Hernan Lopez

3.5K posts

Hernan Lopez

@hernanlopez

Media & Tech Entrepreneur | Founder, Owl & Co, @WonderyMedia, @hernanlopezff | Founding Governor, @podcastacademy

Los Angeles Beigetreten Ocak 2012

1.4K Folgt5.1K Follower

Film was the first audiovisual language. TV was the second. Vertical video is the third; and it's worth $100B+.

Most of the industry still thinks of vertical as "short video" or "microdramas." That's like calling TV "soap operas" in the 40s; it misses the point. Vertical has its own grammar, its own economics, its own audience psychology. And most of the opportunity is still up for grabs.

In December, Owl & Co. convened an invitation-only Short Drama Business Summit: senior executives from major studios, talent agencies, dedicated vertical apps, tech platforms, and investors. Candid conversation, proprietary data, and the room left with a shared conviction: this format is real, and the opportunity both is larger than the industry has priced in.

For example, last year we predicted there would be vertical reality, vertical animation and vertical comedy. We did not quite anticipate all three genres would merge that quickly to create something like Fruit Love Island (186M views as of this morning, and a WSJ writeup).

On June 3rd, we're expanding that conversation with the Vertical Media Summit in Los Angeles.

What we'll cover:

→ The business of vertical: from IAP to subscriptions to ads

→ Why microdramas are just the beginning

→ Vertical news, sports, comedy, games, animation, and reality

→ Platform vs. studio economics

→ AI, production efficiency, and the cost curve

→ Global markets and the China playbook

This is a ticketed half-day event for senior operators, investors, and builders. Structured debate. Proprietary Owl & Co data. Limited seats.

THE BIGGER PICTURE:

→ Vertical is more than a format; it's a new language, and mastering it requires effort

→ The companies that learn it first will capture the most enterprise value

→ The window to get in early is closing

Pre-register: link in comments

English

English

Flattered/honored that our @SABEW honored our coverage of the Warner Bros deal with its best in business prize.

Also intrigued to learn that CNBC qualifies as a medium to small news organization.

English

@nielsen reversed itself on The Gauge within 24 hours. The story behind that reversal tells you everything about what streaming really competes for.

Nielsen was about to publish February data showing streaming would lose five share points to linear (nearly 10%) due to a methodology change that corrected for overestimated broadband-only homes. "Most" Nielsen clients had pushed for the change, but once Patrick C. at the WSJ reported the numbers on Thursday, someone must have complained loudly enough for Nielsen to delay the change until the fall.

Why fight so hard over a metric Nielsen itself calls "not a product"?

Because The Gauge isn't about ad rates, it's about perception. @netflix has cited its Gauge share in investor communications since 2022. @YouTube used the same playbook to drive the "YouTube is TV" narrative. The metric has been one perception-based signal influencing the reallocation of investor dollars from traditional media to streaming, and television dollars towards YouTube.

Though the Gauge doesn't drive ad rates, for most linear TV in the US the underlying Nielsen viewer counts do, and those were (and still are) going to reflect the new methodology in the fall. That's good news for @Disney, @ParamountPics, @wbd and @NBCUniversal which still make most of their advertising revenue from linear. For streaming, however, ad inventory is mostly priced on first-party data rather than Nielsen's impressions (with exceptions, eg NFL games).

The same week, Disney's new CEO Josh D'Amaro announced Disney+ will become the "digital centerpiece" of the company, a "portal" connecting stories, experiences, games, and films. This is Streaming Enterprise Value at work: using streaming to drive value in Experiences, their most profitable segment, not just as a standalone business. In a way, not unlike how Amazon and Alphabet leverage streaming to drive results across other parts of their businesses.

THE BIGGER PICTURE:

→ The Gauge has been great marketing for Netflix and YouTube: both used it to shape investor and advertiser narratives

→ Linear still drives the majority of video ad revenue

→ Disney is turning streaming into a new funnel for experiences, in addition to a content destination

More in this week's Streamonomics® (including So-ra long!). Link under my name.

English

Applications for the 2026 Lopez Fellowship are now open.

This is year six. Nearly 40 professionals have gone through the program, and up to eight will be selected this year. The Fellowship runs May through September: five months of executive coaching, mentorship, public speaking training, career architecture, and AI proficiency, at no cost (the program is underwritten by the Hernan Lopez Family Foundation). The only investment is your time (3-4 hours per week) and your commitment.

New this year: an AI proficiency test.

AI is fundamentally changing the relationship between managers, leaders, ICs and companies. We wanted to understand where applicants stand. To be clear: we're not looking for a minimum score, and we're mindful that some questions reflect your company's AI adoption more than your own. But the exercise itself is part of the point.

Coincidentally, an updated Anthropic Economic Index report was released today, covered in a great article by Axios about AI Fluency.

What the program includes:

→ 1:1 executive coaching with Cindy Shove

→ Group and individual sessions with me and senior industry leaders

→ Public speaking coaching with John Koch

→ Career architecture with Todd Gitlin

→ Enterprise-level AI training through Section AI.

→ Curated reading list

Who should apply:

You're a professional with 7+ years of experience. You've been promoted, taken on bigger roles, or founded a company that's raised outside funding. You currently work in tech, media, healthcare, education, finance, or another field entirely, based in the US. You've overcome real obstacles. You know there's a gap between where you are and where you're capable of going.

