Angehefteter Tweet

Saurav

3K posts

Saurav

@ThinkWithSaurav

The sector can be right. What matters is where inside it. Focus on what’s coming, not what’s visible. By the time attention arrives, the move is often over.

Before It Moves Beigetreten Ocak 2024

8 Folgt676 Follower

Yes, that’s the right way to look at it. But one year may still be early.

Execution will start showing in parts over the next 12–18 months, but the bigger impact comes when it moves into scale and integration, which is more 2026 onwards.

So near term, moves can come from order flow and initial execution visibility.

But the stronger re-rating will depend on

consistent execution → earnings visibility → then integration + maintenance layer

That’s when it becomes more sustainable, not just expectation driven.

So you’re on the right track, just think slightly longer in terms of the full cycle.

English

@ThinkWithSaurav @sunilgurjar01 Yes rightly said, execution and then integration as of advanced signaling. Holding few names from the list. Expecting good execution one year down the line.

English

🚄 Vande Bharat Mega Expansion: 4,500 Trains by 2047 – Railway Capex Supercycle Begins 🇮🇳

📌 Massive opportunity Railways & related sector stocks!

Bookmark & Repost

Stocks to Watch:🎯

1) Frontier Springs

2) Titagarh Rail Systems

3) BEML

4) Hitachi Energy India

5) Transformers & Rectifiers

6) Gabriel India

7) Jupiter Wagons

8) Ramkrishna Forgings

9) Rvnl

10) RailTel

11) HBL ENG

12) Kernex Microsystems

13) KEC International

14) Oriental Rail Infrastructure

15 ) Transrail Lighting

#stocks #investing

English

Of course you cannot expect 10x 20x from here. Cochin Shipyard at 35,000 plus crore Mcap today is not the same bet as Cochin Shipyard at 3,000 crore in 2020. That chapter is closed. You are right.

But, is the theme done. Or has only the first layer been discovered.

Understand how cycles actually work.

The market never discovers an entire theme at once. It discovers it layer by layer. With a 12 to 24 month gap between each layer.

Defence proved this perfectly.

2020 to 2022. HAL. BEL. Mazagon Dock. Platform manufacturers. Everyone said defence is done after that move.

2022 to 2024. Defence electronics. Astra Microwave. Data Patterns. Another significant move.

2024 onwards. Naval supply chain. Indigenous sonar. Electronic warfare. Intelligence inside the platforms. Still being discovered.

Same theme. Three layers. Three different timing windows. Three different sets of companies.

Now apply the same thinking to shipping.

Layer one. Freight rates. Great Eastern. Tanker companies. Already visible. Two quarter story. Partially priced.

Layer two. Ship repair and dry docks. Cochin Shipyard repair margins at 44 percent. GRSE repair growing 6x in three years. Mazagon Dock acquiring Colombo Dockyard. Starting to get discovered. Full move not happened yet.

Layer three. Component and systems suppliers feeding every repair and shipbuilding contract. Quest Flow Controls supplying valves to every GRSE vessel. Marine Electricals supplying electrical systems to 81 ships under construction. CFF Fluid Control making sonar for Scorpene submarines. Krishna Defence supplying structural steel to all major Indian shipyards. This layer has not been discovered yet. Mcaps small. Earnings just beginning to accelerate. No rerating has happened here.

The 10x 20x opportunity is not in layer one stocks that already moved. It is in layer three where Mcaps are small and the market has not connected the dots yet.

Quest Flow Controls. Revenue 67 crore. Defence marine doubled in one year. Directly correlated to every GRSE naval contract.

Krishna Defence. Revenue 194 crore up 83 percent. Targeting 500 crore in 3 to 4 years. Structural steel supplier to all major Indian shipyards.

Marine Electricals. Revenue 700 crore. 81 ships under construction. 99 more in planning. AMC recurring revenue running in parallel for every vessel supplied.

The rerating in large PSU shipyards is done. You are right about that. The rerating in the ecosystem feeding those shipyards has not started.

That sequence of discovery is 12 to 18 months away.

The cycle has not ended. It has just moved to the next layer.

The question is whether you are looking at the layer that already moved or the layer that is just beginning.

English

@ThinkWithSaurav But PE rerating has already happened....now you can't expect 10x 20x kind of returns in future also....your view please....

English

Before you think about the shipping sector understand this first. This will help you find the right stocks around it. If you are in that space.

Most people watching shipping right now are watching one number. Freight rates. Tankers at 400,000 dollars per day. Great Eastern's next quarterly result.

That is the right thing to watch for the next two months.

Here is what to watch for the next three years.

Every commercial vessel is legally required to enter dry dock at least twice every five years. Annual surveys. Intermediate surveys. Special survey every five years. Miss these and the ship cannot trade. Insurance lapses. Port entry denied.

This is not discretionary demand. Not dependent on freight rates. Not dependent on sentiment.

It happens. Every year. Every vessel. Without exception.

India's fleet alone generates roughly 500 mandatory dry docking events every year. Before counting a single foreign vessel. Before counting war driven repair surge. Before counting vessels stressed by longer Africa rerouting.

500 events. Structurally. Unavoidably. Regardless of what Nifty does.

Now here is the problem that creates the opportunity.

Over 30 percent of India's addressable repair work currently flows to Singapore, China, and UAE. Not because it is cheaper. Because it is faster and more reliable. India has dry docks but most are defence oriented and poorly equipped for fast turnaround commercial repair.

The gap is not demand. The gap is capacity and execution.

Now look at what is changing.

Cochin Shipyard. New 310 metre dry dock commissioned January 2024. MOU signed with Maersk February 2025. MOU with Drydocks World UAE. Master repair agreement with US Navy. Ship repair EBIT margin 44.2 percent. Shipbuilding margin 8%. Management guided 14 to 15% revenue growth FY26.

That margin difference tells you everything. Repair is 7 percent of their order book but generates margins five times higher than building new ships. Why? Because dry dock slots are the constraint. When slots fill up pricing power shifts completely to the yard. Ship owner cannot negotiate. Ship must dock.

Mazagon Dock. Plans to ramp repair revenue from 1,000 crore to 1,500 crore. Made their first ever international acquisition. Controlling stake in Colombo Dockyard for 53 million dollars. Management is telling you exactly where the next growth layer is.

Garden Reach Shipbuilders. Repair revenue grew from 19 crore in FY22 to 114 crore in FY25. Six times in three years. Management explicitly said they are shifting toward repair because margins are higher than shipbuilding.

Three public sector shipyards. All moving in the same direction. All saying the same thing in their management commentary. That convergence is the signal.

Now the war added urgency on top of a structural story that was already building.

Ships stressed from longer Africa routes. Maintenance deferred at 400,000 dollars per day. That deferred maintenance is now becoming mandatory. And it has to go somewhere.

