Sabitlenmiş Tweet

Saurav

3K posts

Saurav

@ThinkWithSaurav

The sector can be right. What matters is where inside it. Focus on what’s coming, not what’s visible. By the time attention arrives, the move is often over.

Before It Moves Katılım Ocak 2024

8 Takip Edilen672 Takipçiler

19 March I wrote this.

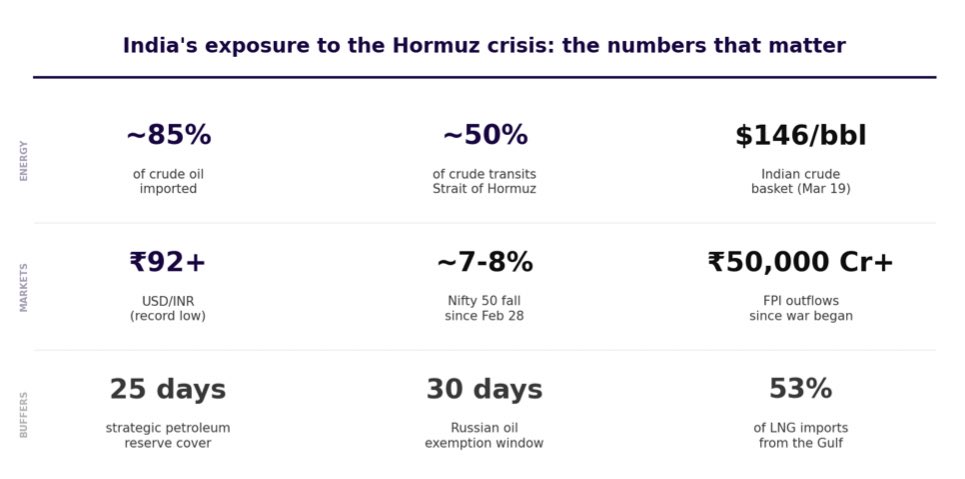

The rupee falling to 92 is what pressed the exit button for FIIs. Not STCG. Not LTCG. Not STT. The rupee dollar math stopped working for them.

Two days later here is where we stand.

WTI crude fell today. Down nearly 2%. Feels like relief. But Brent, which is what India actually pays for its oil imports, is still sitting above $107. For India the pain has not reduced as much as the headline number suggests.

And the rupee. It hit 94.05 today at that time. Its biggest single day fall in four years.

So the exit button is still being pressed. Just slightly less hard today than yesterday.

But here is the new information worth thinking about this weekend.

Goldman Sachs said this week that if oil flows through the Strait gradually recover from April, Brent could fall to the 70s by Q4 2026. The US is already discussing lifting sanctions on Iranian crude to bring prices down. Trump publicly called on allies to help reopen the Strait. The UK has sent military planners to work on a plan.

These are not peace signals yet. But they are the first signs that the people with the most to lose from high oil, which includes the US itself paying $4 a gallon at the pump, are actively looking for a way out.

Now connect this back to the rupee and FIIs.

The exit button has one on switch and one off switch.

The on switch is crude up plus rupee down. That is what March gave us.

The off switch is crude falling plus rupee recovering.

When Brent moves from 107 toward 90, India's dollar demand for oil reduces. Less dollar demand means less rupee pressure. Rupee starts recovering from 93 toward 89 or 88. When that happens the FII math changes completely. A 10% gain in rupee terms starts looking like a real dollar return again. The reason to leave disappears.

And history says what comes after that is not slow.

After 2020 when the rupee recovered and crude fell, FIIs brought back 38 billion dollars into India in 18 months. They never trickle back. They come back the same way they left. Fast and together.

The exit button is still on right now. Brent at 107 makes sure of that.

But Goldman Sachs just told you when it could switch off.

Watch Brent. Not WTI. Not Nifty.

Brent below 90 is when the rupee math starts working again for FIIs.

That is the number that changes everything else.