Applications close April 13th (Link in comments.) You will need to write a 2-page essay (not with ChatGPT; we can tell), submit your resume, an 'elevator pitch' in an audio file, your AI proficiency test results. Those who also submit a genuine, strong letter of recommendation from a boss, client, or colleague get noticed.

If you know someone who should apply, tag them below or comment for visibility.

English

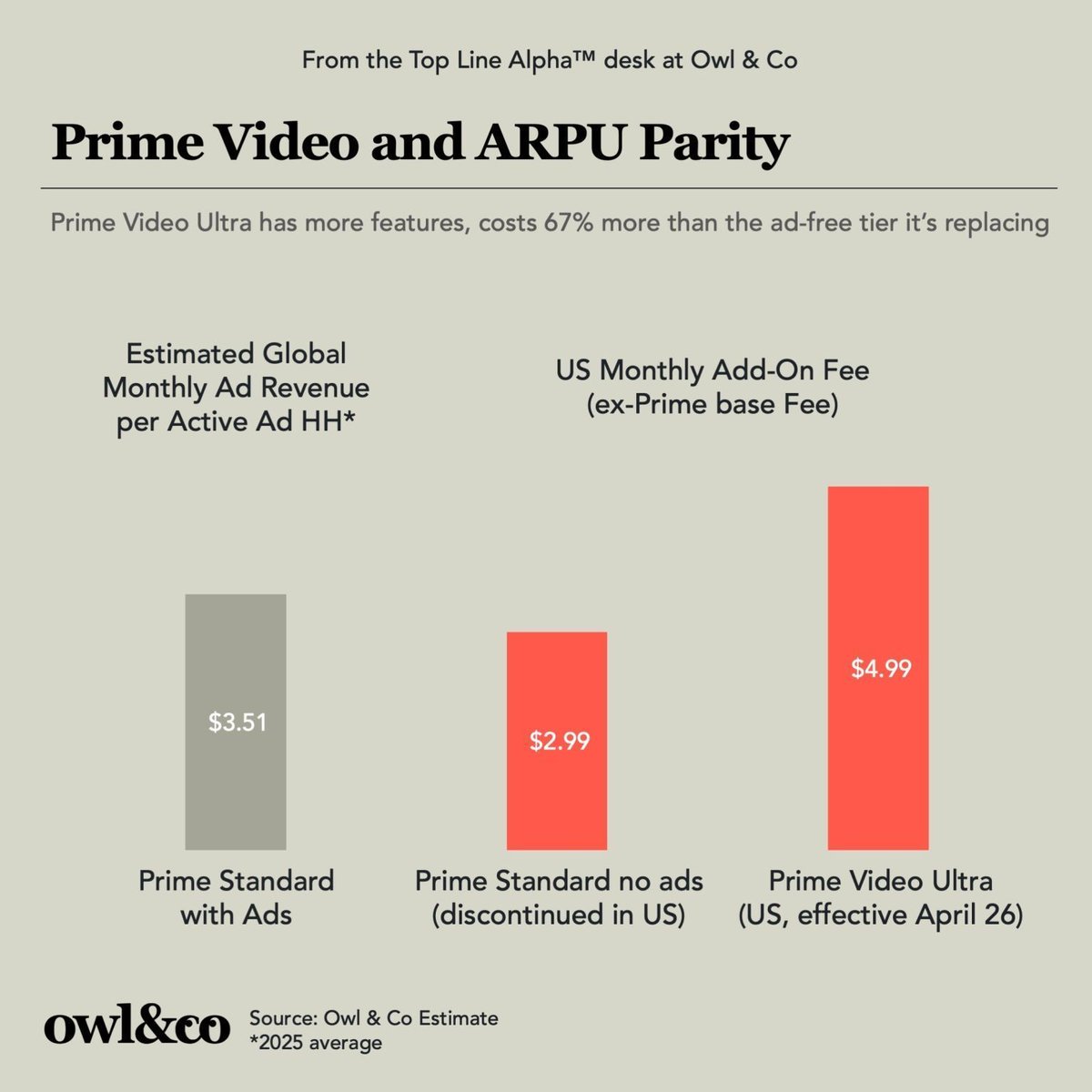

Amazon @PrimeVideo had a good problem. Ad revenue per active subscriber was running ~$3.50/month. But the ad-free tier cost $3. Every subscriber who paid to skip ads was costing them money.

How do you close that gap without triggering a backlash? Amazon had three options:

Option 1: Raise the ad-free price 67%, from $3 to $5. Predictable result: outrage, headlines about "greedflation."

Option 2: Introduce a new premium tier, offer them side by side: $3 for basic ad-free, $5 for premium ad-free (as most streamers have). Predictable result: very few people upgrade, more choice anxiety.

Option 3: Create a new premium tier, simultaneously retire the old one.

Amazon chose option 3. Prime Video Ultra launched at $5/month with 4K (now exclusive to this tier), Dolby Atmos, more concurrent streams, and more offline downloads. The old $3 ad-free tier is being discontinued in the US. Your options are now: Ultra at $5 or standard with ads at no extra cost over Prime.