The 30% leaking to Singapore and UAE is beginning to come home. Quarter by quarter. As new domestic capacity comes online.

Defence shipbuilding. Long cycle. 7 to 10 years per vessel. Slow revenue. Government pricing pressure. 8 percent margin.

Ship repair. Short cycle. Weeks not years. Fast cash collection. Commercial pricing. 44% margin.

Freight rate stories last two quarters. Everyone is watching them right now. Dry dock slot stories last three to five years. Almost nobody is watching them yet.

That gap between what everyone is watching and what is actually building is exactly where the next three years of returns come from.

Find the constraint. Own the constraint. Wait for the cycle to fill it.

English

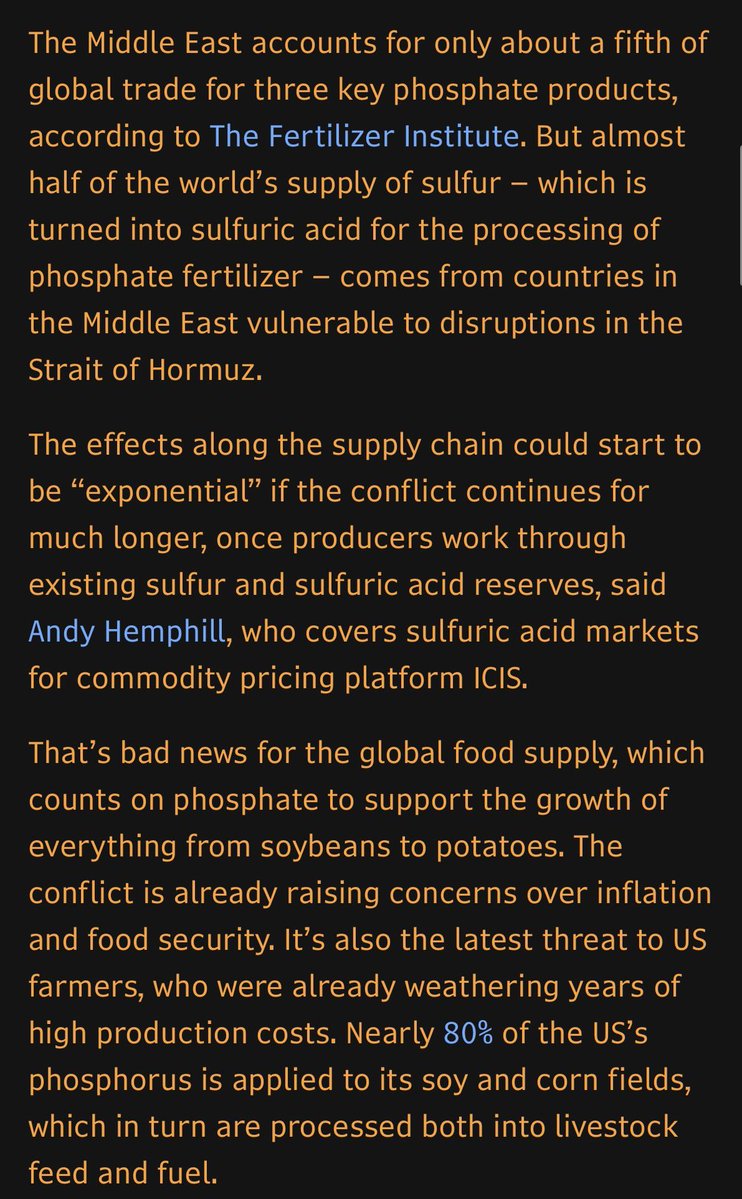

Why am I saying this is a good opportunity right now?

Because most people are looking at the fertilizer story at the surface level. Urea prices up. Plants cutting production. India running to China. That is the visible layer.

But there is a second layer almost nobody is connecting.

Look at this.

Almost half the world's sulfur supply comes from the Middle East. Sulfur becomes sulfuric acid. Sulfuric acid processes phosphate into DAP. DAP goes into the soil before every kharif crop.

No sulfur. No sulfuric acid. No DAP. No phosphate fertilizer.

The expert quoted here says effects along this supply chain could become exponential once existing reserves are worked through.

This is not a urea story anymore. This is a full fertilizer supply chain disruption working its way through layer by layer. Urea was layer one. Sulfur and phosphate is layer two and most people are still only reading about layer one.

India imports 50 to 60% of its DAP. Most sulfuric acid processing happens using imported sulfur from the same region the Strait runs through.

Now look at what two companies are quietly building right now while everyone else is watching urea prices.

Paradeep Phosphates expanded sulphuric acid capacity from 1.39 MMTPA to 2 MMTPA. Already commissioned October 2025. Before the war. Before the Strait closed. Before anyone was talking about sulfur supply chains.

Coromandel International building its own sulphuric acid and phosphoric acid plants at Kakinada. Commissioning Q4 FY26. Plants running above 100 percent capacity utilisation today. EBITDA per tonne guided to rise to 6,500 rupees once backward integration is complete.

Both companies are not just expanding capacity. They are building backward integration into the exact raw material layer that the Strait closure just made uncertain for every import dependent competitor.

Think about what that means in practical terms.

When sulfur reserves run low and sulfuric acid prices spike in the coming months the companies making their own sulfuric acid will have a cost structure their competitors simply cannot match. Every competitor importing sulfuric acid at elevated spot prices will see margins compress. Coromandel and Paradeep making their own will see margins expand. Same war. Same disruption. Opposite impact depending on which side of backward integration you sit on.

That divergence in margins is what the market has not priced yet.

The war did not just disrupt urea. It is working its way through the entire fertilizer supply chain layer by layer.

Urea was the first signal. Sulfur and phosphate is the second. By the time the market connects the full chain the companies that were already building the right things will have moved.

That is why this is a good opportunity right now.

Not because prices are spiking. Because the companies solving the structural problem were already building before anyone was watching.

Saurav@ThinkWithSaurav

The Strait closed. Three Indian urea plants cut production. Urea prices jumped 21% to a three year high. India quietly approached China asking them to lift export quotas before kharif season. China said no. 86% of the LNG India's fertilizer plants need comes from West Asia. Kharif season is 8 weeks away. More than 60 percent of India's agricultural output depends on fertilizer availability in June and July. Energy dependence hit your portfolio last month. Food dependence hits something more personal. But what most people are not connecting is that the same pressure that forced India to build its own batteries, its own defence equipment, its own solar panels is now forcing India to build its own fertilizer independence. Domestic backward integrated producers are gaining structural cost advantage right now while import dependent competitors struggle with elevated input costs. And the structural solution is already being built. Green ammonia made from Indian solar instead of Qatari LNG. SECI already auctioned 724,000 tonnes per year to 13 fertilizer plants. Ten year fixed contracts. First commercial plant commissioning 2028. From that year a portion of India's urea will be made from Indian sunshine. No Strait dependency. No Chinese permission required. The war did not create this opportunity. It just made it impossible to delay any longer.