Saurav@ThinkWithSaurav

STCG. LTCG. STT. High valuations all these things are okay. But this is not the actual reason for FII selling. Yes, these things matter. But they are not the main reason FIIs are leaving right now. Not in March 2026. The main reason is the rupee is at 92 against the dollar. See, FIIs bought Indian stocks when the rupee was at 83. Their investment went up 10% in rupee terms. But now when they change those rupees back to dollars, that 10% gain comes down to somewhere around 2% because the rupee itself went down against the dollar in the same time. Their dollar return, which is the only return that actually counts to them, just disappeared. Now think about it why would you stay in a market where the currency is falling, oil is above 100 dollars, and every passing day your dollar return is getting smaller. You would leave too. This is why FIIs pulled out over 52,000 crore from Indian equities in just the first nine trading days of March. They are not leaving because they studied every Indian business and decided things are bad. They are leaving because the rupee-dollar math stopped working for them. Now one part most people are not connecting is that when FIIs need to exit fast, they don't go to small caps or mid caps. They can't. Those stocks don't have enough buyers on any given day to handle big selling. If an FII tries to exit a small cap in a hurry, the price falls fast before they are even halfway out. So they go where they can sell fast like large banks, IT majors, oil companies. Stocks where buying and selling happens easily. In and out in minutes. Price barely moves compared to how big the trade is. That FII selling in large caps is what pulls Nifty down. But fear doesn't stay in one place. Retail investors see Nifty falling. They see the FII numbers in the news. They panic and sell whatever they own, including small caps and mid caps that FIIs were never even sitting in. So your small cap falls 40% not because FIIs sold it, but because everyone around you got scared watching FIIs sell something completely different. Nifty falls because of what FIIs are selling. Small caps fall because of what nobody is buying. Same fear. Completely different reason. And the same reason that causes the deeper fall also causes the sharper recovery. When fear passes, buyers come back to a stock where very few people are left willing to sell. Price has to move up fast to find sellers. That is why small caps fall harder and recover harder. Same reason both times. The STT and LTCG discussion is real. But it is a slow issue. The rupee falling to 92 is what pressed the exit button in March. Understanding that one thing changes how you read everything else happening in the market right now.

English

@ThinkWithSaurav Yes reading. Thank you. Hooked to your content. 👌🙏

English

Saturday evening.

Two things are happening at the same time right now that most people are not connecting.

One. The market is falling in a very specific way. Not randomly. There is a pattern in the charts that explains exactly why Nifty fell, why your small cap fell harder, why banks are red and pharma is green, and what three numbers to watch before Monday opens.

Two. Right in the middle of that fear, the biggest opportunity map of the next 10 years is sitting open. Written by the government. Backed by national urgency. Connected to everything India cannot afford to get wrong. Grid. Battery storage. Battery recycling. Oil and gas storage. Ports. Ship repair. Almost nobody is talking about the right parts yet.

Understanding both together changes how you see this market completely.

English

This is exactly right.

Most people who quit in phase 1 do not quit because they lack patience. They quit because they are in the wrong cycle. Watching a great company go nowhere for 5 years while their neighbour's portfolio doubles is not a patience problem. It is a cycle problem.

Compounding works the way you described. But only when the underlying business is in the right phase of the right cycle at the right time.

HDFC Bank investors have been patient for 5 years. 0.8% return. Not because they lacked discipline. Because the banking cycle was not the rewarded cycle from (2020 to 2025).

Polycab investors who bought in (2020) and held through uncertainty experienced exactly what you described. First two years nothing dramatic. Then grid capex started scaling. Then the numbers started compounding. Then suddenly everyone noticed.

The sudden part is always the same. Government order books converting to revenue. New capacity hitting full utilisation. Margin expansion from operating leverage. All arriving in the same quarter. And the stock moving 40 to 50% in months after years of waiting.

But here is what most people miss about phase 1.

Phase 1 is not nothing happening. Phase 1 is everything being built invisibly. Order books filling. Capacity coming online. Management executing. Government policy solidifying. The foundation being laid for the sudden that everyone will call obvious in hindsight.

The people who quit in phase 1 always say the same thing when phase 3 arrives.

I knew about that company. I just did not hold long enough.

The problem was never patience.

The problem was not understanding deeply enough what was being built in phase 1 to have the conviction to stay through phase 2.

Conviction comes from understanding the cycle. Not from following someone else's recommendation.

English

Compounding is slow… then sudden.

First 5 years: Nothing happens

Next 5 years: Something happens

Last 5 years: Everything happens

Most quit in phase 1.

English

Sir the problem is not with these companies.

HDFC Bank is a great bank. TCS is a great company. HUL has built one of the most powerful distribution networks in India. Asian Paints has a moat most businesses can only dream of. These are genuinely excellent businesses run by excellent managements.

The problem is the cycle.

Every 5 years in India a completely different set of sectors gets rewarded. The last 5 years were the cycle of defence, railways, solar, grid, and transmission. HAL gave 4x. Polycab gave 9x. Cochin Shipyard gave 6x. RVNL gave 5x. In the same 5 years that HDFC Bank gave 0.8% and TCS gave minus 5%.

Not because HDFC Bank is worse than Cochin Shipyard. But because the cycle rewarded whoever was solving what India needed most at that specific moment and what India needed from (2020 to 2025) was defence self reliance, renewable energy, and grid modernisation. Not more banking penetration or more IT outsourcing.

So long term investing is actually simple. But only if you get three things right together.

First understand the cycle. What does India need to build most urgently in the next 5 years. That question alone eliminates most wrong decisions.

Second find the right sector inside that cycle. Defence is right. But defence electronics is more right than defence platforms right now. Solar is right. But battery storage is more right than solar panels right now. Shipping is right. But ship repair is more right than shipbuilding right now.

