Alxi_Stock

36 posts

Alxi_Stock

@Tijd_Less

Tweeting about whatever comes to my mind. From BE.

Beigetreten Aralık 2020

335 Folgt55 Follower

@D27357 Read your update, didn’t see the QA transcript. Was at the poolside in a sunny resort, so decided to skip this one. Thanks for the work brother, I enjoy reading your takes.

English

@Tijd_Less I think they explained it very well in the earnings call - of course they might also just be making stuff & excuses up, but it convinced me at least. I transcribed the Q&A section on my Substack if you're interested.

English

I just uploaded my analysis of Chagee's Q2 on Substack:

open.substack.com/pub/fatumopes/…

Constructive feedback would be appreciated.

Summary:

This was a weak quarter & the outlook for the rest of the year is rather poor as well.

The main problem remains SSS (Same Store Sales), with -7% QoQ decline, which is an alarming 31% annualised, despite Q2 being seasonally stronger than Q1, although this can be mitigated by an issue that is temporary (*1).

At the same time core operations remain at strongly profitable & at least some part of the currently poor performance is impacted by temporary headwinds, even though some problems are likely not temporary.

My longterm investment thesis remains intact, although somewhat bruised.

Nonetheless I still have conviction about the long-term potential & trajectory of the company.

I will therefore stay significantly invested, but am considering rotating partly into other stocks, as the outlook for at least the next two quarters is rather poor - likely similar to this quarter - and I still see some very interesting opportunities in the market that might perform better over the next 6-12 months. I currently hold ca. 13.5% of my stock portfolio in $CHA at a cost $ average of $23.84.

English

@ReturnsJourney Source for Didi?

Isnt it the safest ride hail platform in the world?Multiple layers of safety implemented in the app. Police is 1 click in the app away. Mandatory video en audio recording. Harder to alter route.

Your point about the drivers?Could be true no expertise on this.

English

I heard good conversations with $Uber drivers that the main advantage of Uber In Emerging markets, at least where I am, is the safety. They pause your account when your car insurance is expired, they ask you for daily photos to prove that you are the account holder driving the vehicle. They are very serious and focused on safety.

Other apps like didi don't, irregular immigrant drivers take the place of registered drivers and customers, especially women, fear for their safety, and the occasional crime happens.

Just 2c from the ground

$uber

English

@D27357 @MikeFritzell Honesly, not sure tbh, I visit mostly leisure locations.

But I asked a friend this Q who works in Shanghai. He said: Chagee is chain for basic bitches right?

But there is a Chagee in his office building though so probably both.

English

Thanks for sharing!

What would interest me is whether Chagee is in your experience only focused on leisure -

or also positions itself in the daily routines on workdays, which is dominated by coffee.

Are the stores only positioned in malls in similar spaces - or is there also an effort to attract the work/productivity crowd with stores in district businesses, with tailored products, eg pure tea?

That could be a huge opportunity imo

English

@shravanrayhaan @MikeFritzell I see. Mixue is indeed world domination but wouldn’t work in the west. We are more health conscious and bigger high middle class.

Mixue is beast in itself. Vertically integrated and killing in SEA too. Currently don’t own it, but wouldn’t mind to. I own $cha and $lkncy.

English

@Tijd_Less @MikeFritzell I was talking from betting on a stock with world domination perspective.

English

@spybear180 @MikeFritzell You’re right. There is, albeit smaller than in the coffee sector, a price war going on. Delivery sector the worst.

-SSS decline

-Vietnam launch no succes

-No one knows the story

-Chinese discount

-Highly competitive sector

I started buying around $25 and down.

English

@Tijd_Less @MikeFritzell I meant they’re caught up in it, not directly involved.

Otherwise why’s it down?

English

@spybear180 @MikeFritzell $Cha doesn’t participate in price and coupon wars, as it doesn’t have to (currently)

Hence the fat gross margins.

English

@MikeFritzell But people pay premium for their thee, and happily wait 45 minutes for their drink and rather don’t throw the cup away when finished.

Competitors are (currently) not in the same league.

Then again: TikTok brain of younger generations can make changes fast in consumer taste.