English

Sir Ji, You are right on the cost gap. Green ammonia at $600 to $700 vs grey at 250 to 300 is real and anyone saying otherwise is not being honest.

But here is what changes that math.

1) The SECI ten year fixed price contracts are essentially government backed offtake agreements. The risk is not on the fertilizer plant. It is on the green ammonia producer. That structure exists precisely because the government knows price parity is not here yet and policy cover is needed to bridge the gap.

2) Grey ammonia at 250 to 300 dollars assumes stable LNG supply from Qatar. This month Indian plants were running at 70% capacity because that assumption broke. The real cost of grey ammonia dependence is not $250 to $300 per tonne. It is $250 to $300 per tonne plus the risk of your plant shutting down when a strait closes.

3) India's solar tariffs have fallen from 7 rupees per unit in 2015 to under 2 rupees per unit in recent auctions. The trajectory is still down. 2032 price parity is actually the conservative estimate not the optimistic one.

The policy cover requirement you flagged is exactly why this is an opportunity not a commodity trade. Companies that lock in ten year SECI contracts today are buying the right to be cost competitive in 2030 at prices that assume today's solar costs. That optionality is not priced yet.

Independence has a cost. But dependence just showed us it has one too.

English

@ThinkWithSaurav Thread nails the structural argument. Blind spot: green ammonia at $600-700/tonne vs grey at $250-300. SECI contracts work IF solar holds at ₹2.5/unit. Independence is coming but the cost gap needs policy cover for 5 years. Price parity 2032 at best.

English

The Strait closed. Three Indian urea plants cut production. Urea prices jumped 21% to a three year high. India quietly approached China asking them to lift export quotas before kharif season. China said no.

86% of the LNG India's fertilizer plants need comes from West Asia. Kharif season is 8 weeks away. More than 60 percent of India's agricultural output depends on fertilizer availability in June and July. Energy dependence hit your portfolio last month. Food dependence hits something more personal.

But what most people are not connecting is that the same pressure that forced India to build its own batteries, its own defence equipment, its own solar panels is now forcing India to build its own fertilizer independence. Domestic backward integrated producers are gaining structural cost advantage right now while import dependent competitors struggle with elevated input costs.

And the structural solution is already being built. Green ammonia made from Indian solar instead of Qatari LNG. SECI already auctioned 724,000 tonnes per year to 13 fertilizer plants. Ten year fixed contracts. First commercial plant commissioning 2028. From that year a portion of India's urea will be made from Indian sunshine. No Strait dependency. No Chinese permission required.

The war did not create this opportunity. It just made it impossible to delay any longer.

English

That’s actually a good place to be.

Before starting, it’s better to spend some time just observing and understanding how businesses and sectors work. Jumping in too early without clarity usually leads to mistakes.

You can start small when you begin, even with a limited amount, just to understand how markets behave in real time.

Along with that, keep studying one sector at a time. That combination of learning + small exposure helps build confidence much better than rushing in.

English

That’s a good start.

Don’t worry about going deep immediately. With Munger, even reading slowly and revisiting ideas works better than trying to finish fast.

Focus more on understanding the thinking — how he looks at decisions, risk, and long-term compounding. That part matters more than memorising concepts.

Over time, it will start connecting naturally with what you see in businesses and markets.

English

@ThinkWithSaurav Have just started reading Munger philosophy,,, that also very superficially,not started following.

English

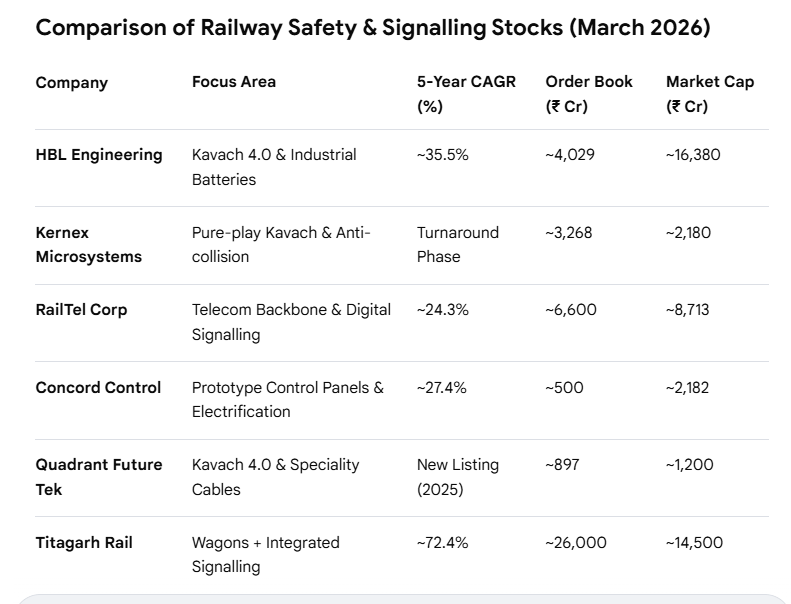

You’re right, safety and signalling is still weak and that’s exactly why the opportunity exists.

But you have to see it in phases, not as one straight story.

Right now, most of the space is already discovered at the announcement and expectation level. Budget increase, Kavach rollout plans, tenders — market has seen this, so some re-rating already happened on that basis.

The next phase is what matters.

Till around 2025–26, it’s more about tendering and initial execution — laying infra like OFC, towers, trackside systems, early deployments. Here, revenue visibility improves, but execution risk is still there.

From 2026 onwards, it shifts to scale + integration. Large network rollout, loco fitment, systems working together in real time. This is where companies that can actually execute and integrate will start showing stronger earnings.

After that, the real layer comes — maintenance, software, monitoring. Signalling is not one-time. It becomes a long-term system with upgrades and diagnostics. That’s where recurring revenue builds and stronger re-rating can happen.

So think like this:

First → re-rating on announcement (already happened)

Next → re-rating on execution and order flow

Then → re-rating on earnings + long-term contracts

And within this, value will shift from simple hardware to control systems, integration, and software layer.

So yes, opportunity is big, but now it’s not about just being in Kavach.

It’s about who can scale, integrate, and sustain over the full cycle.

English

@ThinkWithSaurav @sunilgurjar01 Saurav ji, how do you see companies in railway kavach and signaling ? We are very poor in railway safety n signaling. Railway has allocated huge budget for signaling and will keep increasing as its just the start.

English

@lohiarajesh Oh that’s a good book.

It explains patience and long-term thinking in a very simple way, which is actually the hardest part in markets. Also, the way it focuses on behavior and decision making, not just numbers, makes it very practical.

