are all making small bets on Corsair.

Top funds like DE Shaw, Millennium Management, State Street and Point72 Asset management and many others all either initiated new positions or bought millions in shares (see snip).

BEAR CASE 🐻

The reason why the market has not rotated into Corsair is because they are afraid this is simply a repeat of 2023.

2023 saw a positive operating income on the tailwind of high demand, and 2024 saw all that money evaporate and then some.

What if the same thing happens again?

It very well could.

I don't want to expand too much on other bear cases because just this one captures multitude of factors:

-Company value tied to cyclical demand

-Compressing margins due to competitions

-Lack of execution by management

-Being majorly controlled by EagleTree at 50% ownership

But ultimately, all of it is represented in the metric of operating income.

THE BOTTOM LINE

The company needs to prove itself. Operating income is fragile at just $2.1M, already guiding 2026 revenue lower and its unclear whether the shift of focus to D2C and non-gaming segments will work.

But this is a company that is STILL guiding to $1.4B revenue at a 600M market cap. They are priced to near bankruptcy and I fundamentally believe they are mispriced.

I do not think they will go bankrupt, and I do not think they will become innovators overnight. I think they will remain a household name with brand recognition that will carry them into new segments and I believe that because of that they will go higher.

Also, both La and Szteinbaum bought 50,000 and 100,000 shares in Nov 2025, so that helps my bottom line statement too 😉