Third find the right company inside that sector. The one with the balance sheet to survive the pre revenue phase. The management that does what it says. The order book that is real and growing. The position in the cycle that captures the margin not just the volume.

Most people do step three without doing step one and step two. They find a great company in the wrong cycle and wonder why it does not move.

Long term investing is not hard. But it requires understanding India's growth journey first. The companies second. The valuations last.

Most people do it exactly in reverse.

English

Top Indian companies. Massive brands. Huge market caps.

But 5-year returns? Almost zero.

😩HDFC Bank → 0.8%

😩TCS → –5.3%

😩Infosys → –1.7%

😩HUL → –1.4%

😩Asian Paints → –1.8%

😩Wipro → –1.6%

Long Term Investing in Stocks is not that easy

English

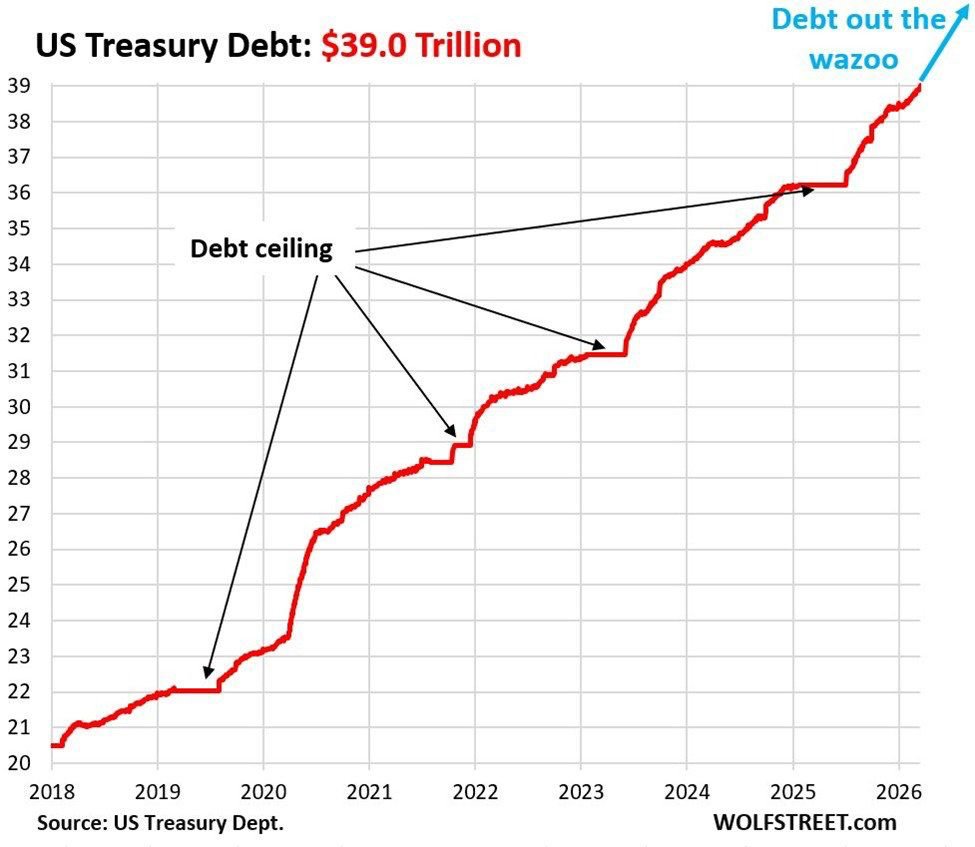

(2019) debt ceiling hit. Raised. Kept going. (2021) debt ceiling hit. Raised. Kept going. (2023) debt ceiling hit. Raised. Kept going. (2025) Moody's downgraded US from AAA to Aa1. First downgrade in over 100 years. Kept going.

America now pays 952 billion dollars per year just in interest. Not defence. Not healthcare. Just interest. By (2030) total debt projected to cross 52 trillion. By (2035) debt to GDP reaching 134%.

And Trump is President until (2029). Tax cuts continuing. War spending continuing. Tariffs slowing global trade. The number is not slowing down. It is accelerating.

Now the India angle .

India's debt to GDP sits at 58.9% (2025). Less than half of America's 122 percent. India's GDP growing at 6.5 to 7 percent annually meaning the burden gets proportionally smaller every year. Two trajectories moving in completely opposite directions.

When the world's reserve currency loses its AAA rating and pays 11 billion dollars per week just in interest the global capital system starts asking uncomfortable questions. That questioning creates opportunities for countries with cleaner balance sheets and genuine productive capacity.

India is building that productive capacity right now. Battery storage. Green ammonia. Defence electronics. Domestic manufacturing. Strategic independence across energy food and materials.

The 39 trillion dollar chart is not just America's problem.

It is the reason India's next decade matters more than most people realise.

English

39 trillion. And every debt ceiling that was supposed to stop it became a speed bump.

But the more important question is not the number itself. It is what this trajectory does to the system built around that number.