English

@ThinkWithSaurav Recently reading The Long Game by Vishal khandelwal

English

Rajesh ji, since you already follow Munger’s philosophy and watch those interviews, I would suggest reading in this order so it connects well with your current thinking:

1. Capital Returns – Edward Chancellor

Start with this. It fits very well with Munger-style thinking — capital allocation, cycles, and how industries move from excess to shortage. Very practical for equities.

2. Titan – Ron Chernow

Then this. It gives a real-world view of how businesses are built over decades, decisions under pressure, and capital deployment at scale.

3. The Prize – Daniel Yergin

Finally this for the bigger picture — history, geopolitics, and how industries shape economies. It helps connect everything together.

English

@ThinkWithSaurav Can you please suggest some books on investment, entrepreneurship.

I am a business man 58 Y, earlier fond of reading , Looking forward to invest in equities. Watch videos of Interviews of Manish Chokhani, Interviews taken by N Mahalaksmi , Munger philosophy

English

Rajesh ji, thank you for giving me this opportunity to suggest books. It means a lot. Hope you are doing well.

Don’t get me wrong, there are many good books on investing and I can definitely suggest some. But investing in equities takes a lot of time and effort, and the challenge is not just learning, it’s applying it at the right time.

What I have seen is that instead of only reading books, it helps more to study one sector deeply, layer by layer. First understand where that sector is going in the next 5 years — growth, demand, and changes.

For example, if you take shipping, then read concalls and annual reports of companies across the value chain. Then slowly start asking questions. That thinking develops over time.

After that, try to connect it with other sectors. Like last year shipping and metals both did well — that usually means something bigger is happening in the economy.

Based on that, you start thinking what can be the next sector over the next few years. This kind of thinking, in my view, you won’t get fully from books.

Still, if you want, I can share a few good books as a starting point.

English

⏩What is the intelligence layer that every naval vessel needs to function in combat?

Two companies cover this layer. One makes the sonar and weapons systems. One makes the radar and electronic warfare systems. Together they represent what makes a warship actually dangerous rather than just seaworthy.

CFF Fluid Control. The sonar and weapons systems layer.

Revenue 146 crore up 36.57%. PAT up 39.58%. EBITDA margin 28.38%. Order book 590 crore with 90% from defence.

India's first ever indigenized variable depth sonar systems for ASW crafts through Atlas Elektronik technology transfer. Steering gear and weapon systems for Scorpene submarines under P75 programme. Buoyant wire antennas for submarine communication replacing imports. IR suppression systems for Indian Navy.

This company makes what the sonar sees with. What the submarine steers with. What the vessel communicates through.

Not the vessel. The intelligence inside it.

Every submarine that Mazagon Dock builds under P75 needs CFF's systems. Every ASW craft that GRSE delivers needs CFF's sonar. The correlation is direct and automatic.

Transition from component supplier to systems integrator underway. Component suppliers earn margins on individual parts. Systems integrators earn margins on entire integrated solutions. Higher value. More recurring. Harder to replace.

Technology partnerships with Atlas Elektronik, Naval Group, and Nereides. Each brings technology transfer that India is building indigenously for the first time. First mover advantage in each category is structural.

Astra Microwave. The radar and electronic warfare layer.

Revenue 197 crore up 28.1%. Order book 1,891 crore. Targeting 18 to 20% revenue growth FY26.

Shipborne radar development contract from DRDO almost in final stage of execution. Completion expected December 2025. Indian Navy already expressing interest in acquiring more indigenous radars after seeing the technology in action.

Management said they expect more clarity on naval orders in next few months.

A development contract becomes a production contract. Production contract for shipborne radars means 10 or 20 or 50 vessels depending on Navy requirements. Management said too early to comment on quantity. But the Navy's expressed interest after seeing the technology is the signal that matters.

Transition from build to print to build to specification means Astra increasingly owns the design. When you own the design you own the repeat orders. When you own the repeat orders you own the margin for the lifecycle of every vessel carrying that radar.

Revenue 197 crore today. Order book nearly 10 times annual revenue. Naval radar is one part of a broader defence electronics portfolio that includes electronic warfare, space electronics, and anti drone systems.

⏩What is management collectively saying across all these companies and what does that convergence tell you?

This is the most important question of all.

Line up all six managements together and listen to what they are saying simultaneously.

Krishna Defence. India's fleet expanding to 175 to 200 warships. 68 warships and vessels currently on order worth 2 lakh crore. Expects geopolitical tensions to fast track procurement files. Targeting 500 crore revenue in 3 to 4 years.

Marine Electricals. 200 ship combat fleet target by 2027 acting as catalyst for unprecedented naval expansion. 81 ships under construction. 99 more in planning. 51 Coast Guard vessels in progress. Most confident about marine shipbuilding as cornerstone business.

Quest Flow Controls. Defence marine segment doubled. Protected market from 75 percent indigenisation mandate. First naval IPMS valve project completed. Strongest conviction in defence and marine going forward.

CFF Fluid Control. India's defence sector entering its golden era. Transition from component supply to complex system integration. Technology partnerships creating first mover advantage in multiple naval categories.

Astra Microwave. 18 to 20% revenue growth targeted. Naval radar development nearing completion. Navy expressing interest in more indigenous systems. Order book nearly 10 times annual revenue.

Cochin Shipyard, GRSE, Mazagon Dock. Combined order book exceeding 75,000 crore. Repair revenues doubling. New dry docks commissioned. International partnerships signed. All targeting aggressive growth through 2030 and beyond.

Now see what they are all describing together.

Not six separate company stories. One ecosystem. One expanding market. Six companies positioned at six different layers of the same chain.

The shipyard builds the vessel. Krishna Defence supplies the structural steel. Marine Electricals supplies the electrical and bridge systems. Quest Flow Controls supplies the valves. CFF Fluid Control supplies the sonar and weapons systems. Astra Microwave supplies the radar.

When the vessel comes in for mandatory repair every five years. Same chain. Same companies. Same demand. Recurring.

Every management is saying the same thing in different words. The market is expanding. The indigenisation mandate is protecting domestic suppliers. The order visibility is extending to 2030 and beyond. And we were already building before the war started.

That convergence across six management teams is not coincidence. It is the signal.

When six companies in the same supply chain are all independently reporting accelerating revenues, strengthening management tone, and increasing order books at the same time the market is not pricing a theme. It is pricing the early innings of a multi year structural cycle.

The war made it visible. The companies were already ready.

That is the gap. That is what is closing between 2026 and 2030 and the companies positioned at the closing of that gap are the ones that matter.

Not the ones everyone is watching right now. The ones the market will spend the next 12 to 18 months discovering.

Layer by layer. Quarter by quarter.That is always where the returns come from.

English

Why am I telling you to look at ship repair for the next few years?

Because there is a map and most people are not connecting it. Let me show you the map.

⏩What is the map most people are missing?