English

@MikeFritzell To add to this:

The appeal of Chagee is the design and lifestyle vibes it gives. Middle class girls walk around with the cup all day to show off to the world.

Is this the best moat in a highly competitive space in which I can name 8+ large players? That’s debatable ofcourse

English

@shravanrayhaan @MikeFritzell Mixue is not even remotely close in the same category tbh, though a great company. Same sector though.

English

@MikeFritzell Are you saying it can beat mixue?

Also $cha maybe having a Chinese adr perception problem

English

@DutchInvestors $LKNCY already has 4 stores open in NYC, and some in SEA.

But when you visit China or understand the Chinese consumer, you’ll instantly realise why Starbucks China is doomed. Chinese are highly digitalised, prefer speed/automation and like discounts. This is Luckin, not SB.

English

A new kind of coffee war is brewing. While we all know Starbucks, their Chinese competitor Luckin Coffee is showing some serious speed.

On average, Luckin Coffee opened around 16.7 stores per day in 2024. The company is currently half the size of Starbucks, but it has a 5-year revenue CAGR of over 60%, showing just how rapidly it's expanding.

#LuckinCoffee #Starbucks $SBUX $LKNCY

English

@SoJustFollowMe @MMoney642 LK management got fired for the accounting fraud.

Then it rebounced while opening from 3000 stores to 25.000 + right now. Being highly profitable and efficient. Its stock also went from the lows of 1 dollar tot 38 dollar as we speak. $cha $lkncy

English

@MMoney642 $CHA is that the Chinese tea chain running a $SBUX-style model?

Full disclosure: I don’t know much about it. But I do remember the last coffee copycat - Luckin Coffee - which went bankrupt in June 2020.

I’d be cautious here, Andy 🙂↔️

English

Chagee Holdings ( $CHA) has the potential to be the next franchise powerhouse, and its valued like its going out of business.

Here is a high level summary:

MFM Key Metrics:

LTM revenue growth >12%: ✅ 98% YoY

LTM EPS growth >15%: ✅52%

ROIC >15%: ✅158%

LTD < 5 Yr FCF:✅ Yes

Share dilution <5%: ✅-5%

Company Specific Metrics:

