daando37 retweetledi

daando37

4.3K posts

daando37

@daando37

side quest. always dyor. all my takes are no financial advices.

Deutschland Katılım Ocak 2021

859 Takip Edilen1K Takipçiler

good work as always @sparkes_dwayne

for anyone who wants to understand the $LAC flowsheet:

x.com/i/status/20075…

Dwayne Sparkes@sparkes_dwayne

With sulfur prices this high, the costs of processing lithium clays, oxide ores (copper, nickel, REEs) is going to BLOW OUT. The smelting of sulphide ores produces sulphuric acid as a byproduct. The processing of oxide ores consumes sulphuric acid. #LAC's Lithium America's Thacker Pass for example is going to do 40,000 tonnes per year of carbonate in phase 1. They've stated a 2250t/day sulphuric acid plant, which is 821,250 tonnes of acid per year. So each tonne of carbonate could require 20.5 tonne of sulphuric acid per tonne of Li₂CO₃. That's about 6.8 tonnes of sulphur. Using the Chinese futures price of US$1050t, that's US$7140t worth of sulphur per tonne of Li₂CO₃. #LAC will most likely source their sulphur internally. American fertiliser companies during Q1 paid US$488/t for molten sulfur, which is $3318 per tonne of Li₂CO₃. I'd imagine its higher now looking at the Chinese price. Spodumene uses 50-60% less acid. Food for thought. I love spod.

English

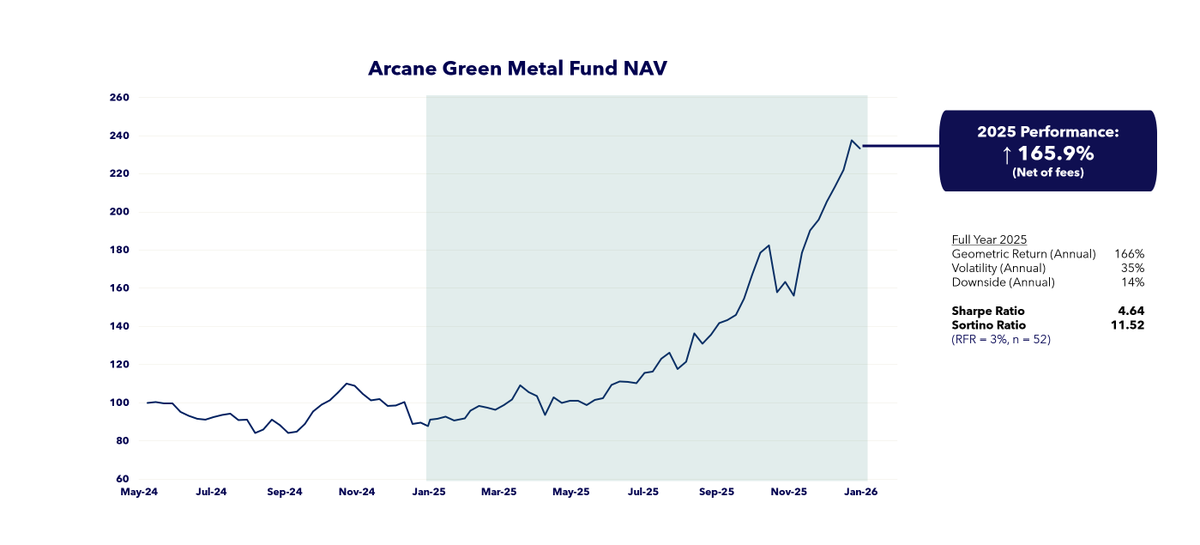

Hoping to keep this run going. Last year the Arcane Green Metal Fund that I manage returned 165.9% net to investors, driven by mostly #silver and #lithium. The resurgence in Lithium this year continues to drive our performance and I still see gold/silver doing well this year.

Legal: The Fund is open to Accredited Investors only.

English

it's not sodium vs lithium. it's lithium w/ sodium.

daando37@daando37

sodium debates are mostly narrative debates. stationary can grow fast, visible & still not touch lithium prices.

English

@sparkes_dwayne @Eagleresa treating bridge money like fid money is how retail ends up applauding its own dilution before the hard part even starts.

