Angehefteter Tweet

Asset light industrials with low Capex to Free cash flow (2025)

$6920 - Lasertec: 4% 🇯🇵

$CGNX - Cognex: 5% 🇺🇸

$BMI - Badger Meter: 8.5% 🇺🇸

$AME - Ametek: 8.5% 🇺🇸

$GGG - Graco: 9% 🇺🇸

$NDSN - Nordson: 9% 🇺🇸

$DPLM - Diploma PLC: 10% 🇬🇧

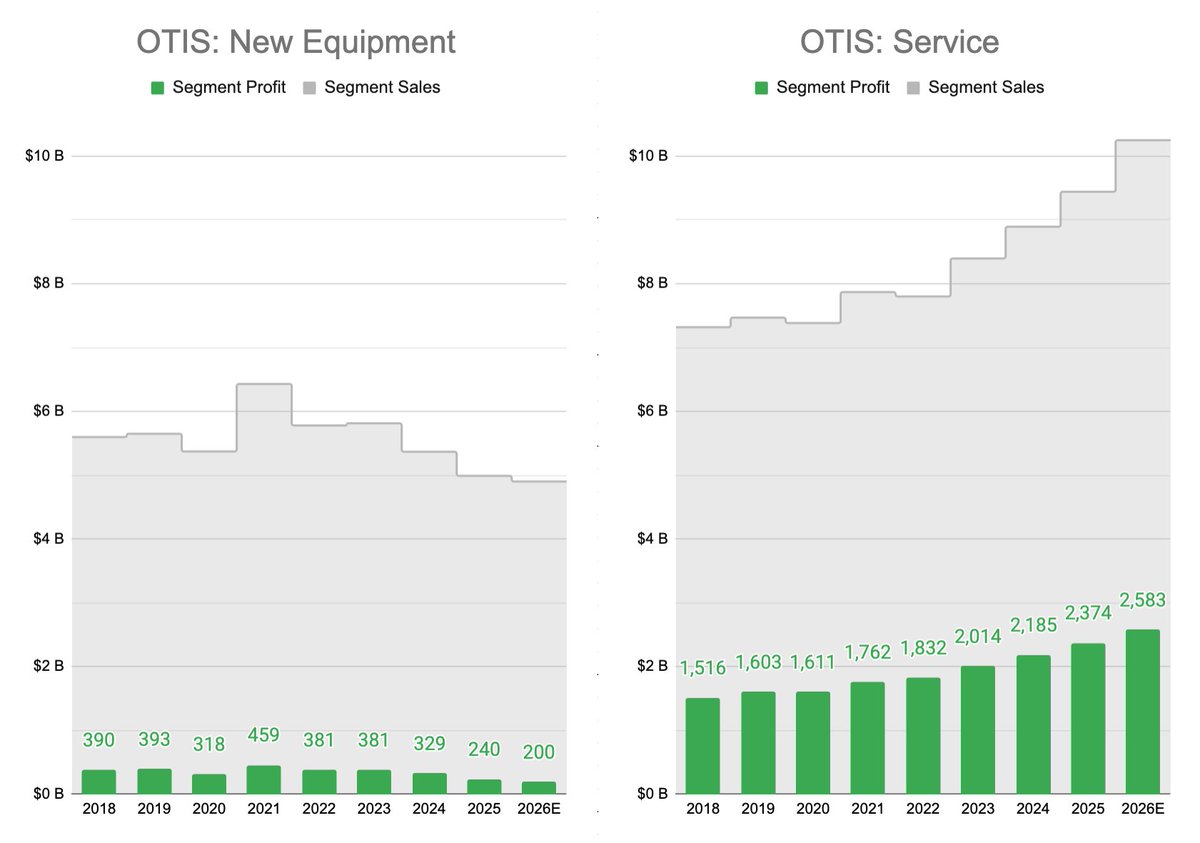

$OTIS - Otis: 10.4% 🇺🇸

$HEI - Heico: 11% 🇺🇸

$GTT - Gaztransport & Technigaz: 12% 🇫🇷

$EMR - Emerson Electric: 12.4% 🇺🇸

$KNEBV - Kone: 12.5% 🇫🇮

$LRCX - Lam Research: 13% 🇺🇸

$ITW - Illinois Tool Works: 13% 🇺🇸

$ASABY - Assa Abloy: 14% 🇸🇪

$IDXX - IDEXX Lab: 15% 🇺🇸

$PH - Parker Hannifin: 15% 🇺🇸

$VRT - Vertiv: 15% 🇺🇸

$INDT - Indutrade: 15% 🇸🇪

$HLMA - Halma: 17% 🇬🇧

$MTD - Mettler-Toledo: 18% 🇺🇸

$ATCO - Atlas Copco: 20% 🇸🇪

English