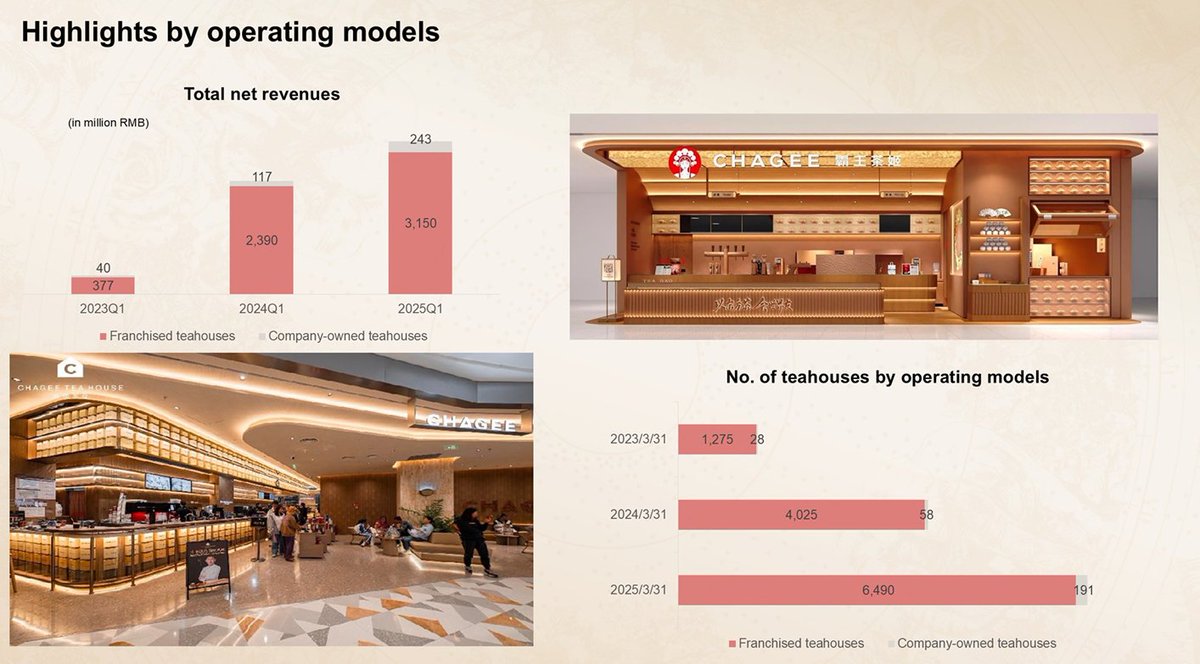

- 6,681 teahouses as of Q1 2025 – 93% franchised

- Very low closure rate of only 1.5% in 2024

- Over 192M total members (45M active) with +15M QoQ – crazy growth

- Over 90% of GMV comes from core tea latte products

- Same store sales down 19%, but offset by ~2,600 new stores added in the past year

Valuation:

$CHA trades at a pretty wild discount.

7x forward EV/EBITDA vs. industry average of ~19x

Take a look at the Fiscal chart below for reference. Yes, same store sales are down 19%, but that wasn’t the focus from management to date. The last two years were all about scaling the store base – and 2,600 new openings in one year speaks for itself. What a multiple for that expansion.

Future Outlook:

Management is now shifting operational focus from opening new stores to driving same store sales growth and overall performance. They have 3 main areas to focus on:

New product launches

Membership program push

Better store level efficiency

There is promise that this can be done. Before the massive expansion, mature locations were grossing high single digit to high teen growth. On top of that, international expansion is still a big part of the plan.

Reasons to Buy:

- Strong International Intros: US and Singapore stores are crushing it. Singapore averages $248K/month vs. OG China locations at $60K/month.

- Powerful Brand Engine: A scalable franchise model plus smart product innovation (like the low-caffeine line) keeps fueling brand momentum.

- Great Financials: ~+20% net margins, debt free, and strong cash.

- Valuation Discount: Like I already noted, trades at a massive discount to peers, leaving room for multiple expansion as the market catches on.

Reasons to Sell:

- Competition: Crowded market, consumer tastes change fast, price sensitivity is real.

- Product Concentration: 61% of GMV comes from just 3 SKUs. That’s risky if preferences shift.

- Macro Headwinds: Slower discretionary spending in China could hit growth.

- Execution Risk: Scaling this fast could make it harder to maintain brand integrity and quality, especially abroad.

Conclusion:

Chagee is going all in on expansion in a tough industry. Risks are obvious – discretionary spending, competition, product concentration. But the upside? You’ve got a strong brand, global momentum, and a stock trading at a dirt-cheap multiple.

If future product lines hit the way their core lattes have, this could easily be a multibagger just on rerating.

For EV/EBITDA comps in chart below: 1364 = Guming Holdings, 2097 = MIXUE Group.

Full credits to @Luce_On_TSLA for showing me this name! Go check out their page!