English

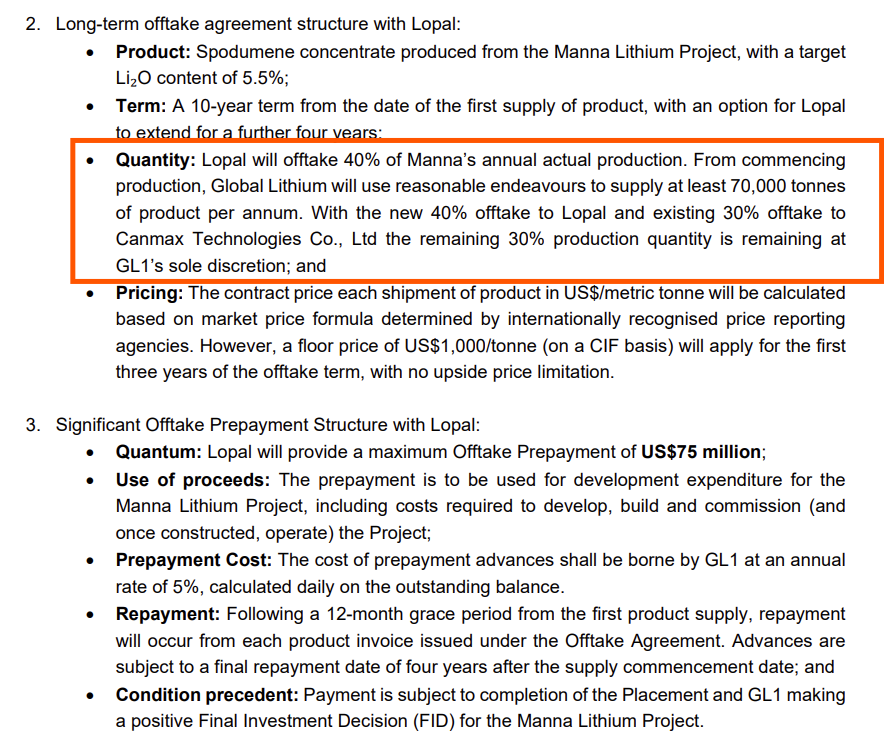

@Eagleresa GL1 need a float according to their DFS. How far will 75mill travel?

English

Give us 40% of your total yearly output of spod and we will pay for it now... You haven't started construction of your mine yet but that's ok.

Why doesn't Jiangsu Lopal Tech just source 70ktpa of SC5.5 from Manono North or from one of the many "mega" deposits recently found? Surely Zijin can spare a measly 70ktpa. Hmmm🤔

Floor price of US$1000 seems to be a common theme now.

Market tight. Bullish Aussie spod.

English

'but there's plenty of supply coming'. sure. capital has a way of exposing which tonnes are real & which ones are just conference slide decoration. the buyer is paying now for future australian spod instead of waiting for the miracle cargo from every overhyped pegmatite on the internet. this deal says the quiet part out loud: downstream doesn't want bedtime stories.

English

not much time today. so just a few quick thoughts about $QTWO $QTWO.V. this part matters.

a single connected system wins 'cause it kills the silent value leaks that show up later as operational surprises. coherent geometry is margin insurance. you're mining a plan, not chasing pockets & blending mistakes. that reduces the probability you end up designing the plant for the worst case, then paying that CAPEX/OPEX forever. cisco's model is explicitly framed as one continuous principal body, true thickness up to ~450 m/~1.8 km strike/drilled to >600 m & still open.

it also wins on scheduling physics. the more 'patchwork' your deposit, the more your mine plan turns into a stockpile management job. stockpiles are working capital. working capital is dilution. dilution is spec drift. spec drift is pricing power loss. a coherent, thick body gives you a shot at stable feed, stable head grade, stable fines curve, stable spec. nobody pays a premium for big. they pay a premium for big that behaves.

why it's already more underwritable at this stage vs a lot of early peers: you've got an actual mre & it's constrained by conceptual pit/ug shapes, w/ cut offs tied to a stated price deck. 295 mt @ 1.36% Li2O inferred (270 mt pit @ 0.40% cut off & 24 mt ug @ 0.70% cut off), w/ the constraints explicitly based on US$1,500/t sc6 (6% basis/fob bécancour). that's not economics, but it's already past the global tonnage headline w/o rpep filter phase.

