Sabitlenmiş Tweet

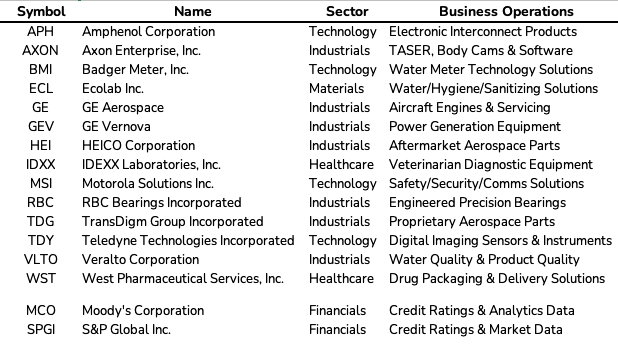

Here's the current state of the Durable Value Creators investable universe. Spent some time recently narrowing down the focus.

Primary themes include picks & shovels of secular trends, recurring revenue, razor-razorblade model, mission-critical, and/or relatively asset-light.

English