The dollar did not become the world's reserve currency because America was the most virtuous. It became the reserve currency because America had the deepest capital markets, the strongest rule of law, and the most credible institutions. Countries held dollars because they trusted the system behind the dollar.

That trust is the asset being slowly depleted with every trillion added and here is what makes this moment different from every previous debt ceiling debate.

This time America is simultaneously running a war in the Middle East, decoupling from China, pressuring allies on trade, and adding debt at a pace that makes the 2008 crisis look modest. The global south is watching all of this at the same time and they are drawing conclusions.

Central banks bought more gold in 2023 and 2024 than any year since 1967. Not because gold became fashionable. Because reserve managers are quietly asking the question they were never supposed to ask out loud. What if the dollar is not as safe as we assumed.

BRICS nations are settling more trade in local currencies. India is buying Russian oil in rupees. The dollar's share of global reserves has fallen from 73 percent in 2001 to around 58 percent today. That is not a collapse. That is a slow structural shift that compounds over decades.

Now here is the India angle that connects everything happening right now.

India sits at a unique intersection of this global shift.

On one side India is deeply exposed to the dollar system. 85% of crude imported and priced in dollars. Battery materials bought in dollars from China. Urea purchased in dollars from the Middle East. Every dollar of import dependence makes India vulnerable to both dollar strength and dollar system instability simultaneously.

On the other side India is one of the few large economies that can genuinely benefit from a multipolar world. Large domestic market. Young population. Strategic geography. Growing manufacturing base. And crucially a government that has finally understood that import dependence is a national security risk not just an economic variable.

What is happening right now in India is the beginning of the answer to that 39 trillion dollar chart.

Battery storage so the grid runs on stored Indian solar not imported oil priced in dollars. Green ammonia so urea is made from Indian sunshine not Qatari LNG bought in dollars. Domestic cell manufacturing so EVs run on Indian energy not imported crude.

Semiconductor components so chips are partly made in India not entirely dependent on Taiwan and priced in dollars.

Every one of these reduces India's structural dollar dependency. Not overnight. Layer by layer. Cycle by cycle.

And here is what Indian investors should understand clearly.

The companies building this dollar independence are not building it because it is fashionable. They are building it because the government of India has finally understood that every rupee of import dependence is a rupee that makes India vulnerable to a chart that looks exactly like the one above.

39 trillion is not just America's problem.

It is the reason India is being forced to build what it should have built 20 years ago.

And the companies doing that building are available today at prices that the market has not yet connected to what they are actually solving.

That is the opportunity sitting inside the problem this chart is showing you.

English

Hard to disagree on the option selling part. In a market driven by geopolitics and crude oil moves that nobody can predict with precision selling options right now is genuinely dangerous. The person on the other side of that trade is the war itself.

But on debt funds.

Debt funds protect capital. They do not build wealth and right now while everyone is either panicking or parking money safely something else is happening quietly.

The companies building India's energy security, battery storage, and food security are running their businesses normally. Order books growing. Government customers placing orders. Capex being deployed on time. Their revenues do not depend on crude prices or FII flows or rupee levels.

The question is not just how to protect what you have during this uncertainty. The question is whether this uncertainty is creating the entry point for the next cycle that you will look back on in 5 years and wish you had used better.

Debt funds for the portion you cannot afford to lose. Absolutely. But the portion you are investing for the next 5 years deserves a different question entirely.

Not debt versus options. But which cycle is just beginning and which companies are building what India cannot afford to get wrong.

English

It’s better to invest in debt mutual funds instead of doing option selling in the current market.

I’m open to arguing, but I don’t think anyone will disagree.

English

These are genuinely good companies. No argument there.

But see what this data is actually telling you.

5 years is exactly one full market cycle and every cycle in India has rewarded a completely different set of sectors. The problem is not these companies. The problem is that most of them belong to the previous cycle.

Think about it.

The last 5 years were the cycle of defence, railways, solar, grid, and transmission. HAL. BEL. Polycab. KEI. Cochin Shipyard. RVNL. These gave 5x 8x 10x returns in the same 5 years that HDFC Bank gave 0.8% and TCS gave minus 5%.

Not because HDFC Bank is a bad bank. Not because TCS is a bad company. Because they were not in the cycle that the last 5 years rewarded.

The cycle does not care about quality. It rewards whoever is solving what India needs most at that specific moment.

So the question is not why did these 25 companies underperform. The real question is what does the next 5 year cycle reward and that answer is already visible if you understand what India is being forced to build right now.

Energy security. Battery storage. Food security. Strategic manufacturing. The companies solving these problems have government customers who do not check Nifty before placing orders.

Same mistake repeated every cycle. People hold quality names from the last cycle and wonder why returns disappoint.

Understand the cycle first. Then find the quality companies inside that cycle.

That combination is the only thing that has worked since 2003.

