Angehefteter Tweet

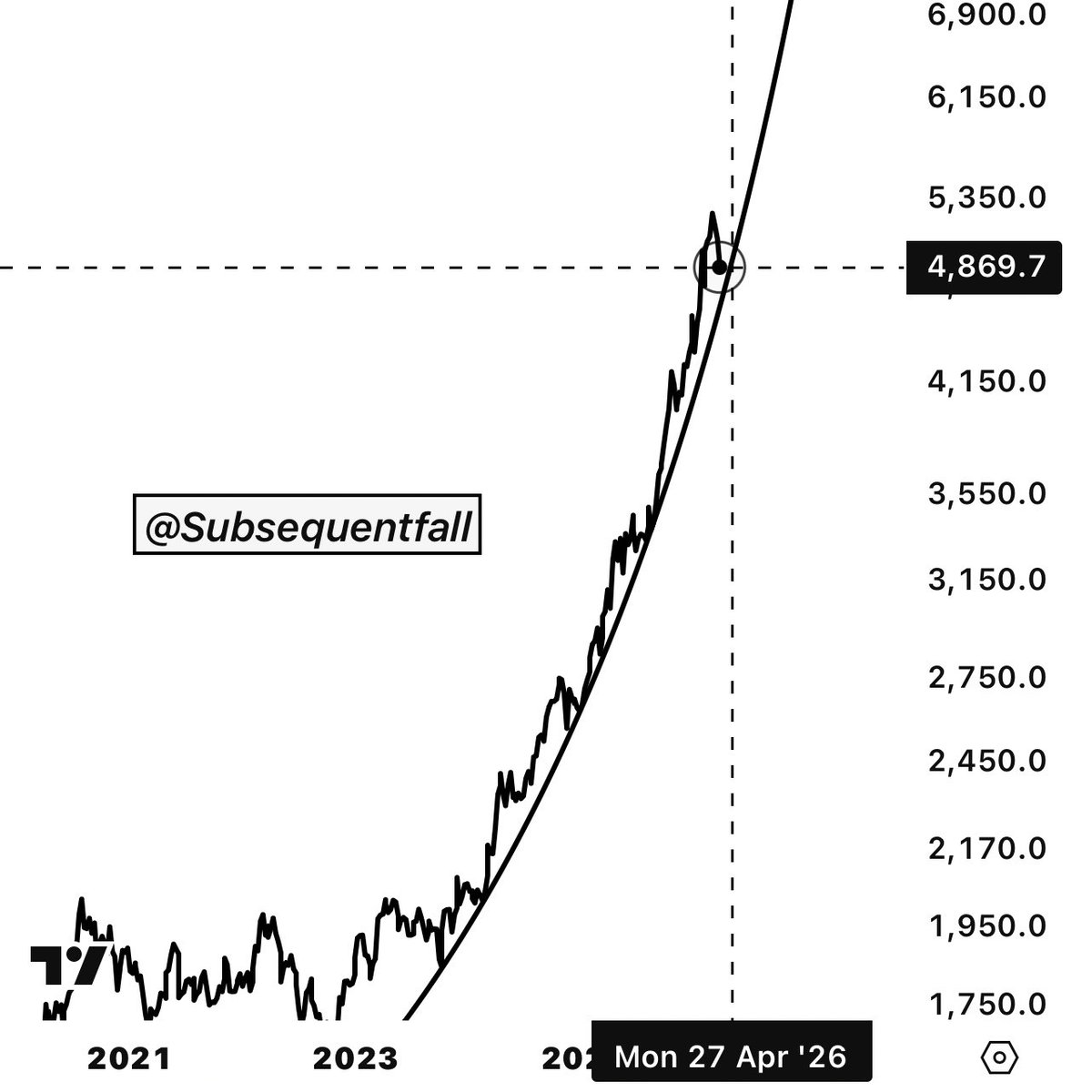

🚨GOLD UPDATE 🚨

Back to the trend line we go. Next leg up by end of April. I hope you take this time to take advantage of discounted prices before the inevitable explosion upwards.

Prepare accordingly.

English

The Subsequent Fall

2.5K posts

@subsequentfall

History tells you the story. I’ll tell you how this chapter ends.

Global airlines are cancelling flights at an unprecedented pace: Airlines have cut 2 million seats and 12,000 flights worldwide from their May schedules over the last 2 weeks, reducing the total available seats to 130 million. This comes as jet fuel costs have DOUBLED since the Iran war began, forcing carriers to cancel unprofitable routes, switch to smaller aircraft, and raise ticket prices. Turkish Airlines and Air China account for the largest seat reductions, cutting ~520,000 and ~490,000 seats, respectively. Lufthansa leads in flight cancellations, at ~4,000 flights in May alone, with the airline having removed 20,000 flights from its schedule between May and October. Meanwhile, Gulf carriers, including Emirates, Etihad, and Qatar Airways, are still operating well below pre-conflict capacity, as the closure of Gulf airports has disrupted ~33% of all European journeys to Asia. Singapore and Tokyo airports asked carriers not to add extra services to limit jet fuel use, and Vietnam introduced jet fuel rationing. The global aviation shock is spreading.

Every time oil prices surged 50% above trend, it triggered a recession. This indicator predicted 6 out of 6 recessions… a 100% success rate. We just triggered that threshold again.... But I guess this time it's different

⛽️👀 FIELD REPORT: Gas prices near you… Download the stickers, edit your local pump pics, and post it. Show us the damage 👇

California’s last major oil shipment is here. After this, we’re short about 200,000 barrels a day—and no one has explained the plan to replace it. @CAProblemSolver asked two weeks ago. Still nothing. You can’t run the fifth-largest economy on “we’ll figure it out.” latimes.com/environment/st…