This is behavioral economics in action. Consumers don't feel a 67% price hike when it's attached to a new product with new features. They feel like they're buying something different.

It's also a replay of the strategy Amazon used when it introduced ads in January 2024. Back then, they defaulted everyone into the ad-supported tier unless they opted out. Most didn't. Now, ad-free subscribers will default into the higher-ARPU Ultra tier unless they opt out. Most won't.

The result: ARPU Parity restored. Both paths (ad-supported and ad-free) will likely generate similar revenue per user. Important caveat: the ad revenue per active ad-supported household in this chart is my *global* 2025 estimate; US alone should be higher, especially in 2026. Prices are as published in the US, only place where the new tier has been introduced.

THE BIGGER PICTURE:

→ Pricing psychology matters as much as pricing math

→ Defaults are powerful: most people stay where you put them

→ Amazon isn't simply raising prices; they're restructuring value, and that distinction is everything

English

Applications for the 2026 Lopez Fellowship open March 24th. If you're thinking about applying, or know someone who should, now is the time to start preparing.

This is year six. Nearly 40 professionals have gone through the program. Up to eight will be selected this year.

The Fellowship runs May through September: five months of executive coaching, mentorship, public speaking training, career architecture, and AI proficiency, at no cost. The only investment is your time (3-4 hours per week) and your commitment.

What the program includes:

→ 1:1 executive coaching with Cindy Shove

→ Group and individual sessions with me and senior industry leaders

→ Public speaking coaching with John Koch

→ Career architecture with Todd Gitlin (Safire Partners)

→ Enterprise-level AI training through Section AI

→ Curated reading list

Who should apply:

You're a professional with 7+ years of experience. You've been promoted, taken on bigger roles, or founded a company that's raised outside funding. You work in tech, media, healthcare, education, finance, or another field entirely. You've overcome real obstacles. You know there's a gap between where you are and where you're capable of going.

The process is intentionally rigorous. Applications close April 13th.

One thing to do now: identify a current or former colleague or manager who can write a letter of recommendation on your behalf. Another new requirement this year: an AI proficiency test.

More details here:

buff.ly/5loKp8o

If you know someone who should apply, please tag them below or just comment for visibility.