English

Solar is not just the future. It is already happening and you are right that this crisis accelerates it.

But the layer most people miss.

Solar generates power. It does not store it. The sun does not shine at night. Wind does not blow on demand. India is targeting 500 GW of renewable energy by 2030. You cannot run that grid without massive storage sitting behind it.

And what is already happening to the grid.

The grid is breaking under the stress of intermittent renewable power. Voltage fluctuations. Frequency instability. Overloaded transmission lines. The grid was designed for steady thermal power. Not for solar that peaks at noon and disappears at sunset. That stress is visible right now in every state that has aggressively added solar capacity.

That grid stress is what makes storage not optional. Mandatory.

411 GWh of battery storage needed by 2031. Less than 1 GWh running today.

Now most people hear battery storage and think about the battery itself. That is one layer.

But inside every BESS project there are three layers that most people have never heard of.

BMS. The intelligence that monitors every cell. Manages charging and discharging. Prevents overheating. Ensures safety. Without BMS the battery is just a box of chemicals.

PCS. Converts DC power stored in the battery into AC power the grid can use. And converts AC grid power into DC to charge the battery. Without PCS the storage cannot connect to the grid at all.

EMS. The brain that decides in real time when to store power and when to release it. Optimises across price signals, grid demand, and battery health. Without EMS the storage is dumb.

The battery cell is the commodity layer. Anyone can import cells from China.

BMS, PCS, and EMS are the intelligence layer. This is where pricing power lives. This is where margins are highest. This is where switching costs are real because these systems are deeply integrated into grid operations.

The question is who owns the intelligence layer inside the storage that solar makes necessary.

We already saw this cycle play out once. Solar gave returns from 2020 to 2023. Then grid and transmission took over. Polycab. KEI. APAR. Because solar power needed cables and transformers to move.

Now storage is the next layer.

Solar is the beginning of the story. Not the whole story.

English

LPG Crisis is blessing in disguise for solar sector

Solar Sector is on 🔥

SOLAR IS THE FUTURE

🔖Bookmark It & Learn from it

English

@lohiarajesh Thanks. Just spending time reading and connecting things slowly.

English

@ThinkWithSaurav Your analysis are really very knowledgeable, it's surprising how do you manage .Gr8

English

The Strait closed. Three Indian urea plants cut production. Urea prices jumped 21% to a three year high. India quietly approached China asking them to lift export quotas before kharif season. China said no.

86% of the LNG India's fertilizer plants need comes from West Asia. Kharif season is 8 weeks away. More than 60 percent of India's agricultural output depends on fertilizer availability in June and July. Energy dependence hit your portfolio last month. Food dependence hits something more personal.

But what most people are not connecting is that the same pressure that forced India to build its own batteries, its own defence equipment, its own solar panels is now forcing India to build its own fertilizer independence. Domestic backward integrated producers are gaining structural cost advantage right now while import dependent competitors struggle with elevated input costs.

And the structural solution is already being built. Green ammonia made from Indian solar instead of Qatari LNG. SECI already auctioned 724,000 tonnes per year to 13 fertilizer plants. Ten year fixed contracts. First commercial plant commissioning 2028. From that year a portion of India's urea will be made from Indian sunshine. No Strait dependency. No Chinese permission required.

The war did not create this opportunity. It just made it impossible to delay any longer.

English

India built its growth inside a world of cheap freely available imports. This chart shows what happens when that world gets disrupted.

85% crude dependence. 53% LNG from the Gulf. 25 days of petroleum reserve cover. These do not change when the war ends. The vulnerability existed before the first missile was fired.

The Nifty will recover. The rupee will stabilise. FPIs will return.

But the structural problem in this chart only changes when India builds the alternative and that building is already happening.

English

@Shailes08254644 Exactly.

What is visible gets priced fast. What is building underneath takes time, and that’s where the real opportunity sits.

You just have to be early and patient till it becomes visible.

English

@ThinkWithSaurav "Focus on what is actually building underneath" thats where alpha is.

English

Before you think about the shipping sector understand this first. This will help you find the right stocks around it. If you are in that space.

Most people watching shipping right now are watching one number. Freight rates. Tankers at 400,000 dollars per day. Great Eastern's next quarterly result.

That is the right thing to watch for the next two months.

Here is what to watch for the next three years.

Every commercial vessel is legally required to enter dry dock at least twice every five years. Annual surveys. Intermediate surveys. Special survey every five years. Miss these and the ship cannot trade. Insurance lapses. Port entry denied.

This is not discretionary demand. Not dependent on freight rates. Not dependent on sentiment.

It happens. Every year. Every vessel. Without exception.

India's fleet alone generates roughly 500 mandatory dry docking events every year. Before counting a single foreign vessel. Before counting war driven repair surge. Before counting vessels stressed by longer Africa rerouting.

500 events. Structurally. Unavoidably. Regardless of what Nifty does.

