Daniel

20.1K posts

Daniel

@danielisdizzy

Investments & market insights 📈 Daily updates + my portfolio growth 💸 YouTube 🎥 https://t.co/dUuKweywva

Katılım Mart 2024

345 Takip Edilen23.8K Takipçiler

Tom Lee expects the S&P 500 to hit 7,800 before a 10–15% correction.

He believes that pullback could set the stage for one of the most bullish 18–24 month stretches of our lifetimes.

Why does he expect the correction?

• Markets will be trying to price in the Fed’s next moves.

• The major $SPXC IPO lock-up expiration could create additional selling pressure.

• Growing shortages in petroleum products could become an inflation risk later this year.

His message is simple:

Expect volatility first.

Then potentially one of the strongest bull markets we’ve ever experienced.

English

@stocksandtax I’ll buy the ones that have fallen the most. Buying where sentiment is at its lowest is where wealth is created 💯

English

@danielisdizzy Corrections are where long-term investors are made.

If we got a 10–15% pullback, which stock would you be buying first?

English

@danielisdizzy AI infrastructure stocks are undervalued. If core players such as ORCL and CoreWeave can rebound, it will be good for the whole ecology. Do you think the demand for cloud computing power will continue to push up these stocks in the second half of the year?

English

Here’s how much these cloud providers need to rally just to reclaim their all-time highs:

• $ORCL: +146.5%

• $CRWV: +128.7%

• $IREN: +98.0%

Some of the companies that will be the biggest enablers of the AI revolution have been absolutely crushed.

Aside from a handful of semiconductor stocks that have gone parabolic, we’re nowhere near an AI bubble.

English

@aleabitoreddit The 800 MW $IREN secured in Australia won’t be energized until 2028 though.

Anthropic needs to move faster than that.

English

Leaked Anthropic docs show plans to secure 1.4GW capacity from Australia, amounting to ~$21.6B.

Recently $IREN, $SHAZ, and other Neoclouds have been building sovereign DCs in Australia.

Guess like a lot of things are stating to make more sense connection wise?

(disclosure: no open positions in any of the above).

English

@TheLongInvest Understanding that not every position is in the same cycle is game-changing

English

I sold $PLTR with +500% gains

Rotated it all into $HIMS and it ran from $11 to $72 but we trimmed between $50 -$60 (only trimmed)

And rotated all of that into $OSCR and then accumulated between $11-$13 which is now up +180%

We don’t use options or leverage so we focus on compounding

We need to get our rotations correct because of our approach

This only took 3 simple decisions to make us astronomical returns

Don’t tell me you can not do the same

I remember we decided to move our Cash out of a money market fund and transferred it into Silver at $24

We only expected to beat a mmf and we would have been happy

But instead that ran +300% in less than 2 years and we trimmed nearly half our position

4 decisions, life changing repercussions

Our main priority is always to eliminate as much risk as possible

Then rotate out of high risk to low risk

Technicals show us what’s stretched and also where to buy

Fundamentals tell us what to buy.

We teach this for everyone.

English

@danielisdizzy Solid take, Daniel! ORCL at the 200-week MA support (~60% off ATH) looks like a classic buy zone with that aggressive OCI ramp: $18B FY26 → $32B FY27 → $73B FY28 → $114B FY29 → $144B FY30.