English

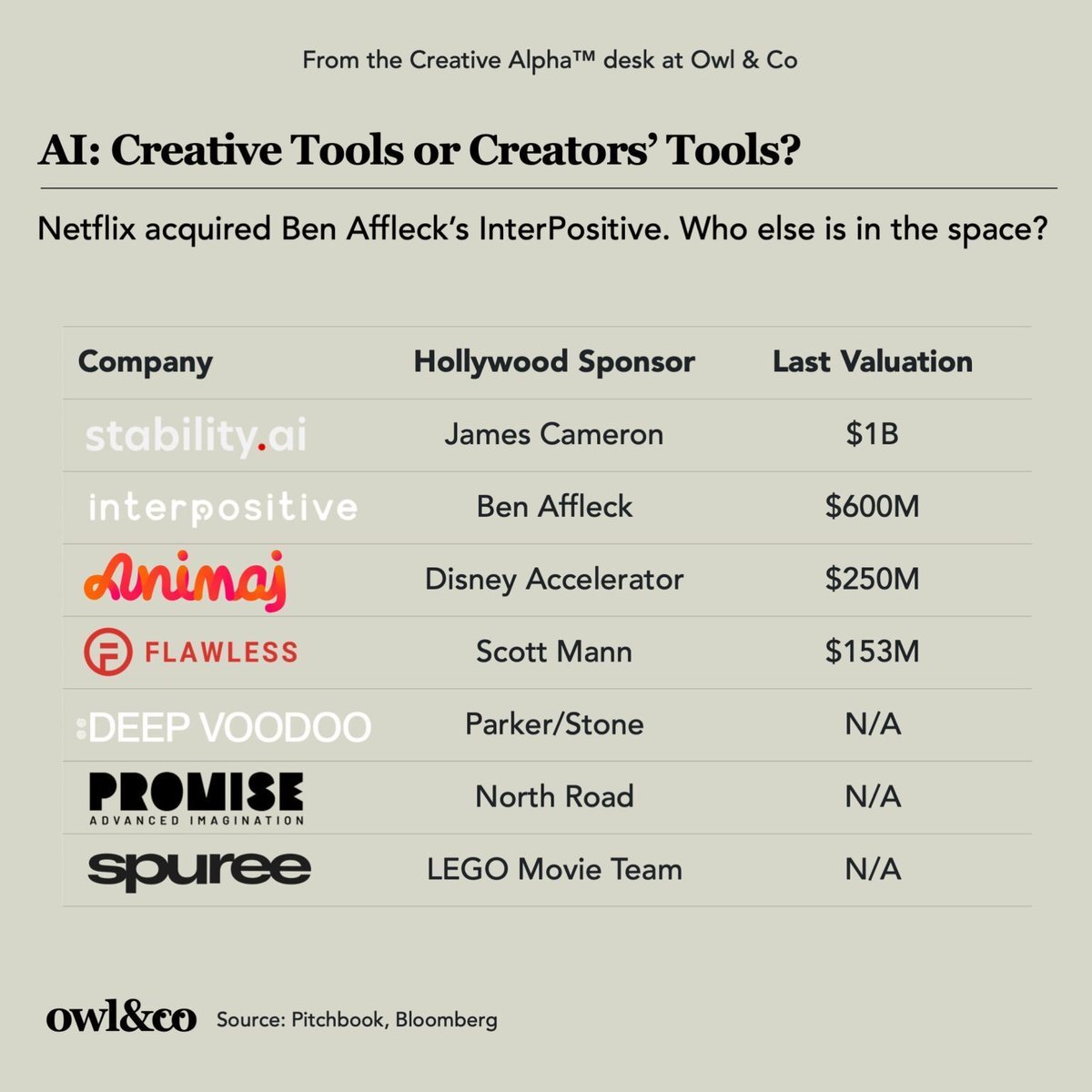

Hollywood is fighting AI while selectively funding it. @netflix just acquired InterPositive, Ben Affleck's AI filmmaking company, for up to $600M per Bloomberg. They're not alone.

James Cameron sits on the board of @StabilityAI (last reported valuation: $1B). The LEGO Movie producers co-founded Spuree. South Park creators Matt Stone and Trey Parker co-founded @DEEPVOODOO. Animaj received investment from Disney Accelerator. Promise AI is backed by Peter Chernin's North Road.

To understand the tension, it helps to separate four very different things that get lumped together under "AI." Erik Barmack at Reel AI lays out the first three categories:

→ Generative models (Sora, Midjourney, Seedance): Create entirely new images or video, often trained on copyrighted material. These trigger the loudest backlash.

→ Production tools: Clean up VFX, adjust lighting, synthesize ADR, streamline editing. Already embedded in filmmaking and increasingly embraced.

→ Synthetic performances: Digital doubles that allow an actor's face, voice, or movement to appear on screen without them being physically present.

I'd add a fourth: AI studios, companies using native AI tools while co-owning the IP they create.

As Erik puts it, "Hollywood's loudest outrage is directed at the first category. But the second and third categories are increasingly embraced — sometimes enthusiastically — by the same people signing anti-AI letters."

As for generative models, Hollywood is following a strategy that reminds me of UMG CEO Robert Kyncl's framework: "License, legislate, and litigate, in that order preferably." The 'preferably' implies that sometimes you need to litigate before you can license.

THE BIGGER PICTURE:

→ Hollywood isn't anti-AI; it's anti-uncontrolled AI

→ Studios and talent are aligned on copyright; that unity is rare and powerful

→ The path to working with Hollywood runs through licensing, not scraping; the companies that understand this will win

(Erik's article "Why did Ben Affleck start an AI company in secret?" is worth reading in its entirety: link in comments.)

English

Only two weeks ago, people were war-gaming a version of @netflix acquiring @wbd. Org charts and new deals were imagined. Some were nervous, others relieved or resigned.

In this week's Streamonomics®, I break down the "whiplash" moment: Netflix walked away, letting @ParamountPics win, and the anxiety spreading through Hollywood has two distinct sources.