Now here is the problem that creates the opportunity.

Over 30 percent of India's addressable repair work currently flows to Singapore, China, and UAE. Not because it is cheaper. Because it is faster and more reliable. India has dry docks but most are defence oriented and poorly equipped for fast turnaround commercial repair.

The gap is not demand. The gap is capacity and execution.

Now look at what is changing.

Cochin Shipyard. New 310 metre dry dock commissioned January 2024. MOU signed with Maersk February 2025. MOU with Drydocks World UAE. Master repair agreement with US Navy. Ship repair EBIT margin 44.2 percent. Shipbuilding margin 8%. Management guided 14 to 15% revenue growth FY26.

That margin difference tells you everything. Repair is 7 percent of their order book but generates margins five times higher than building new ships. Why? Because dry dock slots are the constraint. When slots fill up pricing power shifts completely to the yard. Ship owner cannot negotiate. Ship must dock.

Mazagon Dock. Plans to ramp repair revenue from 1,000 crore to 1,500 crore. Made their first ever international acquisition. Controlling stake in Colombo Dockyard for 53 million dollars. Management is telling you exactly where the next growth layer is.

Garden Reach Shipbuilders. Repair revenue grew from 19 crore in FY22 to 114 crore in FY25. Six times in three years. Management explicitly said they are shifting toward repair because margins are higher than shipbuilding.

Three public sector shipyards. All moving in the same direction. All saying the same thing in their management commentary. That convergence is the signal.

Now the war added urgency on top of a structural story that was already building.

Ships stressed from longer Africa routes. Maintenance deferred at 400,000 dollars per day. That deferred maintenance is now becoming mandatory. And it has to go somewhere.

The 30% leaking to Singapore and UAE is beginning to come home. Quarter by quarter. As new domestic capacity comes online.

Defence shipbuilding. Long cycle. 7 to 10 years per vessel. Slow revenue. Government pricing pressure. 8 percent margin.

Ship repair. Short cycle. Weeks not years. Fast cash collection. Commercial pricing. 44% margin.

Freight rate stories last two quarters. Everyone is watching them right now. Dry dock slot stories last three to five years. Almost nobody is watching them yet.

That gap between what everyone is watching and what is actually building is exactly where the next three years of returns come from.

Find the constraint. Own the constraint. Wait for the cycle to fill it.

English

Solid framework.

The crude GDP relationship is real but it is the symptom not the diagnosis.

The question is why India is still this exposed to crude after 75 years of independence. 85% import dependence is not a market problem. It is a structural problem that every government has acknowledged and none has fully solved.

Until now the urgency was not strong enough.

This war changed that. When the Strait closed and crude crossed 112 dollars every policy maker in Delhi felt what 85 percent dependence actually costs. Not in economic models. In the rupee. In the current account. In the subsidy bill. In fertilizer plants shutting down eight weeks before kharif season.

That feeling drives policy faster than any RBI or IMF report ever could.

So yes. Oil at 60 to 70 boosts consumption and supports GDP. That relationship is correct.

But the more important question for the next 5 years is this. Which companies are India building to make that crude GDP equation permanently less severe.

Battery storage so the grid runs on stored solar not imported oil. Green ammonia so urea is made from Indian sunshine not Qatari LNG. Domestic cell manufacturing so EVs run on Indian energy not imported crude.

Every percentage point reduction in import dependence permanently reduces the sensitivity of India's GDP to crude price movements.

That is not just an energy story. That is the biggest structural GDP story India has right now and the companies building it are available today.

English

India GDP vs Crude Oil🚨

India imports 85% of its crude. Higher oil = direct hit on growth.

Every $10 rise in crude cuts India’s GDP growth by 0.2–0.3% (estimates from Reserve Bank of India & International Monetary Fund).

Oil at $100+ means higher inflation, weaker Rupee, wider current account deficit. This means a 1% downside in GDP atleast.

Oil at $60–70 boosts consumption, lowers inflation & supports GDP.

English

@Shailes08254644 Glad it made sense.

That’s the idea, just trying to look beyond what everyone is tracking right now and focus on what is actually building underneath.

Let’s see how it plays out.

English

@ThinkWithSaurav Beautiful. You are musician with analysis. What a flow 👌🙏

English

Exactly right.

It is not just fear stopping them. It is familiarity. They know HUL. They know HDFC Bank. They know Infosys. The unfamiliar feels risky even when the fundamentals are stronger.

But every bull market in India since 2003 has followed the same pattern. The next cycle rewarded the sector solving what India needed most at that specific moment. Infrastructure in 2003. Consumption in 2012. Specialty chemicals in 2016. Defence and grid in 2020.

Right now India needs energy security. Battery independence. Food security. Strategic manufacturing. The companies building those things have government customers who do not check Nifty before placing orders. Real order books. Real timelines. That do not depend on sentiment to execute.