English

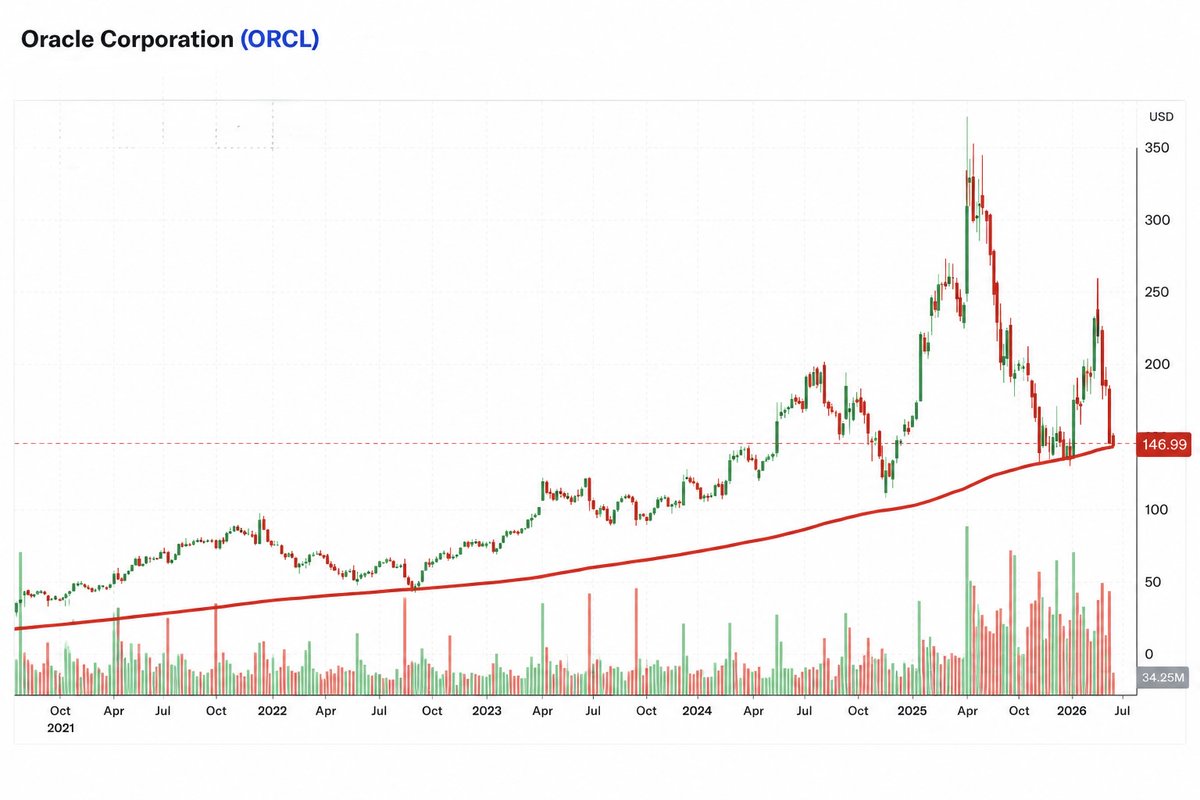

$ORCL is back at its 200-week moving average, a historically important support level.

Down 60% from its all-time high.

Meanwhile, Oracle expects OCI revenue to grow to:

• FY2026: $18B

• FY2027: $32B

• FY2028: $73B

• FY2029: $114B

• FY2030: $144B

Hard to ignore that setup.

Anyone buying $ORCL here?

English

@CryptoBankz_65 $TSLA needs to fall a lot further before it becomes interesting again

English

@danielisdizzy Never interested in any MAG 7 except $TSLA which I also don't own

English

@MMatters22596 I’m not ready to pull the trigger on $PLTR just yet.

But that moment will come

English

A list of my highest conviction stocks to hold for the long-term:

1. $NBIS

2. $CRDO

3. $ZETA

4. $OSCR

5. $CRWV

6. $SOFI

7. $RKLB

8. $PLTR

I am invested into all of these, and I have absolutely no doubt that every single one will outperform the market over the next three years.

Which are your's right now?

English

@oguzerkan If you simply buy solid stocks that have been beaten down instead of chasing stocks that have already had incredible runs, you’ll become a better investor than 99% of people

English

10 high-quality stocks trading near their lowest valuations:

1. $MSFT

- 5 Year Revenue CAGR: 12%

- Forward P/E: 19x

English

@TheMarketJarl And that’s exactly why I made this post.

The video was recorded before any agreement between $NVDA and $IREN

English

Jensen $NVDA:

“If we didn’t help $CRWV exist, they wouldn’t exist.

If we didn’t support $NBIS, they wouldn’t be where they are today.”

Now look at $IREN.

NVIDIA has already signed a $3.4B cloud services agreement with the company and holds an option to invest up to $2.1B.

This strategy makes perfect sense.

$AMZN, $MSFT, and $GOOGL are all investing heavily in their own custom AI chips to reduce their dependence on NVIDIA and capture more of the economics.

NVIDIA has every incentive to make sure the next generation of AI cloud providers becomes massive.

The goal isn’t for companies like $CRWV, $NBIS, and $IREN to simply rent compute to hyperscalers.

It’s to become AI infrastructure giants in their own right, competing for enterprise and developer workloads.

Being backed by the most valuable company in the world is not something investors should underestimate.

NVIDIA isn’t just selling GPUs.

It’s creating the next generation of AI cloud giants.

$CRWV $NBIS $IREN

English

@danielisdizzy Best bet is holding the two.

Both still have an incredible upside

Both $NBIS and $CRWV still have a long way to go but in all honesty, if you compare their EV/EBITDA, nebius is still a better bet most people will go for.

English

$NBIS is up 10% today while $CRWV is in the red.

YTD performance:

• $NBIS: +215%

• $CRWV: +33%

Current market cap:

• $NBIS: $65B

• $CRWV: $51B

Yet here’s where they stand:

• Backlog

$CRWV: $99.4B

$NBIS: ~$45B

• Expected end-2026 revenue run rate

$CRWV: $18–19B

$NBIS: $7–9B

• Expected connected power by end-2026

$CRWV: ~1.7 GW

$NBIS: 800MW–1GW

I’m not saying $CRWV has a better business than $NBIS.

I’m saying there’s no convincing case for it to trade at a lower market cap.

Yes, $CRWV carries more debt, but that alone doesn’t justify the valuation gap.

$NBIS has had an incredible run.

$CRWV hasn’t.

Buy the laggard.

English

@frombroke2bull $NBIS is my largest holding right now.

But the only neocloud companies I’m buying at current prices are $IREN and $CRWV 💯

English

@danielisdizzy I'm liking both $IREN and $CRWV here. Honestly, more than $NBIS.

To be fair, I missed my shot to buy Nebius in the 80s.

English

$MSFT IS CHEAPER THAN IT HAS BEEN IN A DECADE.

It needs to rally 51% just to reclaim its all-time high.

Yet it’s trading at its lowest forward P/E in the past 10 years: just 20x.

Azure and Copilot will make Microsoft one of the biggest winners of the AI era.

Most investors are chasing what’s already gone vertical.

The smarter trade is buying what the market is still underpricing.

$MSFT

English

@oguzerkan $MSFT today looks more and more like $GOOGL did in 2025

English

$MSFT

- Down 25% YTD

- Forward P/E is 19x

- Azure growing 40% YoY

At what point it becomes ridiculous?

English