The previous post showed you the structural repair story. Mandatory dry docking. 500 events per year. 30 percent leaking to Singapore China and UAE. Cochin Shipyard. GRSE. Mazagon Dock. The dry dock slot as the constraint.

That was the first layer of the map. But a map has more than one layer.

Think about what happens when India's ship repair market grows from 1.3 billion dollars today to 2.8 billion dollars by 2033.

More vessels enter Indian dry docks. More repair work gets done domestically instead of going abroad. Cochin Shipyard fills its new 310 metre dry dock. GRSE adds another dry dock. Mazagon Dock ramps repair revenue through Colombo Dockyard.

That is the visible layer. The layer the market is starting to discover. Now think about what every single one of those repair jobs actually requires inside the vessel.

Structural steel sections that form the hull. Valves inspected or replaced. Electrical and bridge systems recalibrated. Sonar systems checked. Radar systems tested. Weapon systems maintained.

These are not optional additions to the repair story. They are the chain that runs underneath it. And the companies sitting at each point in that chain are what most people have not connected yet.

⏩Why does this matter specifically for the next three to five years?

Because three things are accelerating simultaneously.

Ship repair growing as 30% of work comes back from Singapore and UAE.

Naval shipbuilding accelerating with Corvettes, frigates, submarines, ASW crafts. India expanding its fleet from 132 ships today to 175 to 200 warships. 81 vessels currently under construction. 99 more in planning phase. 51 Coast Guard vessels in progress. 30 more planned.

Indigenisation mandate pushing 75% of defence capital budget to domestic sourcing. Every system on every vessel. Structural steel. Valves. Electrical systems. Sonar. Radar. All of it being sourced domestically for the first time.

When all three accelerate together the companies supplying each layer of every vessel compound automatically. Not because of any one contract. Because every contract across all three accelerating programmes generates demand for their products simultaneously.

The chain runs from the dry dock slot all the way down to the structural steel sections the vessel is built from. Most people are looking at the dry dock. The chain goes much deeper.

⏩Start from the foundation. What goes into building the vessel before anything else?

Before any valve goes in. Before any sonar goes in. Before any radar goes in. Before any electrical system goes in. The steel structure of the vessel has to be built.

Bulb bars are the structural steel sections that form the hull frames of every naval vessel. Without bulb bars there is no vessel. Without the vessel there is nothing else to put inside it.

India was importing these from Russia until one company indigenised them and received a Defence Technology Absorption Award from PM Modi for doing so.

Krishna Defence

Revenue 194 crore up 83.1%. PAT up 124%. EBITDA up 96.3%. Order book 270 crore highest ever. 96% revenue from defence.

Registered and approved vendor for Indian Navy supplying to all prominent shipbuilders. MDL. GRSE. Cochin Shipyard. All of them. When any of these yards wins a contract Krishna Defence supplies the structural steel sections for the vessels being built.

Doubled manufacturing capacity at Halol facility operational April 2025. Current utilisation 60% targeting 80%. Total installed capacity can support 350 to 400 crore revenue.

But here is what management is building beyond bulb bars.

Acquired 20% stake in Conceptia Software Technologies. Marine and offshore engineering design company with 60 to 65 crore revenue. Partnership with Planys Technologies for underwater remotely operated vehicles for hull cleaning and paint services. VABO Composite JV for fire resistant doors and hatches on naval vessels. Increasing stake in Waveoptix Defence Solutions from 25 to 40% for defence electronics.

Management is not just selling structural steel. They are building a portfolio of companies that together cover multiple layers of the naval supply chain. Each acquisition takes them one layer deeper into the vessel.

Management tone significantly strengthened. Most confident about naval shipbuilding as primary growth engine. Expects geopolitical tensions to fast track procurement files. Pipeline tenders worth 120 to 130 crore with 50 to 60% win ratio expectation.

Targeting 30 to 40 percent CAGR over next 3 to 5 years. Revenue target 500 crore in next 3 to 4 years from 194 crore today.

⏩What goes into the vessel as the systems are installed?

Two companies cover this layer. One supplies the electrical and bridge systems. One supplies the valves and flow control systems. Both are directly correlated to every GRSE and Cochin Shipyard contract.

Marine Electricals. The electrical and bridge systems layer.

45 years of relationship with Indian Navy. Started in 1978. This is not a new entrant chasing a theme. This is a company that has been inside every major Indian naval vessel for nearly five decades.

Integrated Bridge Systems. Navigation. Communication. Electrical automation. NAVCOM packages. Supplied to P17A frigates, ASW crafts, Next Gen OPVs, Next Gen Missile Vessels.

Revenue 700 crore up from 533 crore. Net profit up 44.69%. Order book 524 crore.

Recent order from GRSE and Goa Shipyard for 77.47 crore for Integrated Bridge Systems in May 2025. Delivery over 27 months.

Now see the scale of what is coming.

81 ships currently under construction across various naval projects. 99 more in planning phase. 51 Coast Guard vessels in progress. 30 more planned. Every single one of those vessels needs an Integrated Bridge System. Navigation systems. Electrical automation. Communication systems.

Marine Electricals has 12 branch offices around the coast specifically for waterfront support. Annual Maintenance Contracts and Rate Repair Contracts running in parallel with every supply contract. That AMC and RRC revenue is the recurring layer. Every vessel they supply equipment to generates a service contract behind it for the life of the vessel.

Management tone significantly strengthened. Highlighting unprecedented naval expansion as primary growth driver. Most confident about marine shipbuilding as cornerstone business with 45 plus years of experience and established product portfolio.

Quest Flow Controls. The valve layer nobody is watching.

Revenue 67 crore. Small. But read what is happening inside that number.

Defence and marine segment more than doubled year on year in FY25. Went from 20% of revenues to 35% in one year. Not gradual. Sharp.

Completed India's first naval Integrated Platform Management System valve project. Established credentials in a niche where almost no Indian company has operated before. Mission critical valves. IPMS compatible. Certified for naval applications.

August 2025 order from Garden Reach for 23.56 crore for supply of valves and spares. July 2025 order from BHEL for naval valves.

Now see the chain connection.

GRSE has an order book of 21,700 crore. Next Generation Corvette contract worth 25,000 crore expected this financial year. Every vessel in those contracts needs marine valves. Mission critical. Non substitutable. Certified.

When GRSE wins Quest Flow Controls wins. Automatically. The market has not priced that connection.

75% of defence capital budget must be sourced domestically. Every valve on every Indian naval vessel is a protected order. No foreign competition allowed.

Order backlog at beginning of FY26 already 50 plus crore on a 67 crore revenue base. Three quarters of annual revenue locked before the year started.

Management most confident about protected market dynamics from indigenisation mandates. Strongest conviction in defence and marine as core growth driver going forward.

