@aleabitoreddit @StephanC86 I think it’s time to get back into $CRDO

English

Avery

2.4K posts

@TrueWealthAngel

Investor in High-Quality, Fast-Growing, Under-Valued Businesses. Join me in finding Rare Gems 💎 that have a 10x Potential 📈. NFA.

$SIVE is now up +73.78% today ($231M MC). As markets price in information synthesis of the next potential $LITE of photonics. If I had to explain the difference: One laser source in Lumentum primarily benefits from current optical bottlenecks. The other in $SIVE is for the upcoming CPO/Silicon Photonic bottleneck. Lumentum is largely benefiting right now from $NVDA and hyperscalers securing capacity of EML lasers for current pluggable optical transceivers cycles. As seen with the current EML bottleneck, hyperscalers are buying out any 800G/1.6T transceiver + upstream capacity from: - $AAOI (in-house) - $COHR, $LITE (EML lasers + design) -> $FN (assembly) - $COHR, $LITE (EML lasers) -> Innolight / Eoptolink What's next? Silicon Photonics and Co-Packaged Optics. The architectural shift to CPO requires massive arrays of high-power CW DFB lasers. And this would likely trigger a complete, sudden paradigm shift in volume demand. $SIVE benefits from InP CW DFB lasers for SiPh and CPO: The up and coming companies like: $AYAR, $POET source $SIVE lasers, but primarily do advanced packaging. Then they feed up to larger companies like $MRVL Celestial (that buy $POET's interposers). However, if you go upstream, the light source is $SIVE. CW DFB lasers are light engine ( $SIVE ); the silicon photonics package ( $POET and others) is how it gets transmitted. CPO scale is not there yet. But we know it's coming. And as seen with current optical transceiver cycles: - Light sources from $LITE and $COHR demand much higher valuations than companies like $FN that focus on advanced packaging. Markets have been focusing on $POET, but missed where they get the actual $LITE type light source for Starlight. The risks are present including facing multi-source competition with $LITE, $COHR, $AVGO, and others. So again, make sure to do your own research. But my argument against that: Sivers been early enough to tailor custom lasers to fit $POET, Ayar, and other specifications before they got popular (sort like the $POET to $MRVL Celestial analogy). There's volume risks as well: But the potential Win Semi qualification offsets that. Dilution risk to scale capacity, is always present with every early-stage company as well. I did my thesis on $LITE last year and still love the stock for Google TPU ramp/OCS. But this year, I'm focusing on: $SIVE, as my personal CW DFB laser exposure for the new photonics architectural shift. I’m sharing my own thoughts on capturing the rotation from the current EML cycle to the upcoming CW DFB/Silicon Photonics cycle.

$SIVE +200% something in only 2.5 weeks all credit to @aleabitoreddit, made me more than I made in crypto past 5 months

$VIAV just smoked the print. > Revenue $406.8M vs guide of $386M to $400M. > Non-GAAP operating margin 21.0%, above the 19.7% guide. > Non-GAAP EPS $0.27 vs guide of $0.22 to $0.24. > Revenue up 42.8% year over year. Non-GAAP net income up 99.4%. This is the testing layer of the AI buildout doing exactly what it should do as 1.6T ramps.

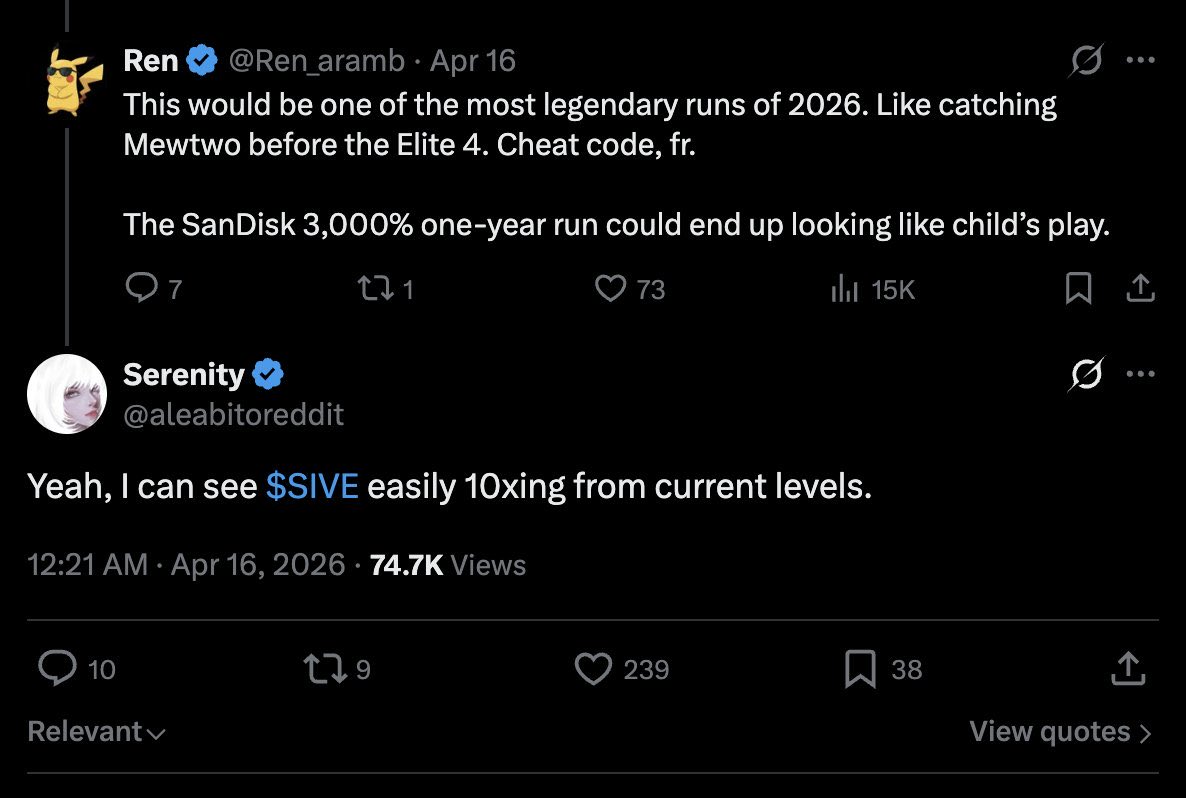

Serenity might be investigated by the NASDAQ 🧐 @aleabitoreddit - $SIVE