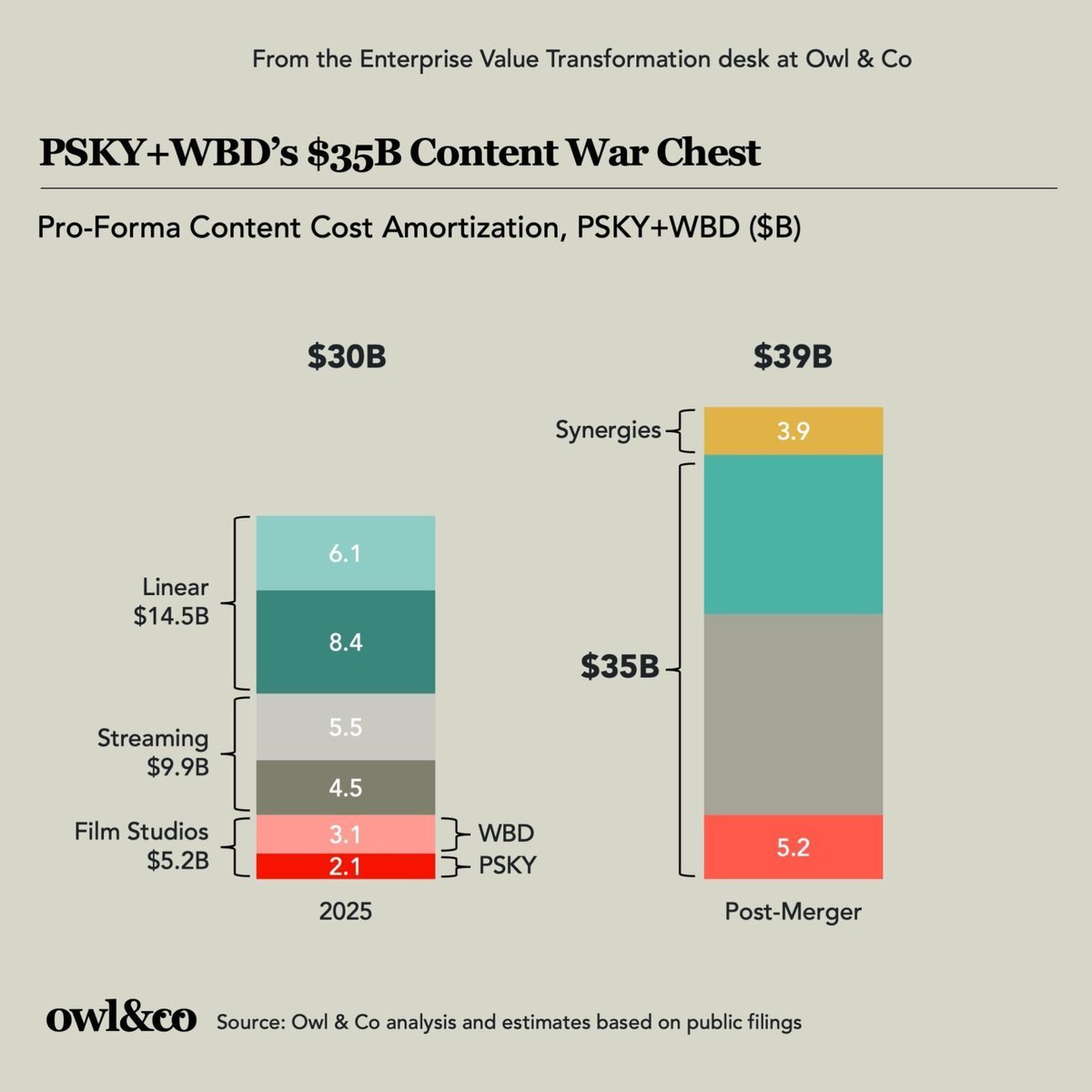

The first is structural. Paramount has promised $6B in annual synergies, but most of them have nothing do to with headcount. There's a simpler explanation: the combined PSKY+WBD entity will have a massive, hard-to-replicate library and a $35B annual content war chest after synergies, according to Paramount's statements in December (link in comments - the number likely reflects '27 or '28 forecasts, as both companies spent collectively $30B in '2025).

The second is timing. The announcement landed amid the SaaSpocalypse, Jack Dorsey's AI-powered layoff plans at Block, and early SAG/AMPTP negotiations. Hollywood is more focused on the latter, but investors and management are paying attention to the first two. A key question for everyone in entertainment and beyond: how does AI reshuffle the deck - for companies, investors, managers and ICs?

I spoke to people who know more than I do (including SectionAI's CEO Greg Shove) and got some answers, informed by several inflection points I've seen before. The anxiety in the industry right now is real, but it's not the main point. Disruption always concentrates opportunity in the people who moved while everyone else was still processing.

THE BIGGER PICTURE:

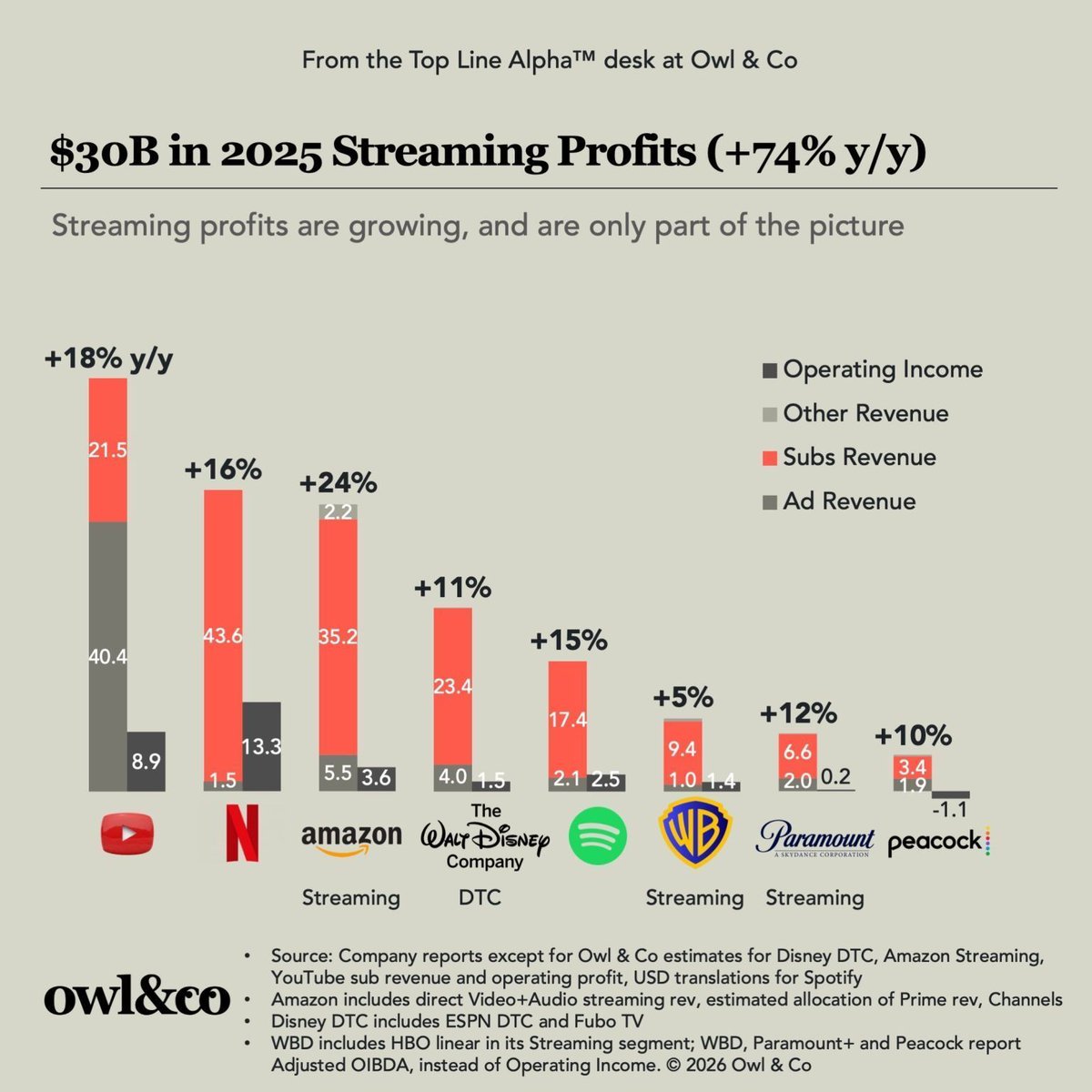

→ We estimate the eight largest streamers made a combined $30B in profits in 2025, +74% y/y

→ That number is a snapshot of an industry mid-reorganization: more profitable, soon more concentrated, more exposed to structural forces than the headline suggests

→ Paramount Skydance's statements in December help answer the questions about how much they expect to spend in content before and after synergies, and why the savings are likely to come from licensing and linear

→ AI proficiency is not a luxury

This issue also covers what analysts are saying about the P+/WBD deal, and why Netflix walking away may be a pricing gift to the entire industry.

Subscribe to Streamonomics® for free (link under my name). Owl & Co clients get it earlier, with exclusive data.

English

@netflix, @YouTube, @Amazon, @Disney, @Spotify, @wbd, @ParamountPics and @peacock collectively made $30B in profits from streaming in 2025: up 74% from '24. But what's behind those numbers and what do they signal for the future of streaming?

Barely 18 months ago, the consensus said "the streaming wars are over, Netflix won." I argued the metaphor was misguided: competition is perpetual because innovation is perpetual: either you do it, or the market does it for you.

At the time, Netflix accounted for the near entirety of collective streaming profits. Today, it still leads, but the field is closing in:

→ YouTube's subscription revenue grew 3x faster than advertising in 2025. YouTube TV (with Sunday Ticket), Music, and Premium are driving margin expansion. By our estimate, YouTube reached 67% of Netflix's operating income. (Alphabet confirmed subscription revenue "exceeded $20B" but does not report profits for YouTube.)

→ Amazon Streaming (Prime Video + Channels + TVOD + Audible + Amazon Music) turned profitable in 2025, driven by a massive step-up in advertising and growth in the highly profitable Channels business. Estimating their revenue requires allocating a portion of Prime membership fees to video, an exercise that's inherently subjective. (I've revised my calculation down from last month.)

→ Disney's streaming revenue grew double digits, powered by bundles to reduce churn, advertising execution, the new ESPN DTC launch, and two months of Fubo TV consolidation. (I've normalized their fiscal year to calendar; the company does not break out ESPN DTC revenue.)

Except for pure-play Netflix and Spotify, streaming is just a subset of a much larger business, contributing to Streaming Enterprise Value™.

Following Paramount's acquisition of Warner Brothers, the questions I hear most: How will they consolidate HBO and Par+ without cannibalizing revenue? How many job losses, second order effects? How does Netflix respond? Where does Peacock fit? NBCU's co-CEO said yesterday they're happy being US-only, but they do own Sky and 50% of SkyShowtime with Paramount.

David Ellison told CNBC today: “We will not sell either lot”

As Streamonomics® readers know, the competitive set keeps expanding. Eight of the top 20 most valuable companies in the world are in the attention economy: Alphabet, Amazon, Apple, Microsoft, Meta, Walmart, Samsung, Tencent all compete with streamers for consumer and/or advertiser dollars, time spent, and talent.

THE BIGGER PICTURE:

→ Streaming profits are growing, but they're only part of the picture

→ The "streaming wars are over" narrative was premature; competition is perpetual

→ For content suppliers, distributors, or investors: the key isn't who's biggest: it's understanding where your content, capabilities or assets fit in the evolving stacks

Back in December I laid out "What I'd Do in 2026". Part II is coming next week. Subscribe to Streamonomics® for free (link under my name). Owl & Co clients get it earlier, with exclusive data.

English

If you can predict how many hours of sleep I got last night, Matt will send you a free Town mug.

Matthew Belloni@MattBelloni

New pod: Did Hollywood just reach DEFCON 1? Breaking down this holy shit moment, with a special Friday appearance by @Lucas_Shaw. Listen! Watch! open.spotify.com/episode/3IQbsd…

English

If you're one of the thousands of Fox International Channels or Wondery alumni, you know what I've always believed: great companies are built by people who are smarter than you, who care, who are driven, and who are great to work with.

That belief hasn't changed. I'm building Owl & Co the same way.