Saurav@ThinkWithSaurav

Before you think about the shipping sector understand this first. This will help you find the right stocks around it. If you are in that space. Most people watching shipping right now are watching one number. Freight rates. Tankers at 400,000 dollars per day. Great Eastern's next quarterly result. That is the right thing to watch for the next two months. Here is what to watch for the next three years. Every commercial vessel is legally required to enter dry dock at least twice every five years. Annual surveys. Intermediate surveys. Special survey every five years. Miss these and the ship cannot trade. Insurance lapses. Port entry denied. This is not discretionary demand. Not dependent on freight rates. Not dependent on sentiment. It happens. Every year. Every vessel. Without exception. India's fleet alone generates roughly 500 mandatory dry docking events every year. Before counting a single foreign vessel. Before counting war driven repair surge. Before counting vessels stressed by longer Africa rerouting. 500 events. Structurally. Unavoidably. Regardless of what Nifty does. Now here is the problem that creates the opportunity. Over 30 percent of India's addressable repair work currently flows to Singapore, China, and UAE. Not because it is cheaper. Because it is faster and more reliable. India has dry docks but most are defence oriented and poorly equipped for fast turnaround commercial repair. The gap is not demand. The gap is capacity and execution. Now look at what is changing. Cochin Shipyard. New 310 metre dry dock commissioned January 2024. MOU signed with Maersk February 2025. MOU with Drydocks World UAE. Master repair agreement with US Navy. Ship repair EBIT margin 44.2 percent. Shipbuilding margin 8%. Management guided 14 to 15% revenue growth FY26. That margin difference tells you everything. Repair is 7 percent of their order book but generates margins five times higher than building new ships. Why? Because dry dock slots are the constraint. When slots fill up pricing power shifts completely to the yard. Ship owner cannot negotiate. Ship must dock. Mazagon Dock. Plans to ramp repair revenue from 1,000 crore to 1,500 crore. Made their first ever international acquisition. Controlling stake in Colombo Dockyard for 53 million dollars. Management is telling you exactly where the next growth layer is. Garden Reach Shipbuilders. Repair revenue grew from 19 crore in FY22 to 114 crore in FY25. Six times in three years. Management explicitly said they are shifting toward repair because margins are higher than shipbuilding. Three public sector shipyards. All moving in the same direction. All saying the same thing in their management commentary. That convergence is the signal. Now the war added urgency on top of a structural story that was already building. Ships stressed from longer Africa routes. Maintenance deferred at 400,000 dollars per day. That deferred maintenance is now becoming mandatory. And it has to go somewhere. The 30% leaking to Singapore and UAE is beginning to come home. Quarter by quarter. As new domestic capacity comes online. Defence shipbuilding. Long cycle. 7 to 10 years per vessel. Slow revenue. Government pricing pressure. 8 percent margin. Ship repair. Short cycle. Weeks not years. Fast cash collection. Commercial pricing. 44% margin. Freight rate stories last two quarters. Everyone is watching them right now. Dry dock slot stories last three to five years. Almost nobody is watching them yet. That gap between what everyone is watching and what is actually building is exactly where the next three years of returns come from. Find the constraint. Own the constraint. Wait for the cycle to fill it.

English

19 March I wrote this.

The rupee falling to 92 is what pressed the exit button for FIIs. Not STCG. Not LTCG. Not STT. The rupee dollar math stopped working for them.

Two days later here is where we stand.

WTI crude fell today. Down nearly 2%. Feels like relief. But Brent, which is what India actually pays for its oil imports, is still sitting above $107. For India the pain has not reduced as much as the headline number suggests.

And the rupee. It hit 94.05 today at that time. Its biggest single day fall in four years.

So the exit button is still being pressed. Just slightly less hard today than yesterday.

But here is the new information worth thinking about this weekend.

Goldman Sachs said this week that if oil flows through the Strait gradually recover from April, Brent could fall to the 70s by Q4 2026. The US is already discussing lifting sanctions on Iranian crude to bring prices down. Trump publicly called on allies to help reopen the Strait. The UK has sent military planners to work on a plan.

These are not peace signals yet. But they are the first signs that the people with the most to lose from high oil, which includes the US itself paying $4 a gallon at the pump, are actively looking for a way out.

Now connect this back to the rupee and FIIs.

The exit button has one on switch and one off switch.

The on switch is crude up plus rupee down. That is what March gave us.

The off switch is crude falling plus rupee recovering.

When Brent moves from 107 toward 90, India's dollar demand for oil reduces. Less dollar demand means less rupee pressure. Rupee starts recovering from 93 toward 89 or 88. When that happens the FII math changes completely. A 10% gain in rupee terms starts looking like a real dollar return again. The reason to leave disappears.

And history says what comes after that is not slow.

After 2020 when the rupee recovered and crude fell, FIIs brought back 38 billion dollars into India in 18 months. They never trickle back. They come back the same way they left. Fast and together.

The exit button is still on right now. Brent at 107 makes sure of that.

But Goldman Sachs just told you when it could switch off.

Watch Brent. Not WTI. Not Nifty.

Brent below 90 is when the rupee math starts working again for FIIs.

That is the number that changes everything else.

Saurav@ThinkWithSaurav

STCG. LTCG. STT. High valuations all these things are okay. But this is not the actual reason for FII selling. Yes, these things matter. But they are not the main reason FIIs are leaving right now. Not in March 2026. The main reason is the rupee is at 92 against the dollar. See, FIIs bought Indian stocks when the rupee was at 83. Their investment went up 10% in rupee terms. But now when they change those rupees back to dollars, that 10% gain comes down to somewhere around 2% because the rupee itself went down against the dollar in the same time. Their dollar return, which is the only return that actually counts to them, just disappeared. Now think about it why would you stay in a market where the currency is falling, oil is above 100 dollars, and every passing day your dollar return is getting smaller. You would leave too. This is why FIIs pulled out over 52,000 crore from Indian equities in just the first nine trading days of March. They are not leaving because they studied every Indian business and decided things are bad. They are leaving because the rupee-dollar math stopped working for them. Now one part most people are not connecting is that when FIIs need to exit fast, they don't go to small caps or mid caps. They can't. Those stocks don't have enough buyers on any given day to handle big selling. If an FII tries to exit a small cap in a hurry, the price falls fast before they are even halfway out. So they go where they can sell fast like large banks, IT majors, oil companies. Stocks where buying and selling happens easily. In and out in minutes. Price barely moves compared to how big the trade is. That FII selling in large caps is what pulls Nifty down. But fear doesn't stay in one place. Retail investors see Nifty falling. They see the FII numbers in the news. They panic and sell whatever they own, including small caps and mid caps that FIIs were never even sitting in. So your small cap falls 40% not because FIIs sold it, but because everyone around you got scared watching FIIs sell something completely different. Nifty falls because of what FIIs are selling. Small caps fall because of what nobody is buying. Same fear. Completely different reason. And the same reason that causes the deeper fall also causes the sharper recovery. When fear passes, buyers come back to a stock where very few people are left willing to sell. Price has to move up fast to find sellers. That is why small caps fall harder and recover harder. Same reason both times. The STT and LTCG discussion is real. But it is a slow issue. The rupee falling to 92 is what pressed the exit button in March. Understanding that one thing changes how you read everything else happening in the market right now.

