High beta stocks create wealth.

But they also expose weak hands.

Most investors panic on the way down

and miss the move back up.

Here’s how much these need to gain just to reclaim their 52-week highs:

$HIMS +262.59%

$ROOT +272.55%

$DUOL +505.28%

$OSCR +64.71%

$LMND +83.47%

$SOFI +101.79%

$HOOD +121.25%

$IREN +95.48%

The upside is obvious.

The discipline isn’t.

@longinvest32 I have a question about Hems stock. Why is it continuing to decline despite the positive news? Is waiting now the solution, or should we sell?

99% of $HIMS investors are focused on the WRONG metrics:

They focus on:

- weekly app downloads

- website traffic on a daily basis

- analyst price targets

- short term growth

- insider "selling"

This is exactly how you lose.

HIMS IS NOT A “TELEHEALTH COMPANY”.

IT IS A DATA-DRIVEN HEALTHCARE NETWORK.

I’ve held $HIMS since $11.40.

Here’s why I believe the bear case is broken, and why this could be far bigger than people think

👇

Everyone thinks growth is collapsing.

They’re wrong.

Let’s break it down.

→ Claim 1: “Revenue growth is slowing, the business is breaking”

False.

Growth is not linear. It never was.

HIMS has always grown in cycles:

• Rapid expansion

• Temporary slowdown

• Re-acceleration

This is what many early businesses look like.

The recent slowdown has clear causes:

• GLP-1 headwinds

• Sexual health transition

• Compounding restrictions

• Revenue recognition changes

These are not structural problems.

Zoom out:

Revenue went from $18M to $617M (quarterly) in ~6 years.

That is execution.

→ The real question:

Can they keep launching and scaling new verticals?

So far, the answer is yes.

Historically: 1 launch per year.

Now: 3 launches in 90 days.

Speed is increasing.

That’s what matters.

→ Claim 2: “Marketing is too high, they’re buying growth”

Lazy take.

Yes, marketing is high.

But it is improving:

• From 50%+ → ~39% of revenue

• Payback < 1 year

• Efficiency trending up

This is not reckless spend.

And it makes sense.

Core categories like:

• Sexual health

• Hair loss

• Mental health

Require marketing due to stigma.

But here’s the shift:

New verticals like peptides and longevity are more organic.

Less paid acquisition.

More word of mouth.

Marketing dependency declines over time.

This is already happening.

→ Claim 3: “Subscriber growth is slowing, they’ve hit a ceiling”

Again, wrong diagnosis.

The slowdown is explained by:

• GLP-1 churn

• Sexual health transition to long-term plans

• Acquisitions not yet reflected (Zava, Eclipsis)

These distort the numbers.

They do not define the trajectory.

Zoom out again:

• ~500K → 2.5M+ subscribers in 6 years

The market is massive.

Penetration is tiny.

There is no ceiling here.

→ Claim 4: “Legal risk and management concerns”

Outdated.

• Novo lawsuit overturned

• Partnership strengthens credibility

• Strong regulatory bench

In fact, friction is expected.

They are challenging a $10T industry.

Resistance is part of the process.

→ Now zoom out.

What is actually happening here?

Healthcare is shifting from:

Reactive → Proactive

Generic → Personalized

Opaque → Data-driven

The old system:

• You get sick

• You see a doctor

• Trial and error treatment

The new system:

• Continuous data

• Early detection

• Personalized protocols

This is the real disruption.

→ The core problem in healthcare:

Lack of data.

Doctors don’t have real-time visibility.

Patients don’t understand their own biology.

So the system stays reactive.

That is changing.

Diagnostics are getting cheaper.

Data is becoming abundant.

And the value shifts to:

The platform that owns:

• The user relationship

• The data

• The entry point

That is where HIMS sits.

Top of funnel.

→ This is not about selling pills.

It is about building a healthcare network.

A system that:

• Acquires users

• Collects data

• Personalizes treatment

• Improves over time

AI will accelerate this.

But only if you already have:

• Distribution

• Data

• Feedback loops

HIMS is building all three.

→ The real moat

Not the drugs.

Not the UI.

Not the marketing.

It is the system.

• Millions of users

• Years of data

• Iteration across verticals

You can copy features.

You cannot copy accumulated healthcare data + distribution.

→ The market sees:

A telehealth app.

Reality:

An early-stage platform sitting at the center of a massive structural shift.

That gap is the opportunity.

→ The bet

This is not about the next quarter.

It is about:

Can they keep launching, scaling, and compounding new verticals?

So far:

They have done it repeatedly.

And they are getting faster.

→ The conclusion

Yes, growth has slowed.

Yes, there are risks.

But:

• The causes are explainable

• The model is improving

• The market is enormous

• The direction is clear

This is not a broken business.

It is a business in transition.

From:

Single-vertical telehealth

→ Multi-vertical healthcare platform

→ Final thought

The best investments look messy in the middle.

This is where doubt is highest.

This is where narratives break.