then the boring but paid part: location reduces the number of heroic assumptions you need before you even get to engineering. they're stating 6.5 km to the paved billy diamond highway & ~150 km to the matagami railhead. plenty of early stage projects are 'big' on paper & still die on access/timelines/logistics friction. fewer moving parts makes the whole thing easier to underwrite.

the milestone stack is explicit: they're already talking updated mre later this year/baseline environmental studies/advanced metallurgy & a pea targeted '27. that's why it feels more investierbarer even w/ inferred tonnes: you can map the gates, you can price the risks & you're not guessing what the next 18 months is supposed to look like.

dyor. no financial advice.

Q2 Metals - Cisco Lithium Project@Q2Metals

💥NEWS: Q2 Metals Announces Inferred Mineral Resource Estimate on the Cisco Lithium Project with 295 Million Tonnes Grading 1.36% Li2O $QTWO $QTWO.V $QUEXF #Lithium Read the full press release here 👇: q2metals.com/news/q2-metals…

English

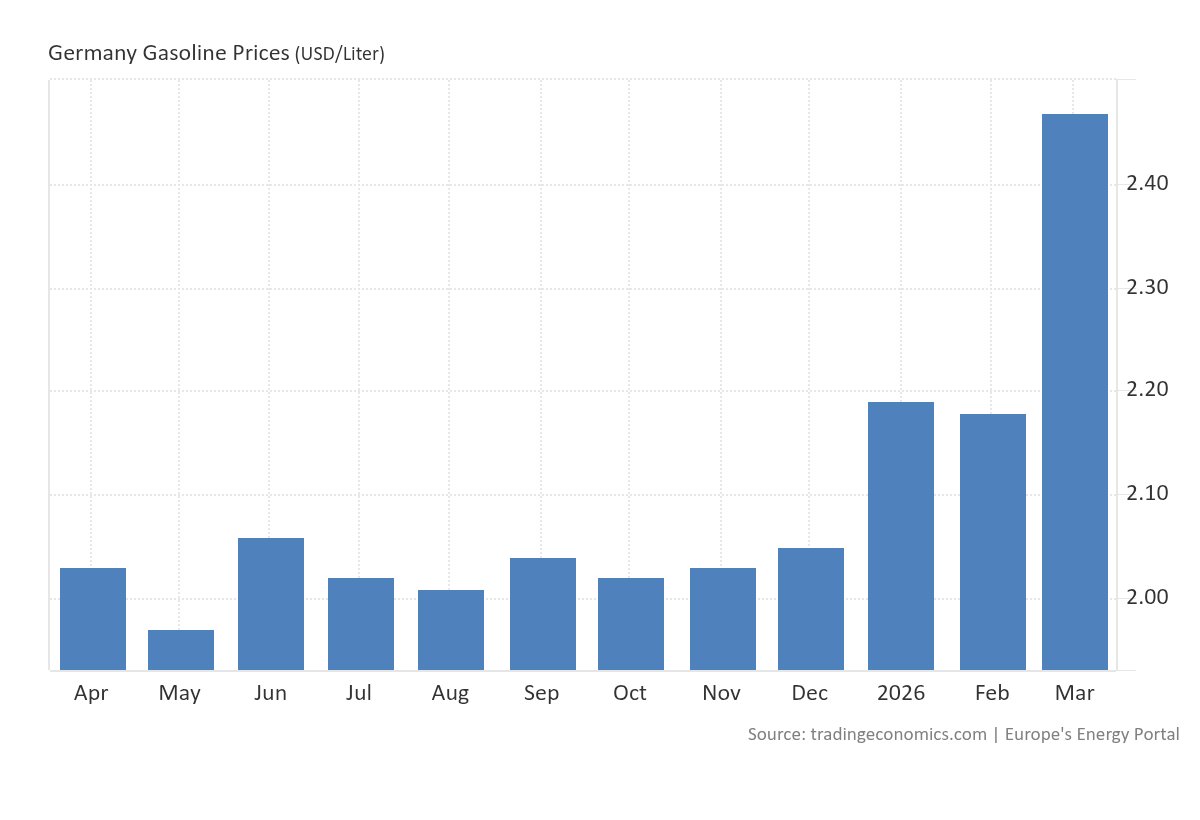

the part i enjoy most isn't being right. it's watching the same people who couldn't be bothered to care about the scenario suddenly talk about it like an unfortunate act of god. no. this was a visible chain: chokepoint stress, damaged flows, sticky risk premium, germany's tax stack & consumer squeeze. nothing mystical about it. & we're still early. the first move is at the pump. the uglier part comes after it bleeds into everything else.