I'm hiring a Principal to work directly with me, advising CEOs, leadership teams, and investors across media, tech, and the attention economy.

This isn't a generalist strategy role. We are an operator-led, specialized firm, deep in the data every day, obsessed with finding every path to grow enterprise value. Our clients often already have world-class internal strategy teams and access to some of the same data we see. They hire us because we've sat in their chair, connect time spent and economics, and we read the early signals that, when compounded, turn into real enterprise value.

The competitive landscape is changing: 8 of the top 20 most valuable companies in the world participate in the attention economy. Large enterprise leaders need to find the next S-curve, which is often in a space considered "too small to bother" (something I heard in the early days of Fox International Channels and Wondery). We have a builder-and-scaler mentality and understand the tradeoffs: budgets, culture, conflicting priorities, stakeholder perception. We won't recommend something you can't actually execute.

The right person has deep consulting roots: the kind where you learned to structure a problem before you solved it. You've spent real years inside a media or attention-economy company, not just observed it. You use AI as a daily force multiplier, not a talking point. And you're drawn to a small, high-leverage firm because you want your work to matter.

We are a demanding place to work. We'd rather run tight than hire wrong. For the right person, it's an extraordinary opportunity.

If that's you, the posting is live: link below.

buff.ly/vbp88tG

If that's someone you know, send this to them or comment "commenting for visibility." Thank you.

And if a full-time role isn't right but you'd want to advise on select engagements, we have an Advisor track too. Same link.

English

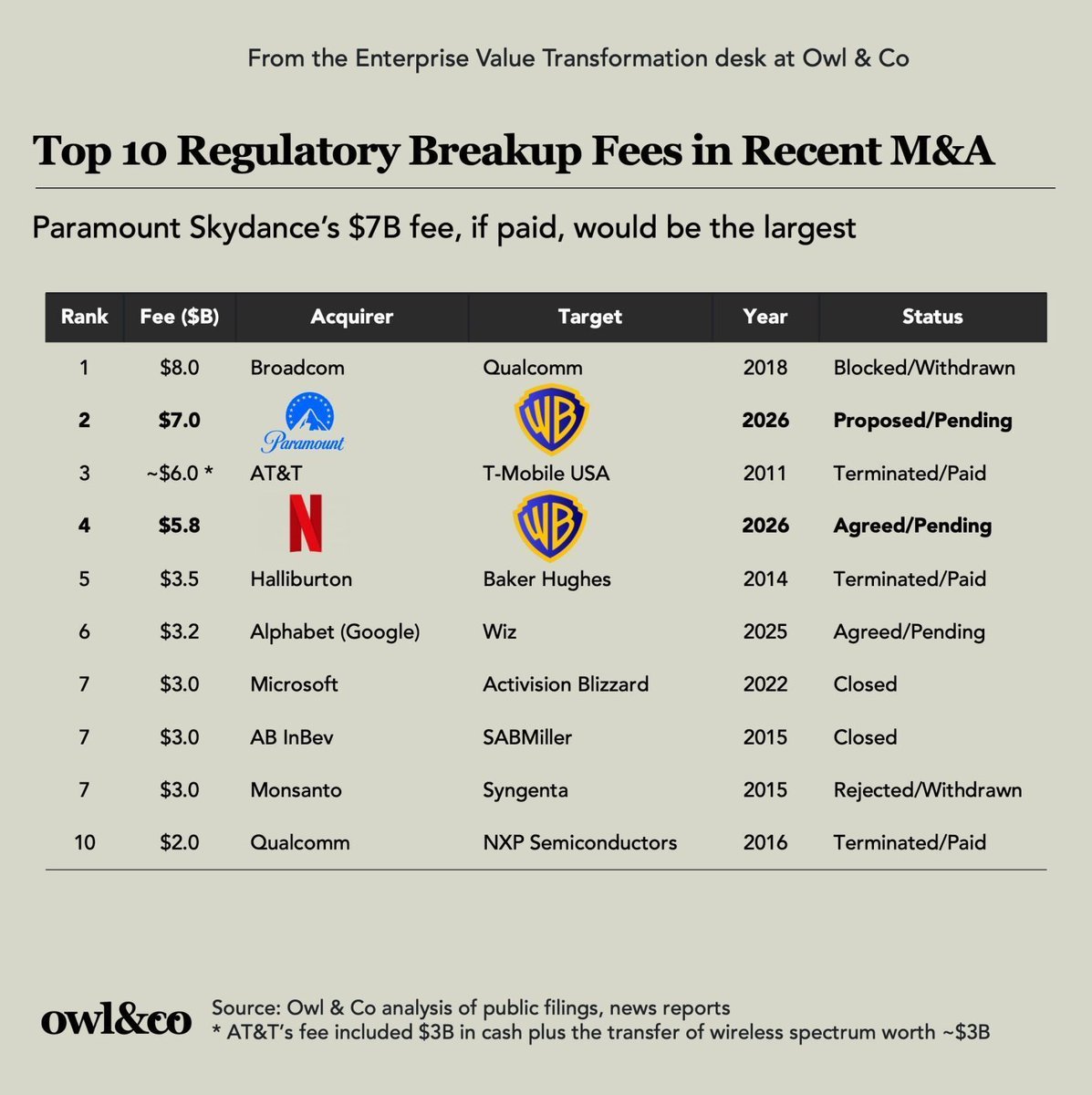

@ParamountPics @Skydance just raised its breakup fee for @wbd to $7B. If paid, it would be the largest in recent M&A history, a sign of the company's confidence in a timely closing, and a tough pill for @netflix to agree to.

