Some random thoughts on the hard rock pegmatites as I sip my morning coffee.

Nobody seems to be talking about the price of Tantalum which has just reached its highest price in 20 years.

A lot of hard rock lithium companies produce Tantalum as a by-product. It’s a relatively rare metal that occurs in small quantities in pegmatites. Most deposits have an average grade of around ~130ppm Ta. It’s quite easy to concentrate given just how heavy it is compared to spodumene and the typical pegmatite associated deleterious elements. Tantalite a specific gravity of ~8 whereas spodumene comes in at ~3.1. However, its worth noting, like all metals and minerals, some deposits will have higher recovery rates and better metallurgy than others.

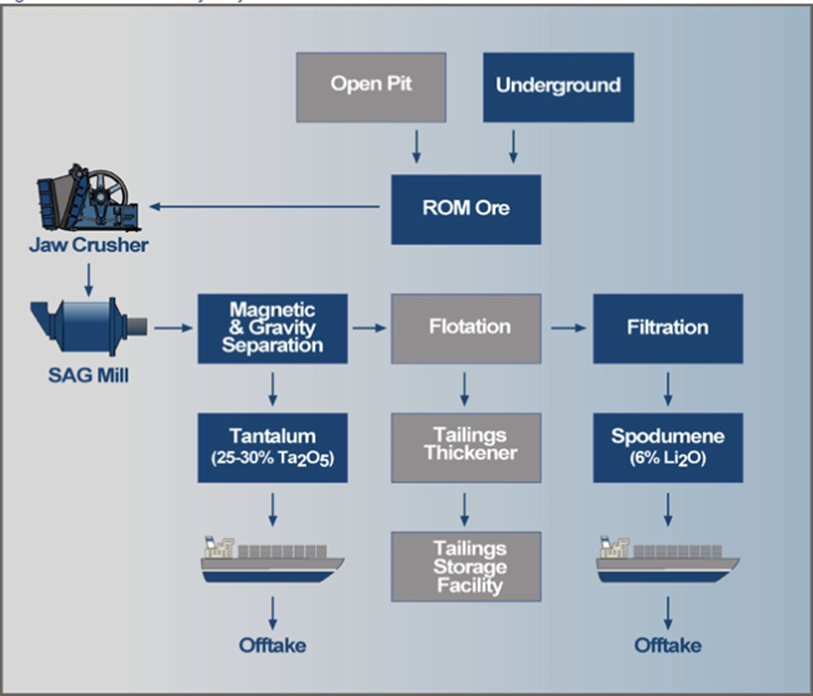

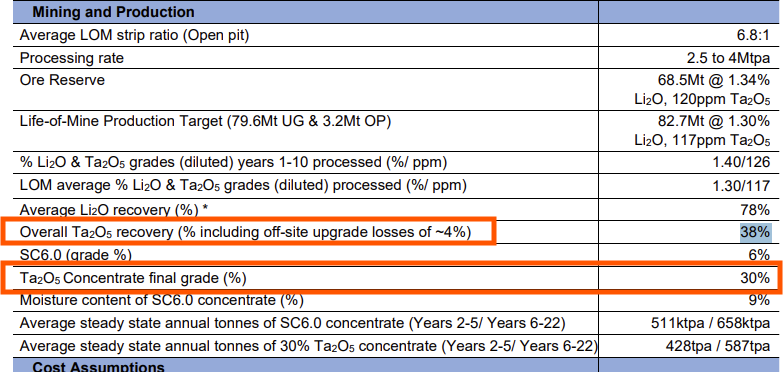

As you can see on the diagram below, given just how heavy it is, and also that it generally contains iron, it can be removed before the flotation step with gravity and magnetic separation. The recoveries are generally quite low (I note LTR’s came in at 38% in their DFS - not sure what they are in operation).

Whilst it’s low, it’s not bad for a by-product and such a simple and relatively low cost process (magnetic and gravity separation after SAG). I’d imagine it would be relatively straight forward to increase the recovery rates. For example the grind size is optimised to suit the spodumene as it’s the main game. If the tantalum price increases enough I’m wondering if there’s a sweet spot where you’d ideally tweak the grind to suit the tantalum recoveries a bit. Although I’m not sure what tantalum price you’d need to warrant that.

Companies generally list it as a credit against the operating costs. In LTR’s DFS for example, they were estimating a US$48 credit per tonne thanks to tantalum concentrate sales. Which equates to a tantalum price somewhere around the ~US$84/lb CIF China mark.

The current price of >30% Ta2O5 concentrate is $US260/lb (this is per contained Ta2O5). So to run through an example, last half yearly, LTR produced around 591dmt of Tantalum concentrate, which equates to 1,302,930 pounds. However, this would come out as a 12% graded product as stated in their DFS and is further upgraded offsite for a 4% loss. So total contained Ta2O5 would be 1,302,930 * 12% * (0.96) = 150,098 lbs of Ta2O5 per half year.

So if you crunch the math, 150,098 x ~$US230(rough realised price) x 1.43(US to AUD) x 2 = ~$A98.7 million annually. It starts to become quite a significant credit, especially if you take into account the simplicity of concentrating it. I'm not sure of the offsite concentrating costs and its not listed anywhere. I'd imagine its still largely magnetic and gravity based so shouldn't be overly high relatively speaking compared to other processes.

If the price of Tantalum continues to increase, you would think companies would start to implement/tweak processing to increase recoveries given how low they are. 38% is quite low if you ask me (using LTR as an example) and I'm sure there would be ways to increase this without hurting the spodumene output. Just a benefit hard rock mining has over brines! Maybe some of the smaller lithium players could look to implement a small scale WHIMS, etc. and start concentrating tantalum to raise early stage cash?

If the price of spodumene holds above US$2000, and you throw in a juicy tantalum credit, you’re going to see some pretty decent quarters for lithium producers I'd say! Thanks for reading!

English