The stocks most people are too scared to buy today are exactly the ones solving problems India cannot afford to get wrong.

That is always where the next bull market comes from.

Not from the stocks that already feel safe.

English

Next bull market won’t come from Nifty 50.

It will come from stocks you’re currently too scared to buy.

English

Yes, that’s a good shift.

Service side can add stability compared to pure equipment supply, and that jump in revenue does show early traction.

But still, it has to sustain. One year jump, hiring, MoUs — all good signals, but the real test is consistent execution and scaling of orders.

Let’s see how it plays out over next few quarters.

English

@ThinkWithSaurav Yes in cff even services of ships n submarines can play big role, earlier equipment supply only. Service revenue 5 cr in fy24 to 35cr in fy25. Employees increased 4 times. New 22 R&D team engineers. Mou tieup with Mazdock and Cochin shipyard. Lets see how things shapes up.

English

Look, there is no doubt that grid, BESS, battery chemicals, battery recycling, green ammonia all of this will play out from here, step by step, cycle by cycle. All you have to do is understand in which cycle what to expect, and what type of companies to choose inside that layer. You have to understand what can happen by 2028, then 2030. This is where you understand the cycle. See what is coming, not what is visible now. This war has created a problem, but it has also shown a much bigger direction to focus on.

But tell me one thing. When the war stops, which one moves more — specialty chemicals or fertilizers?

You have to think like this. It is not which sector will move. It is what problem the market will focus on after the war. Because sectors don’t move randomly. They move when a problem becomes urgent.

After the war cools down, what changes?

Right now the problem is energy supply, oil, inflation. After things settle, the problem shifts to rebuilding supply chains, reducing import dependence, and securing inputs like chemicals, fertilizers, and energy.

Now the question — specialty chemicals vs fertilizers.

Fertilizers is a short-term impact sector. It moves when supply gets disrupted, subsidy changes, or prices spike. After the war, demand stays, but pricing is controlled and linked to government decisions. So upside usually stays limited. Big moves don’t sustain unless policy changes. So fertilizer is event-driven.

So Deepak Fertilisers ? Paradeep Phosphates ?

Specialty chemicals is more structural. It moves when China supply issues come, when global companies diversify sourcing, or when India builds capacity. After the war, if companies try to reduce dependence on certain regions, supply chain shifts can benefit Indian chemical players. Margin and export story matters more here. Also think about battery chemicals in this space. So chemicals is a longer cycle, not an instant spike.

So it is not about where will the biggest move come, its about where will earnings actually change.

Because price follows earnings.

Now what I am seeing is this. A lot of you are still very focused on the defense sector, which is good from a national priority point of view. As I always say, focus on national priority-led sectors like defense. But what I am saying is, you also have to look at what the market has not discovered yet. This time is a good time to look for that.

If you look at the defense sector, most areas are already well discovered. But if you look at grid-related areas, they are still not well discovered because the problem has not fully come yet. It will start showing more clearly by 2028.

So somewhere here, logic and emotion both are working. You have to focus more on logic.

But if you still want to focus on defense, there are many companies.

1⃣

First is system, electronics, decision, doctrine, complexity-driven. These are the companies repeatedly discussed as structural compounders.

Astra Microwave Products — RF, radar electronics, EW, seekers, microwave subsystems. Role is detection and sensing.

Data Patterns — radar systems, EW systems, avionics, system-level electronics. Role is system ownership and integration.

Avantel — secure communication, SATCOM, naval and UAV systems. Role is communication backbone.

Zen Technologies — simulators, counter-drone, robotics. Role is training and application layer.

C2C Advanced Systems — command and control, sensor fusion, decision systems. Role is decision layer.

2⃣

Then comes volume-led, replenishment-led, high-criticality manufacturing.

Solar Industries — explosives, rockets, loitering munitions. Role is ammunition backbone.

Premier Explosives — propellants, rocket motors. Role is missile and propulsion.

Bharat Dynamics — missile manufacturing. Role is production and replenishment.

Paras Defence — optics, EO systems, electronics. Role is niche electronics and optics.

Apollo Micro Systems — embedded and missile electronics. Role is execution layer.

MTAR Technologies — precision components. Role is mission-critical manufacturing.

Azad Engineering — aerospace engine components. Role is precision manufacturing.

3⃣

Then there are companies which will do a lot of work as programs scale, but value capture is limited.

Centum Electronics — high-reliability electronics manufacturing.

Rossell Techsys — wire harnesses and cable systems.

DCX Systems — cables, kitting, integration.

AXISCADES — engineering services and design.

Sika Interplant — tooling and production support.

4⃣

Then the most important layer, where you have to decide your direction by reading them.

Hindustan Aeronautics

Bharat Electronics

Mazagon Dock

When you study these companies, you start understanding the ecosystem. Screener will not help you understand the cycle. You have to build that thinking.

So I have given you categorized companies. Now when you study them, you have to ask the right questions, because answers are available, but questions are missing.

