Tweet fijado

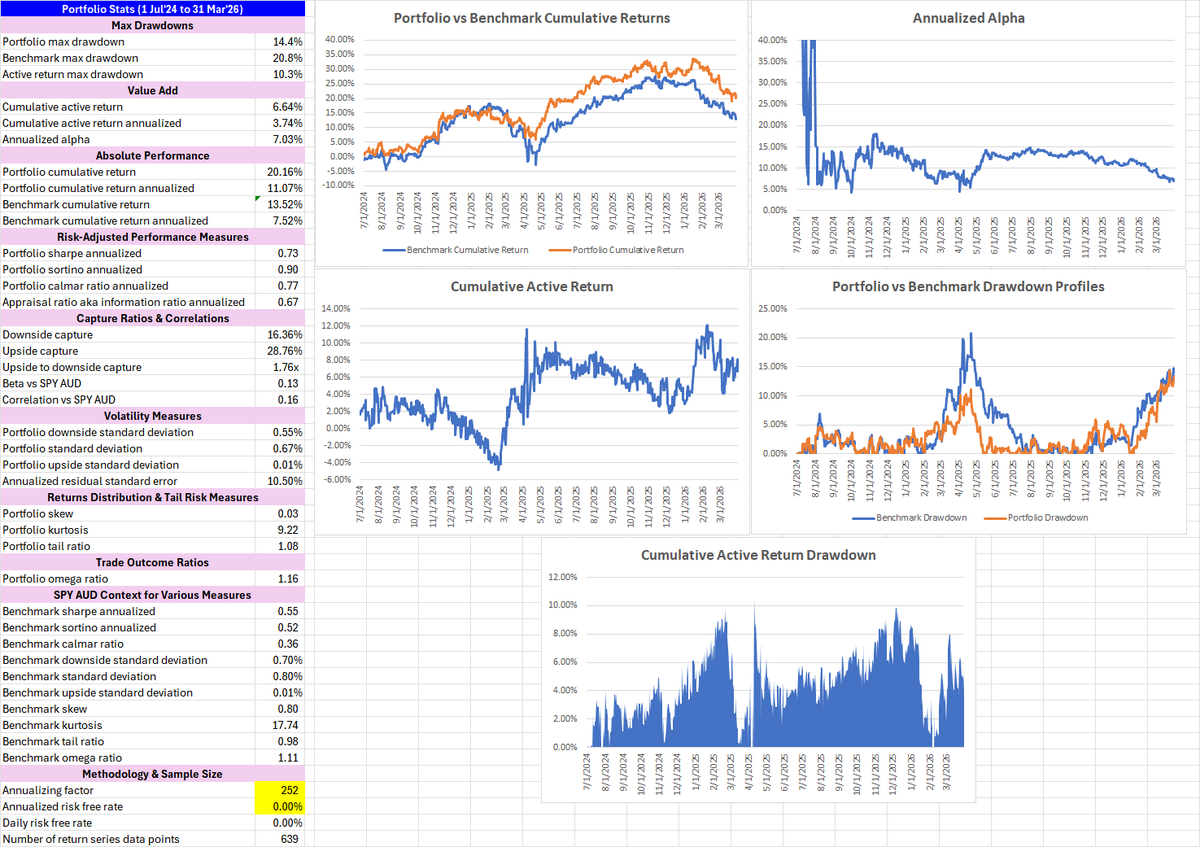

Top metrics to look at to separate skill from luck in portfolio performance

Get this template for FREE here:

huntingalphas.com/#/portal/signu…

English

Hunting Alphas | 5-Min Stock Pitches

469 posts

@HuntingAlphas

9k+ ticker universe. 5-min tactical stock pitches for serious investors & position traders. Granular portfolio analytics. Former analyst at $6Bn fund.