And this is where asymmetry lives.

$HIMS is not collapsing.

It is evolving.

And most people are missing the bigger picture.

بيت التمويل يعلن عن تطوير جديد في KFH Trade

بإتاحة التداول في السوق الأمريكي قبل الافتتاح وبعد الإغلاق إضافة إلى وقت السوق الرسمي.

لكن بصراحة:

أنا بشكل عام ما أنصح بالتداول خارج أوقات السوق،

لأن الحركة تكون أعنف، والسيولة أقل، وأحيانًا العمولة أعلى

حياك الله اخوي. انا احب سهم $HIMS الصراحة. العقد الجديد مع شركة $NVO جيد. لكنه ليس بالممتاز لاكون صريح معاك. لان هوامش الربح ستكون قليلة مقارنة بالسابق عندما كانت الشركة تبيع منتاجاتها الخاصة. هل السهم ممكن ان يصعد من المستويات الحالية برأيي اكيد ولكن يمكن للموضوع ان يطول حتى حدوث ذلك.

لا اعلم هل تملك سهم $IREN ام لا, لكني افضّله اكثر عن $HIMS. واعتقد خلال الفترة القليلة المقبلة سهم $IREN سيرتفع اكثر من $HIMS

Your point could be valid, but it’s not that simple.

Right now, the stock doesn’t have a clear trigger, and it already broke key levels (23.5).

High short interest doesn’t automatically mean upside — it needs a strong catalyst or a clear breakout to trigger a squeeze.

Without that, the stock could continue a normal correction, especially with margin pressure after the Novo deal.

In short:

This isn’t the time to underestimate shorts… nor to be overly optimistic.”**

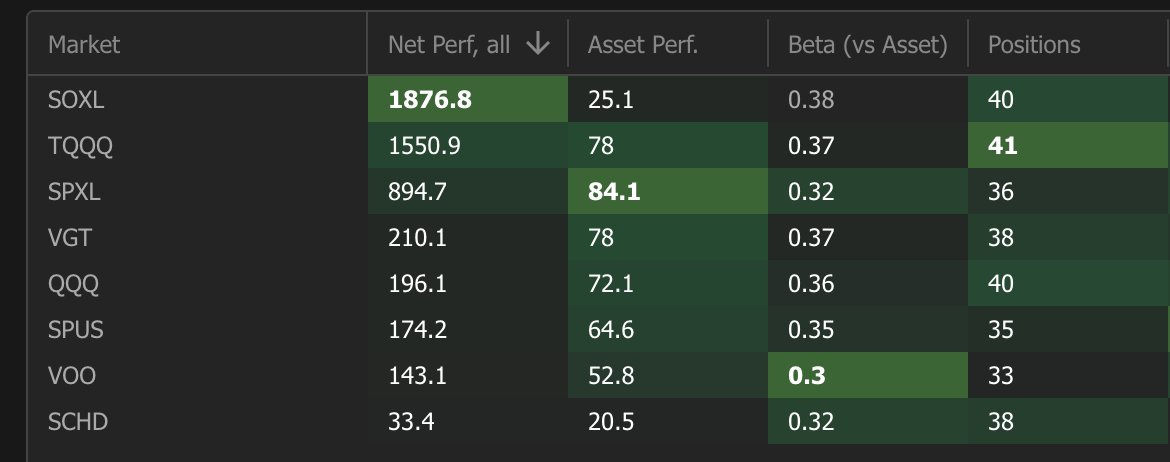

اداء الاستراتيجية القديمة التي كنت استخدمها سابقاً لآخر 4 سنوات مع تعديل بسيط عليها. الاداء خرافي!!

في الصورة أداء أهم الصناديق المعروفة في #السوق_الأمريكي

لا اعلم لماذا تركتها للأسف 😔. ان شاء الله انتظر فقط عودة ارتفاع سهم $IREN خلال الاشهر القليلة القادمة وسوف اعاود استخدام هذه الاستراتيجية من جديد!

ولكن سؤال مهم الان احد لديه فتوى يتيح لنا من خلالها تداول صندوق TQQQ 😅!! لان تداول مؤشر بهذا العائد حتى مع الرسومات لهذا الصندوق غير طبيعي!

$SOXL $TQQQ $SPXL $VGT $QQQ $SPUS $VOO $SCHD #الاسهم_الامريكية

وعليكم السلام اخي, سهم $HIMS ممتاز على المدى البعيد. بعد الاعلان الاخير بعد معارك مع شركة $NVO ثم التعاقد معاها يعتبر خبر ممتاز جداً. الشركة لديها خطط ممتازة للمستقبل وقد قلت ذلك كثيراً سابقاً. في ضل الضروف الحالية للسوق ممكن ان يبقى قليلاً عند مستوايته او حتى يرتفع بعض الشي. لكن اقرب خط عند 33 ثم 40. وممكن اخيراً ان يصل لارقام قياسية جديدة عند تعافي الاسواق وانتهاء الحرب ان شاء الله