English

@ThinkWithSaurav Yes reading. Thank you. Hooked to your content. 👌🙏

English

Saturday evening.

Two things are happening at the same time right now that most people are not connecting.

One. The market is falling in a very specific way. Not randomly. There is a pattern in the charts that explains exactly why Nifty fell, why your small cap fell harder, why banks are red and pharma is green, and what three numbers to watch before Monday opens.

Two. Right in the middle of that fear, the biggest opportunity map of the next 10 years is sitting open. Written by the government. Backed by national urgency. Connected to everything India cannot afford to get wrong. Grid. Battery storage. Battery recycling. Oil and gas storage. Ports. Ship repair. Almost nobody is talking about the right parts yet.

Understanding both together changes how you see this market completely.

English

This is exactly right.

Most people who quit in phase 1 do not quit because they lack patience. They quit because they are in the wrong cycle. Watching a great company go nowhere for 5 years while their neighbour's portfolio doubles is not a patience problem. It is a cycle problem.

Compounding works the way you described. But only when the underlying business is in the right phase of the right cycle at the right time.

HDFC Bank investors have been patient for 5 years. 0.8% return. Not because they lacked discipline. Because the banking cycle was not the rewarded cycle from (2020 to 2025).

Polycab investors who bought in (2020) and held through uncertainty experienced exactly what you described. First two years nothing dramatic. Then grid capex started scaling. Then the numbers started compounding. Then suddenly everyone noticed.

The sudden part is always the same. Government order books converting to revenue. New capacity hitting full utilisation. Margin expansion from operating leverage. All arriving in the same quarter. And the stock moving 40 to 50% in months after years of waiting.

But here is what most people miss about phase 1.

Phase 1 is not nothing happening. Phase 1 is everything being built invisibly. Order books filling. Capacity coming online. Management executing. Government policy solidifying. The foundation being laid for the sudden that everyone will call obvious in hindsight.

The people who quit in phase 1 always say the same thing when phase 3 arrives.

I knew about that company. I just did not hold long enough.

The problem was never patience.

The problem was not understanding deeply enough what was being built in phase 1 to have the conviction to stay through phase 2.

Conviction comes from understanding the cycle. Not from following someone else's recommendation.

English

Compounding is slow… then sudden.

First 5 years: Nothing happens

Next 5 years: Something happens

Last 5 years: Everything happens

Most quit in phase 1.

English

Sir the problem is not with these companies.

HDFC Bank is a great bank. TCS is a great company. HUL has built one of the most powerful distribution networks in India. Asian Paints has a moat most businesses can only dream of. These are genuinely excellent businesses run by excellent managements.

The problem is the cycle.

Every 5 years in India a completely different set of sectors gets rewarded. The last 5 years were the cycle of defence, railways, solar, grid, and transmission. HAL gave 4x. Polycab gave 9x. Cochin Shipyard gave 6x. RVNL gave 5x. In the same 5 years that HDFC Bank gave 0.8% and TCS gave minus 5%.

Not because HDFC Bank is worse than Cochin Shipyard. But because the cycle rewarded whoever was solving what India needed most at that specific moment and what India needed from (2020 to 2025) was defence self reliance, renewable energy, and grid modernisation. Not more banking penetration or more IT outsourcing.

So long term investing is actually simple. But only if you get three things right together.

First understand the cycle. What does India need to build most urgently in the next 5 years. That question alone eliminates most wrong decisions.

Second find the right sector inside that cycle. Defence is right. But defence electronics is more right than defence platforms right now. Solar is right. But battery storage is more right than solar panels right now. Shipping is right. But ship repair is more right than shipbuilding right now.

Third find the right company inside that sector. The one with the balance sheet to survive the pre revenue phase. The management that does what it says. The order book that is real and growing. The position in the cycle that captures the margin not just the volume.

Most people do step three without doing step one and step two. They find a great company in the wrong cycle and wonder why it does not move.

Long term investing is not hard. But it requires understanding India's growth journey first. The companies second. The valuations last.

Most people do it exactly in reverse.

English

Top Indian companies. Massive brands. Huge market caps.

But 5-year returns? Almost zero.

😩HDFC Bank → 0.8%

😩TCS → –5.3%

😩Infosys → –1.7%

😩HUL → –1.4%

😩Asian Paints → –1.8%

😩Wipro → –1.6%

Long Term Investing in Stocks is not that easy

English

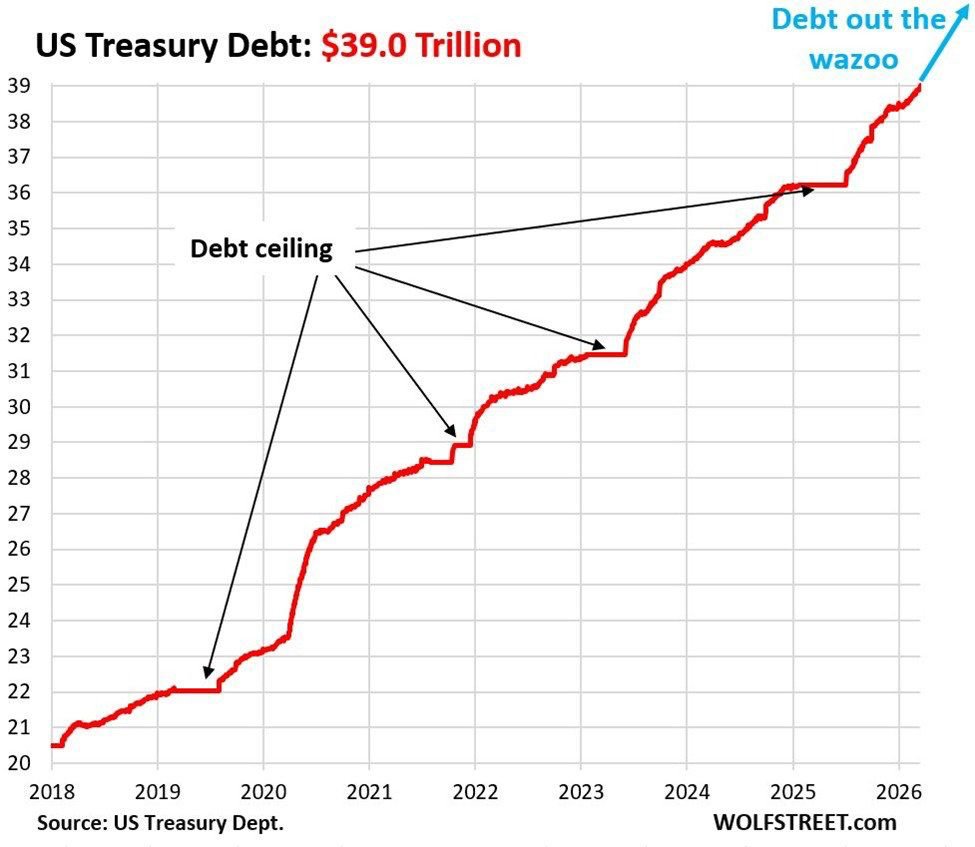

(2019) debt ceiling hit. Raised. Kept going. (2021) debt ceiling hit. Raised. Kept going. (2023) debt ceiling hit. Raised. Kept going. (2025) Moody's downgraded US from AAA to Aa1. First downgrade in over 100 years. Kept going.