daando37@daando37

same barrel. different tax stack. different pain threshold. at $194-276 brent, germany isn't dealing w/ an oil move. it's dealing w/ a consumer squeeze that turns political fast. the uk gets squeezed hard. the us still feels it, but from a much lower all-in base.

English

europe treats an energy shock like a fairness debate instead of a throughput problem. tax the producer. regulate the symptom. subsidise the voter. then act surprised when none of it fixes supply.

germany already burns extra fuel today 'cause the state let core infrastructure drift into congestion, bottlenecks & reliability problems. that is not theory. the council of economic experts says the poor condition of transport infrastructure is increasingly causing motorway congestion. in addition traffic delays rose in ~77% of german urban areas in last year (source: inrix global traffic scorecard).

so before the next shortage is even fully priced, part of the fuel bill is already being wasted by policy failure at home.

daando37@daando37

if energy is genuinely strategic, stop treating the companies that produce it like temporary atm machines every time policy failure hits the invoice.

English

if energy is genuinely strategic, stop treating the companies that produce it like temporary atm machines every time policy failure hits the invoice.

Energy Headline News@OilHeadlineNews

Five EU countries call for windfall tax on energy companies

English

the word 'collapse' is doing a lot of theatrical work here, but the underlying point is still right enough to matter. a sustained 7-11% hit to global oil supply is not some spicy macro subplot. that's the kind of shock that reprices transport, diesel, fertilizer, chemicals, food, freight & politics all at once. the argument over who breaks first is almost secondary. everybody gets poorer. some just find out faster.

PBD Podcast@PBDsPodcast

🚨 The Economy Cannot Survive the Strait of Hormuz Closing "The world economy cannot survive a 7 to 11% loss of oil supply. It will not survive" "We can debate: is Europe going to go first and collapse? Is Southeast Asia going to go first and collapse? Will America collapse first? But the global economy, it is a certainty, it will collapse if we keep oil supplies down 7 to 11%."

English

you're mixing product, pricing & timing into one clean number.

yes, phase 1 is lithium chloride concentrate, not carbonate. that's exactly why the dfs uses a lower realised price. but the study already bakes that in: ~$22.8k/t lce realised vs $29k carbonate (~78-80% payability). the '-25%' isn't a new adjustment. it's already in the model.

the bigger issue is elsewhere:

you're taking 5ktpa nameplate * utilisation * price like it's steady state. the ann literally says they start at ~4ktpa annualised, not 5ktpa. ramp up comes later. early revenue isn't 5,000 * 80% * sellable price. it's closer to lower throughput * lower recovery * higher unit cost.

& that's before you even touch:

- commissioning losses

- spec risk / rework

- working capital lag between pond to product to cash

also worth remembering:

the 10kt lce in ponds isn't 10kt that hits revenue. that's inventory inside the system, not saleable tonnes. so yes, licl vs carbonate matters. but the real error isn't the 25%. it's treating a staged ramp up as if it's already a steady state operation.

that's where most of the revenue disappears.

dyor. no financial advice.