Where does the company sit in the value chain?

Is it linked to initial orders or long-term usage and upgrades?

What problem is it solving?

Is that problem critical or optional?

Who uses it and who decides adoption?

Does its importance increase as complexity increases?

Can it be replaced easily or not?

Does it work across multiple systems or just one?

At what stage of the cycle does it become relevant?

What is management saying about future demand?

By the time you finish reading all this, you will feel this is a good way to think. You will find the right areas. You may even save it. But later you might forget.

So don’t just follow the process. Learn the process. Put the right thinking in the right place.

English

@ThinkWithSaurav Thank you for elaborating. Could you share "few newly listed companies" in Grid level solutions , quality power ?

English

How specific can you be while choosing a BESS company, and how do you give priority to your thinking and your process?

How will you decide?

There are two types of BESS — utility-scale BESS and C&I BESS. A simple way to understand this is by looking at the role they play and who actually uses them.

Utility-scale BESS is used by grid operators. Its job is to stabilise the grid and support large-scale renewable integration. It works like bulk storage for overall grid health.

C&I BESS is used by factories, commercial buildings, and data centres. The goal here is to reduce power costs, manage peak demand, and replace diesel backup. It works like a private power bank for site-level savings and reliability.

Now tell me which side you will choose, and what type of companies you will choose. This one question alone can filter most of the companies inside the BESS ecosystem.

If we talk about project size, utility-scale projects are large, often in blocks of 500 MWh or more. C&I BESS projects are small to mid-sized and are mostly behind the meter.

If you look at the utility BESS side, there can be payment issues. Receivables tend to be high, and cash flows can get stretched. Projects are large, but money comes with a delay.

If you look at the C&I BESS side, payment issues are usually not there. Cash cycles are cleaner. But companies in this space usually do not do everything in-house. They depend on partners for cells, PCS, EMS, integration, or EPC.

So after choosing the BESS side, the next step is to filter again at the company level.

You are thinking cells are the problem? You are thinking lithium prices going up will be the problem?

No.

That is not the real issue. Many companies have already fixed cell prices with suppliers. Most of them will pass through the price, so lithium volatility alone will not decide outcomes.

The real problem is something else. The question is, which company actually does everything except the cell? Do they design the system? Do they handle PCS, EMS, integration, controls, safety logic, and execution? Or are they only assembling parts sourced from outside? That is where the difference will come from. Not from cells, but from who controls the rest of the system.

Saurav@ThinkWithSaurav

BESS - Battery Energy Storage System You already know about this, what we need to think is where to focus and what to avoid. You must have already read that BESS is in an early stage in India, yes that is correct. You have also read that it is like the solar sector a few years back. Now BESS is in the same place like that, and in many ways the situation is similar. The question is, where to focus and what to avoid? Some companies will grow on volume but not in margin, so we have to see who can increase margin as well. What are the layers inside BESS? And in which layer is the real opportunity? You already know a few companies related to the BESS sector, and some of them look good. But knowing the names is one thing. Understanding where the opportunity actually sits is another.

English

Completely agree. Survival first. No portfolio question is more important than cash flow and job security right now and for many people this is genuinely the only thing that matters in this moment.

But for those whose survival is already secure here is the one thing worth adding. Gloom is not the time to chase returns. But it is exactly the time to understand what the next cycle looks like. Because by the time clarity arrives and good times are visible to everyone the easy part of the move is already over.

Every single cycle the pattern was the same. The returns went to the people who understood what India needed to build next. Not to the people who started looking after the news turned positive.

Right now this war has made certain things permanently urgent for India. Energy security. Food security. Battery independence. Strategic manufacturing. Things that were already being built before the first missile was fired. With real order books. Real government customers. Real timelines. That do not depend on the war ending to keep executing. Those businesses did not stop running because Nifty fell 2,400 points.

The next cycle is already visible if you know where to look.

English

People are asking about markets. Nothing wrong because your financial welfare is tied to it.

War is yet to end. Even now expert voices are saying it would take few years for global economy to recover. We don't know to the extent to which this conflict is going to escalate. War has to end first to assess the potential damage and future recovery.

Based on how things are moving on - a prolonged global recession cannot be ruled out. Each country and it's stock market are impacted in different ways, both on plus and minus sides. Too early even to gauge how much our economy and markets would be impacted. It may take time for clarity to emerge.

Not all stock markets would act or react in the same manner.

Now is not the time to focus on returns or notional losses, due to portfolio value going down. Focus on survival. Survival is based on human capital, your job or profession or business. Those who have sizeable safe money also can manage.

This is a wrong time to think about returns or growing wealth. The focus is on financial survival of your family.

During gloom, we may think good times would never be back. I've pointed out so many times. Life, economy, markets - everything is cyclical. Good times and bad times keep following each other.

Focus on your survival while waiting for the next good time to occur.

English