America now pays 952 billion dollars per year just in interest. Not defence. Not healthcare. Just interest. By (2030) total debt projected to cross 52 trillion. By (2035) debt to GDP reaching 134%.

And Trump is President until (2029). Tax cuts continuing. War spending continuing. Tariffs slowing global trade. The number is not slowing down. It is accelerating.

Now the India angle .

India's debt to GDP sits at 58.9% (2025). Less than half of America's 122 percent. India's GDP growing at 6.5 to 7 percent annually meaning the burden gets proportionally smaller every year. Two trajectories moving in completely opposite directions.

When the world's reserve currency loses its AAA rating and pays 11 billion dollars per week just in interest the global capital system starts asking uncomfortable questions. That questioning creates opportunities for countries with cleaner balance sheets and genuine productive capacity.

India is building that productive capacity right now. Battery storage. Green ammonia. Defence electronics. Domestic manufacturing. Strategic independence across energy food and materials.

The 39 trillion dollar chart is not just America's problem.

It is the reason India's next decade matters more than most people realise.

English

39 trillion. And every debt ceiling that was supposed to stop it became a speed bump.

But the more important question is not the number itself. It is what this trajectory does to the system built around that number.

The dollar did not become the world's reserve currency because America was the most virtuous. It became the reserve currency because America had the deepest capital markets, the strongest rule of law, and the most credible institutions. Countries held dollars because they trusted the system behind the dollar.

That trust is the asset being slowly depleted with every trillion added and here is what makes this moment different from every previous debt ceiling debate.

This time America is simultaneously running a war in the Middle East, decoupling from China, pressuring allies on trade, and adding debt at a pace that makes the 2008 crisis look modest. The global south is watching all of this at the same time and they are drawing conclusions.

Central banks bought more gold in 2023 and 2024 than any year since 1967. Not because gold became fashionable. Because reserve managers are quietly asking the question they were never supposed to ask out loud. What if the dollar is not as safe as we assumed.

BRICS nations are settling more trade in local currencies. India is buying Russian oil in rupees. The dollar's share of global reserves has fallen from 73 percent in 2001 to around 58 percent today. That is not a collapse. That is a slow structural shift that compounds over decades.

Now here is the India angle that connects everything happening right now.

India sits at a unique intersection of this global shift.

On one side India is deeply exposed to the dollar system. 85% of crude imported and priced in dollars. Battery materials bought in dollars from China. Urea purchased in dollars from the Middle East. Every dollar of import dependence makes India vulnerable to both dollar strength and dollar system instability simultaneously.

On the other side India is one of the few large economies that can genuinely benefit from a multipolar world. Large domestic market. Young population. Strategic geography. Growing manufacturing base. And crucially a government that has finally understood that import dependence is a national security risk not just an economic variable.

What is happening right now in India is the beginning of the answer to that 39 trillion dollar chart.

Battery storage so the grid runs on stored Indian solar not imported oil priced in dollars. Green ammonia so urea is made from Indian sunshine not Qatari LNG bought in dollars. Domestic cell manufacturing so EVs run on Indian energy not imported crude.

Semiconductor components so chips are partly made in India not entirely dependent on Taiwan and priced in dollars.

Every one of these reduces India's structural dollar dependency. Not overnight. Layer by layer. Cycle by cycle.

And here is what Indian investors should understand clearly.

The companies building this dollar independence are not building it because it is fashionable. They are building it because the government of India has finally understood that every rupee of import dependence is a rupee that makes India vulnerable to a chart that looks exactly like the one above.

39 trillion is not just America's problem.

It is the reason India is being forced to build what it should have built 20 years ago.

And the companies doing that building are available today at prices that the market has not yet connected to what they are actually solving.

That is the opportunity sitting inside the problem this chart is showing you.

English

Hard to disagree on the option selling part. In a market driven by geopolitics and crude oil moves that nobody can predict with precision selling options right now is genuinely dangerous. The person on the other side of that trade is the war itself.

But on debt funds.

Debt funds protect capital. They do not build wealth and right now while everyone is either panicking or parking money safely something else is happening quietly.

The companies building India's energy security, battery storage, and food security are running their businesses normally. Order books growing. Government customers placing orders. Capex being deployed on time. Their revenues do not depend on crude prices or FII flows or rupee levels.

The question is not just how to protect what you have during this uncertainty. The question is whether this uncertainty is creating the entry point for the next cycle that you will look back on in 5 years and wish you had used better.

Debt funds for the portion you cannot afford to lose. Absolutely. But the portion you are investing for the next 5 years deserves a different question entirely.

Not debt versus options. But which cycle is just beginning and which companies are building what India cannot afford to get wrong.

English

It’s better to invest in debt mutual funds instead of doing option selling in the current market.

I’m open to arguing, but I don’t think anyone will disagree.

English

These are genuinely good companies. No argument there.

But see what this data is actually telling you.

5 years is exactly one full market cycle and every cycle in India has rewarded a completely different set of sectors. The problem is not these companies. The problem is that most of them belong to the previous cycle.

Think about it.

The last 5 years were the cycle of defence, railways, solar, grid, and transmission. HAL. BEL. Polycab. KEI. Cochin Shipyard. RVNL. These gave 5x 8x 10x returns in the same 5 years that HDFC Bank gave 0.8% and TCS gave minus 5%.

Not because HDFC Bank is a bad bank. Not because TCS is a bad company. Because they were not in the cycle that the last 5 years rewarded.

The cycle does not care about quality. It rewards whoever is solving what India needs most at that specific moment.

So the question is not why did these 25 companies underperform. The real question is what does the next 5 year cycle reward and that answer is already visible if you understand what India is being forced to build right now.

Energy security. Battery storage. Food security. Strategic manufacturing. The companies solving these problems have government customers who do not check Nifty before placing orders.

Same mistake repeated every cycle. People hold quality names from the last cycle and wonder why returns disappoint.

Understand the cycle first. Then find the quality companies inside that cycle.

That combination is the only thing that has worked since 2003.

English