English

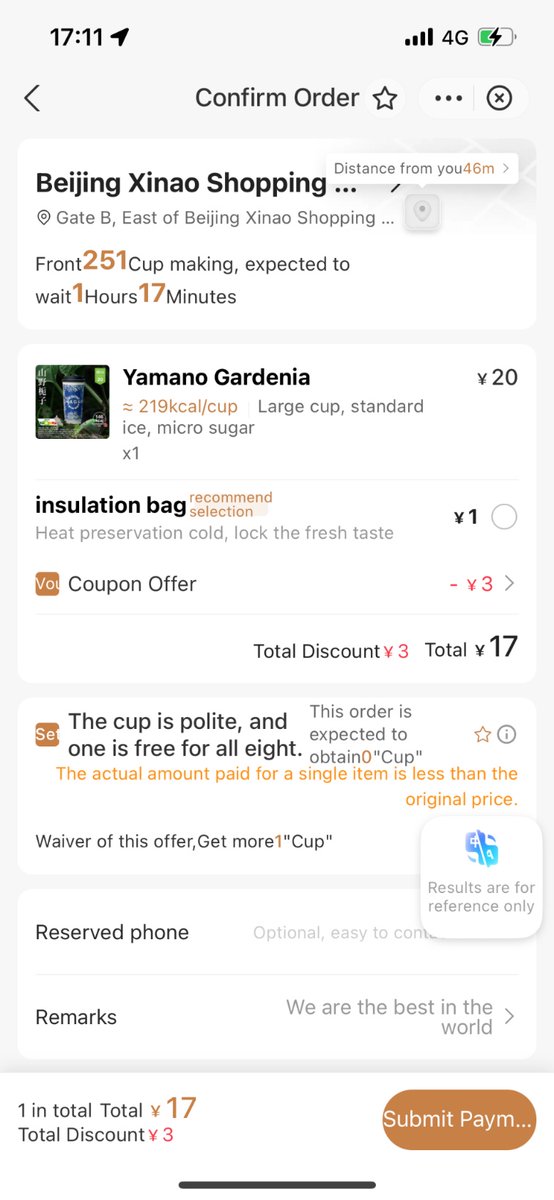

@MMoney642 @Luce_On_TSLA Here is some anecdotal evidence.

Stores are highly efficient and automated. But, there was a 1h queue when I got one yesterday, which was not even on a highly premium location. $cha

English

@Luce_On_TSLA $CHA is a company I will review in the next day or so

English

Today I prefer:

$GOOG over $MSFT

$UBER over $TSLA

$DAVE over $UPST

$BN over $BRK

$AMD over $NVDA

Would you say the same?

English

@D27357 Yes I have, many times only in CN.

Chagee is the number one player in up-scale tea. Its products are well liked by mostly middle and upper middle class. They are mostly on premium and B locations. I have limited characters on X, so DM me I’ll tell you more.

English

Have you tried CHA? Not available where I live unfortunately. How does it hold up against Heytea for instance?

CHA has plans to challenge coffee as daily work/productivity. Has a pilot with 11 stores of chagee NOW in Shanghai as far as I know, explicitly with that goal. Very interesting vision imo, but can't find a lot of info.

Do you happen to know more about that?

English

Bought more $CHA Chagee.

$KSPI Kaspi had solid earnings, as always, despite some macro headwinds.

I'm very excited to see what they do in Turkey once they get their banking license approved (apparently due in next couple of months).

Turkey has more than 4x the GDP of Kazakhstan. Kaspi is currently serving around 15mio people and is aiming to service 100mio. (Turkey has population of 85mio people)

Kaspi is highly profitable and CapEx-light; their net profit margin in Kazakhstan is 37.6%.

The e-commerce infrastructure of Hepsiburada is pretty good, but their margins and fintech & other services lack, so this could be a great synergy - Kaspi doesn't have to build the costly e-commerce infrastructure and can implement its Super app services with relatively little CapEx.

If they can successfully scale Hepsiburada into a dominant Superapp, as in Kazakhstan, with high profitability, the upside is very significant. Dominance, especially in e-commerce will be unlikely to be at the same level as in Kazakhstan, as in Turkey they have formidable competition from Trendyol; but potential is still huge imo.

Even without a banking license, margins, EDITBA have already improved for Hepsi in q2.

Kaspi's current pe ratio is around 8, so undervalued imo.

English

@Luce_On_TSLA CHA IPOed in the US because they want to become a ‘global brand’, not a Chinese chain.

Which is indeed a bold choice, but shows ambition. But honestly, if they IPOed in HK the stock would’ve done fire just like many other tea, sugar and coffee chains. We’ll see.

English

@pufferfishfin It’s similar to LK in a sense that they target the same audience in China.

Also LK is offering more and more tea products, while CHA isn’t going the coffee route.

The scale of LK is also insane, but CHA is quickly getting there.

I own both.

English

Taking a look at $CHA today, the Starbucks of China. Wondering if this has any similarities to $LKNCY so let's take a look.

So far, $CHA is down 50% from the IPO day peak, which questions whether this is getting into value territory, or just another mispriced IPO. (1/11)

English