English

@zahihajar @markjohnallen73 @daando37 @GalanLithium I believe their output will be lithium chlorides, not lithium carbonate so those numbers will need to be adjusted from $20K/t by ~25%. At 5,000tpe nameplate, that implies revenue of $65M at 80% utilization $GLNLF

English

so @markjohnallen73 the clean answer is:

known study inputs:

- dfs 1 opex: us$3,963/t

- dfs 2 licl sellable price: us$22,841/t

- dfs 2 carbonate reference: us$29,000/t

- implied payability: ~78.8%

clean dfs math:

- gross proxy: ~us$228.4m

- less dfs 1 opex: ~us$39.6m

- implied gross proxy: ~us$188.8m

that's a mathematical upper bound assuming the full 10kt converts from this point. it won't. even if you anchor to ~60% system recovery, you're talking ~6kt recoverable before pricing. & that's before ramp up dilution: 4ktpa start vs 5.367ktpa design = higher unit cost early. first product h1, first shipment h2 = inventory doesn't equal near term cash. that $188m number looks clean on paper. it doesn't survive contact with commissioning.

real world caveat:

- the 10kt is not saleable tonnage

- the missing variable is residual recovery from current pond inventory to payable licl. so us$188.8m is not a realised value, it's just a ceiling style proxy before ramp up reality hits.

dyor. no financial advice.

English

this is the part nobody wants to model honestly. it also explains why $GLN's share price discounts the study long before the market discounts the story.

the 10kt lce isn't 10kt you can sell.

it's basically lithium sitting inside the pond system, expressed as lce. gln's own conversion note says lce is just an equivalency measure & assumes 100% recovery / no process losses. so right out of the gate, the 10kt is an inventory metric, not payable tonnes. today's ann only says ~10,000t lce in ponds ready for processing by end april '26. it does not say 10kt saleable licl concentrate.

that's why you can't do simple math like

10,000 * lithium price.

wrong stage. wrong product. wrong shortcut.

the dfs gives you two useful anchors, but for different reasons.

for the cost side, i use dfs 1 opex (us$3,963/t lce). why? 'cause phase 1 is the relevant circuit for the current start up. that study is built around the initial 5,367tpa recoverable lce operation in the form of a 6% lithium chloride concentrate product. that makes dfs 1 the cleaner base case for what the first product is supposed to cost when it behaves.

for the top line, i would use dfs 2 payable/sellable pricing, 'cause that's the cleaner updated commercial assumption:

average lithium chloride selling price (us$22,841/t lce) vs a long term lithium carbonate price (us$29,000/t lce). that implies an effective payability of about 78.8% (22,841 / 29,000 = 0.7876). i use that 'cause dfs 2 is the later study, w/ the updated commercial framing for licl value.

so if you want a clean calc, before you inject any realism:

10,000 * us$22,841 = us$228.4m gross payable value proxy

then less dfs 1 opex:

10,000 * us$3,963 = us$39.6m

which gets you to a dfs clean gross contribution proxy of ~us$188.8m.

but here's the blindspot: that number still treats the 10kt pond inventory like it converts cleanly into recoverable, payable product from here. the studies do not give you that clean bridge. & the dfs itself tells you why.

phase 1 reserve assumptions used a combined recovery factor of 57%, made up of about 66% ponds & processing, 90% licl to lce conversion, then another 4% allowance for transport & operational losses. phase 2 is similar but updated:

global process recovery 61.65%, w/ long term pond recovery moving to about 68.5%.

more importantly, both studies make the same early ramp up point: in the first yrs, pond recovery is lower 'cause the system is still building its working inventory. early yrs pond recovery ~52.7% 'cause the system is still filling itself. that alone tells you pond inventory isn't sellable product. ponds are part of the machine, not the end of the machine.

so the right way to think about it is:

pond inventory * residual recovery from current pond stage to saleable licl * payable price minus ramp up adjusted opex on the tonnes you actually recover.

problem:

that residual recovery from 'where the 10kt sits today' to saleable product is not broken out separately in either dfs. that means anybody giving you one neat dollar figure is filling that gap w/ an assumption. & if you want to be honest, early stage opex is not us$3,963/t in practice anyway. today's ann says they start at only 4ktpa annualised, while dfs 1's cost base sits on 5,367tpa after ramp up. same broad fixed cost base, fewer early tonnes. so effective unit cost early should be higher, not lower. that's before you even touch commissioning inefficiencies, recovery slippage, off spec, rework or timing drag.

English

@LukeyTrags it proves the majors finally remembered they're not charity foundations.