The revised offer also accelerates the "ticking fee" to Q4 2026 (vs. Q1 2027 previously), adding pressure to close faster (for every quarter beyond Q4 2026, Paramount must pay an additional $0.25/share, equivalent to ~$0.65B).

But here's what most coverage misses: Netflix has two paths, not one.

Path 1: Match. WBD's Board hasn't yet said Paramount's proposal is "Superior" - they said it could reasonable expected to be. Once they formally declare it a "Company Superior Proposal," Netflix gets 4 business days to counter; the clock hasn't started yet. But in addition to increase the headline price, will they accept a $7B regulatory break fee plus an headline purchase price increasing by $0.65B every quarter starting in Q4? Netflix's current fee is $5.8B, and it has an out date of March 2027, automatically extended until June, then September'27.

Path 2: Walk away with $2.8B. Netflix's existing agreement includes a termination fee if WBD takes a superior offer, and Paramount has agreed to reimburse that fee. Ted Sarandos said as recently as this weekend that they could walk away - as readers of The War for Warners will remember, the Netflix/WBD agreement started with an ultimatum.

What happens next:

→ WBD must keep Netflix informed within 24 hours of any material developments, including draft agreements

→ Any material non-public info Paramount gets, Netflix gets at the same time

→ March 20 stockholder vote remains on the calendar; WBD can't freely postpone it

→ No recommendation change until WBD formally declares Paramount "superior" and completes the match process

→ Pre-closing covenants likely to be heavily negotiated

Paramount reports Q4 earnings at 1pm Pacific today. Listen for signals on financing confidence and integration plans.

THE BIGGER PICTURE:

→ The $7B breakup fee signals Paramount's conviction and puts Netflix in a tough spot; if paid, it would be the largest (Broadcom's $8B breakup free to Qualcomm never got paid, as the DOJ blocked the deal before there was a definitive agreement)

→ Netflix's $2.8B walk-away option is underappreciated; they may prefer cash to complexity (Last night, prediction market Kalshi had Paramount's chances of success at 64%, the highest since the process started)

I've been tracking this deal since Paramount's first approach. Full breakdown of the merger mechanics in my updated "War for Warners" article (link in comments).

English

In 1996, @HBO told the world: "It's not TV. It's HBO."

In 2025, @YouTube said: "YouTube IS TV."

Both statements were positioning genius. HBO was telling premium subscribers they were buying something above television: prestige and originality that justified a monthly fee on top of cable. YouTube was telling advertisers the opposite: that the biggest screen in the house now belonged to them.

But between those two slogans, separated by nearly thirty years, what counts as "television" has stretched further than ever. In this week's Streamonomics®, I break down three storylines that help explain why:

→ Video podcasts are becoming TV, starting with daytime (a daypart underinvested by both linear and premium streaming). @Apple just announced native video support for podcasts. Meanwhile, @netflix, @hulu, @Amazon, and @Tubi are all licensing and/or commissioning, with other streamers making offers. There's a wide range of visual aesthetics, storytelling and interviewing skills, production qualities and economics, but the bar is only going up. Video podcasts that were only available on YouTube a year ago are now sharing shelf-space with Stranger Things.

→ Vertical Video is a third audiovisual language. Not a format. A language. Film. TV. Vertical. Microdramas (which are as divisive as podcasts were before them) are just the first scripted expression; at 3% of vertical video's $100B+ market. The canvas will expand to capture every genre of television, then every subgenre.

→ AI will close the production gap, not the storytelling gap. The still ongoing "SaaSpocalypse" rattled software stocks. Then came Seedance 2.0, which rattled media stocks (as I call it, the "AI Flu") and provoked a strong counter-reaction, uniting studios and talent, and prompting Seedance to delay the availability of their API in the US. Though the direction is clear: as entrepreneurial creators and studios are able to produce more, supply will increase, so will discovery challenges.

Both HBO and YouTube are again in the news today. HBO parent WB is deciding who's going to be their next owner: Netflix or Paramount, which submitted a new bid last night. And YouTube is rumored to be the front-runner for a new package of 4 NFL games.

THE BIGGER PICTURE:

TV didn't kill Film. Vertical won't kill TV or Film. Each new audiovisual language expanded the market; each new format expanded what counts as television.

The question for leaders, talent, creators, entrepreneurs, is how to capture the gains from the next wave of expansion.

I cover this in depth tomorrow. Subscribe to Streamonomics® for free (link under my name). Owl & Co clients get it a day early, with exclusive insights.

English

Hollywood waiting for @Lucas_Shaw’s Screentime to tell us what’s going on in the War for Warners

GIF

English

New pod: The head of Netflix is making a final push to convince us buying Warner Bros is good for Hollywood. I have MANY questions. With Ted Sarandos. Listen!

open.spotify.com/episode/1Ya9W5…

English