Angehefteter Tweet

Stat Arb

14.8K posts

Stat Arb

@quant_arb

MFT & HFT | Views my own. Not financial advice.

the orderbook Beigetreten Kasım 2019

1.6K Folgt68.3K Follower

Options MFT is quite a vague idea for most people.

How do we construct portfolios?, what do alphas look like?, we surely cant be predicting each option individually can we??

In my latest article I cover this topic and how to construct alphas and portfolios for options MFT

English

When markets are volatile managing stress is crucial in order to perform optimally

Don’t be afraid to scream at your wife or kick your dog to blow off some steam and get your head back in the game

English

An alpha is the same as a feature from classical machine learning. It is some metric which captures information about what we are trying to predict.

Say we believe momentum arises on the 4 week timeframe from smooth returns. So we use Sharpe ratio of returns over the last 4 weeks (basically return penalized for volatility - ie not being smooth) and that is our feature.

This is an MFT example for futures but for options is may be something like volatility in the underlying for ATM vol parameter or aggressive trades spike as another example

English

One of the points I make in this article is about how alphas drive profitability and not models because fundamentally models behave like more of a multiplier than addition. Alphas are addition.

In the MFT case, 0*2 is still 0, and hence it only makes sense to have people who spend a huge proportion of their time of optimising the multiplier if your base number is already large (because the gains will likely be quite incremental so you need to have a very profitable base for that incremental gain to be worth enough to have that person in that role)

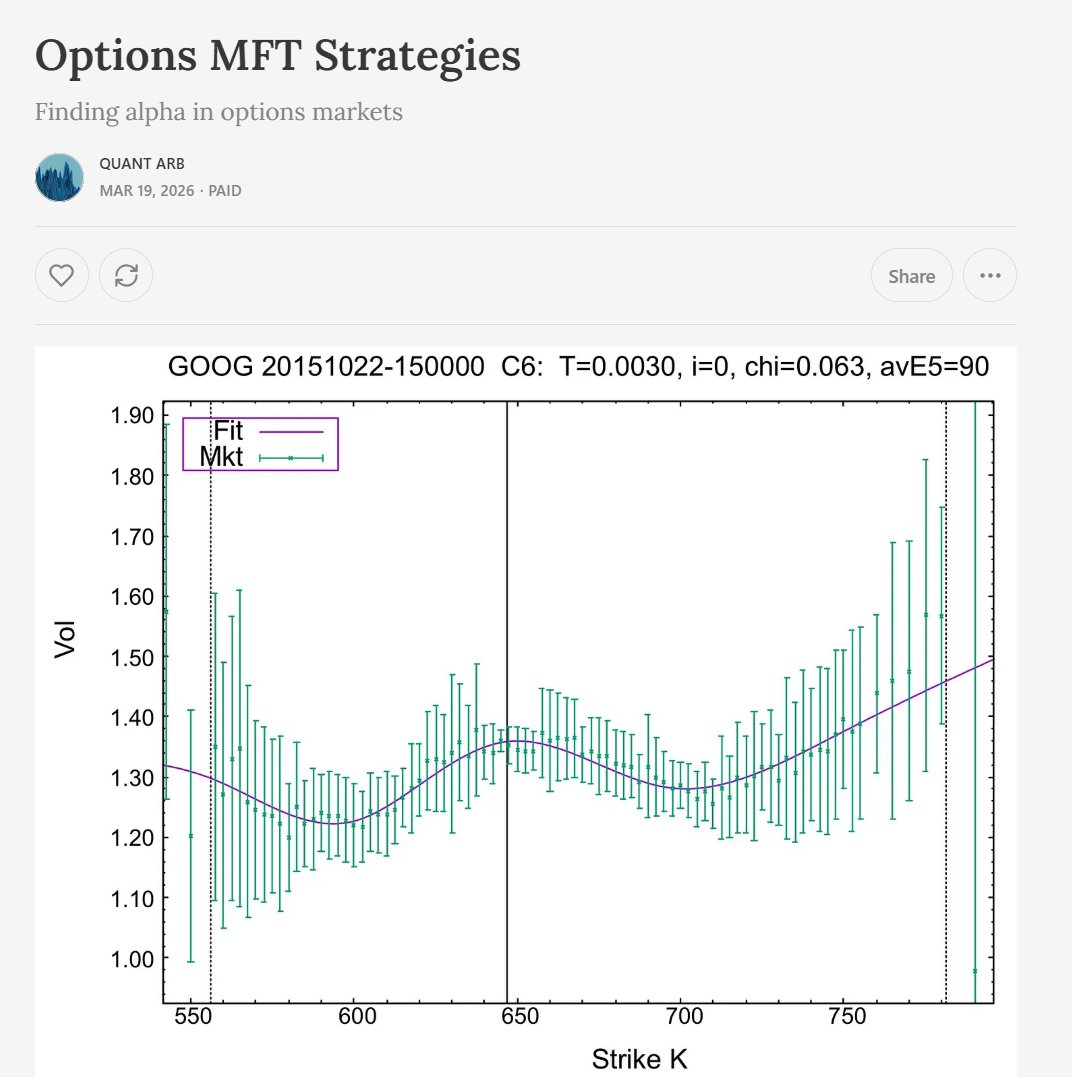

I’ve made this point a few times before - but I expand it to the world of options this time. A lot of options revolves around condensing the immense dimensionality of 1000 options prices into a limited set of metrics/parameters and to normalise them all so they are comparable.

To normalise them, the standard is black Scholes - not because it is a perfect normaliser but because it is a simple one. Basically what’s the standard deviation of a normal distribution which makes this option fairly priced.

To condense them, we use vol curves. The parameters represent some characteristic of the curve (overall vol, skew, tails) and we use it as an approximation for 1000s of prices. The edge is not in the model, but in predicting the parameters themselves. If you have a very simple model SVI and you can predict the parameters incredibly well - you’ll make a fortune, but if you have the most detailed model on the planet which fits amazingly but have no idea about the future the you probably won’t make much at all quoting around it. The alphas once again are the edge (the features which we use to predict parameters) and not the model itself!

It’s all alphas…

Stat Arb@quant_arb

Article on how to structure, trade, and monetize alphas on my blog out now :)

English

@josusanmartin Yeah on-demand seems to be about 60% of the price of opus 4.6

English

@quant_arb Codex has the best limits. I feel like it's 4-5x more than Claude Code Max.

Comparing the two $200 versions.

English

@0xHamsterdam I think so, I’d be using Claude directly through Anthropic with Claude Code so probably cheaper

English

What does good features look like?

- order flow imbalance doesn’t work (at least not raw volume without interesting transforms)

- orderbook imbalance works really well but everyone knows it!

- there’s 100s of other features you can engineer and skew into on various timeframes

Stat Arb@quant_arb

The trick is to have good mid price and blow out spread at the right times. That’s a lot of the problem. Good mid is just many good features and hence good forecasts

English

The trick is to have good mid price and blow out spread at the right times. That’s a lot of the problem. Good mid is just many good features and hence good forecasts

daqing su@DaqingSu

@quant_arb Genuine question: what theoretical framework would you start with? Stochastic optimal control problem? HJB? With RL, regime, OBI, OFI, queue dynamic?

English

English

Ever since Claude code came out there has emerged a group of people into algo trading that didn’t have the IQ previously to produce a working trading algorithm but now post as if they’re RenTech. I heard one say he “spoke to a Quantum at Jump” and saw the secret sauce

English

@QuantumHoneybee I heard it’s HMMs over at RenTech.

Hearing things 👂👆

English