English

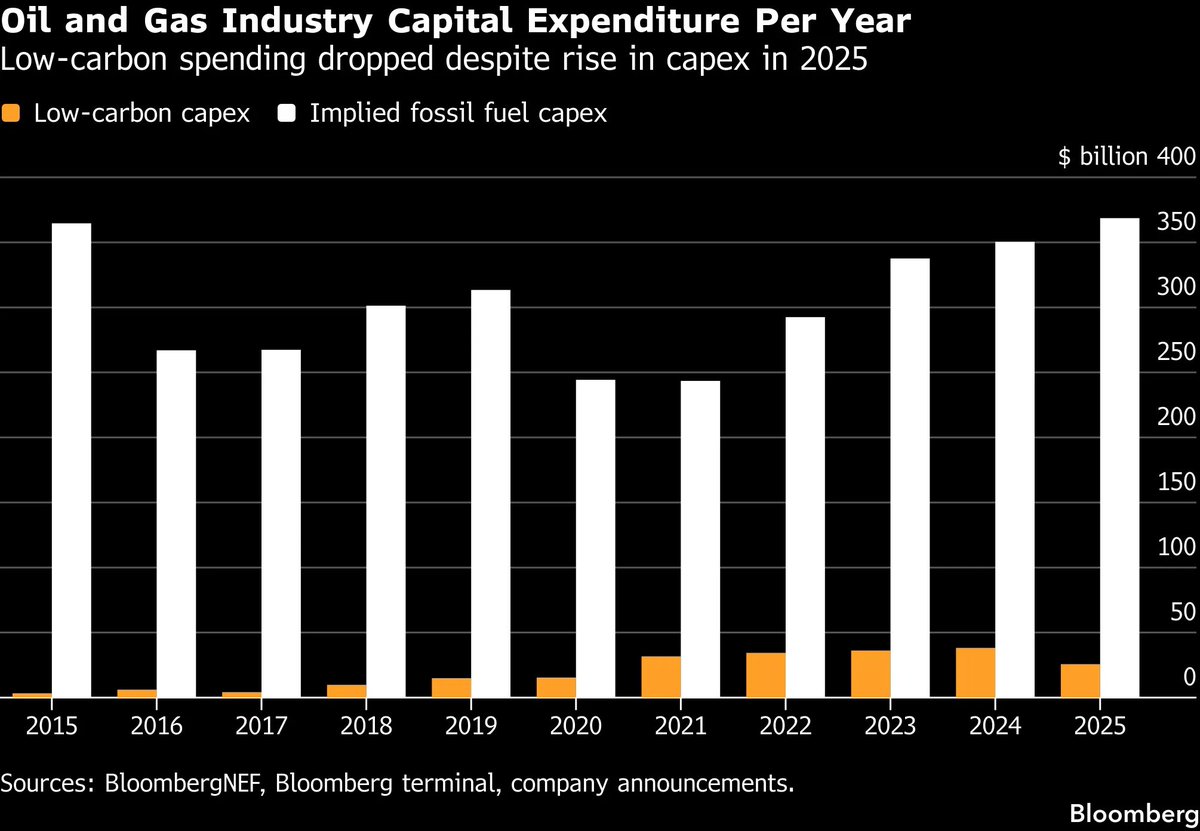

More proof the 'energy transition' has peaked globally.. #oil & #gas giants cut low-carbon spending by over 1/3 in 2025 - first drop in 8 years - down to ~$25B from ~$38B.. now just 6.5% of total capex.. reality hitting that renewables are subsidized fraud w/ better economics in core hydrocarbons.. shareholders + humanity wins when capital goes to real #energy.. $XOM $CVX $BP $SHEL $PRT $E $TTE $EQNR #OOTT #coaltwitter

Hydrocarbon@LukeyTrags

So $RIO.AX has quietly axed its 'big green dream', disbanded the dedicated decarbonisation team (slashing the budget from ~US$7.5bn down to just US$1-2bn out to 2030 similar to $BHP.AX), & folded the work back into the core commodity businesses.. another reality check & reminder that #renewables are fraud.. #coaltwitter $YAL.AX $WHC.AX $NHC.AX theaustralian.com.au/subscribe/news…

English

one of the very few accounts in lithium that feels like an upgrade to the feed. good to see him back on my timeline. @sparkes_dwayne

daando37@daando37

@elonmusk bring my brother @Sparkes_Dwayne back. thank you.

English