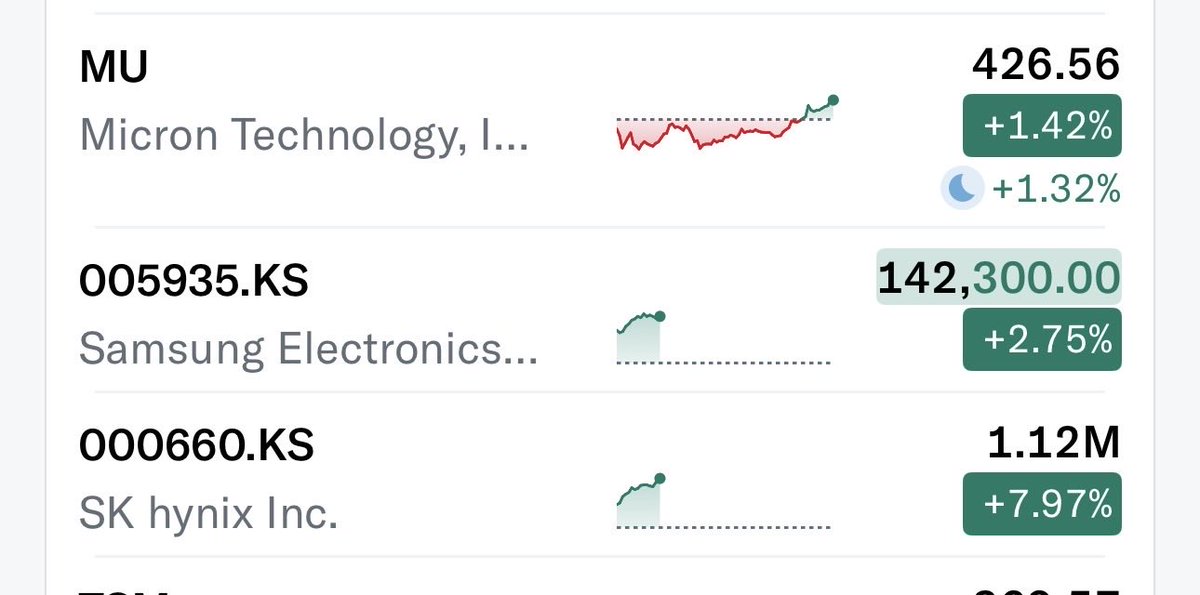

SK Hynix ATH

Look at the underlined parts It adds credence to the view that: 1. The ceasefire between US and Iran is still intact 2. The 2 nations' representativeness are in better talking terms 3. Although there is no lasting peace deal yet, it is still net progress toward de-escalation compared to the start of last week

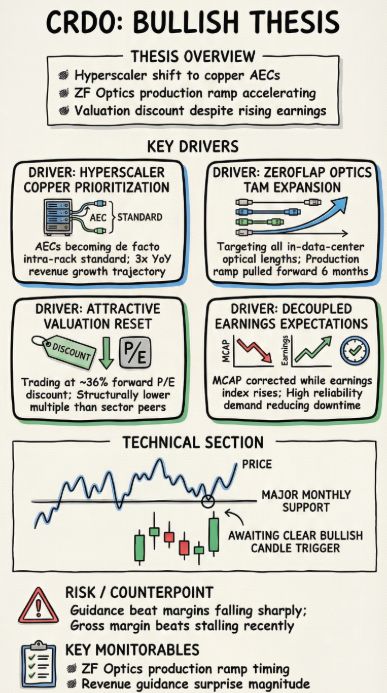

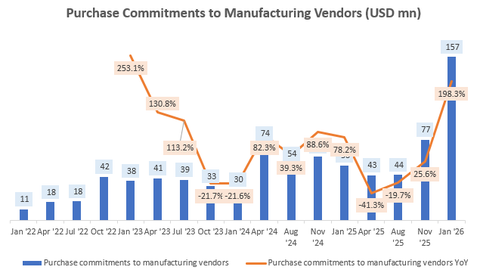

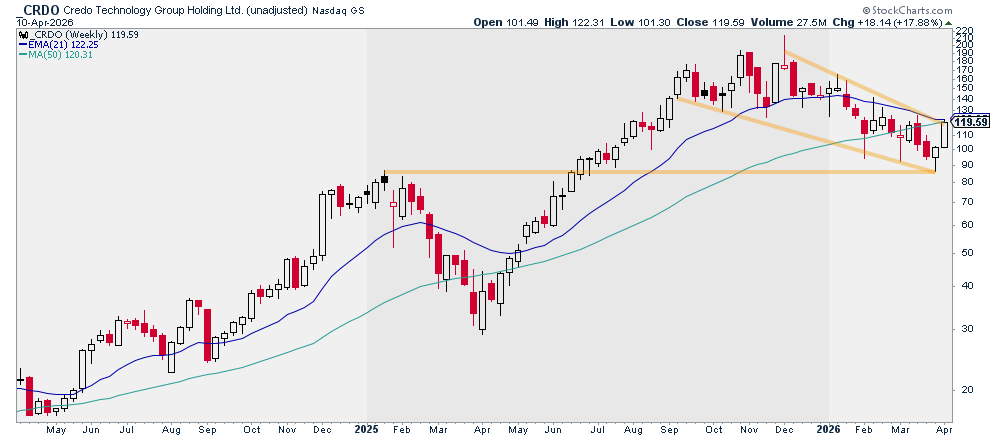

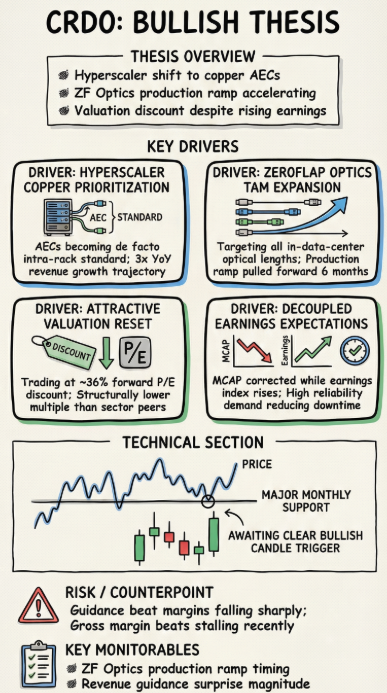

I'm bullish on Credo $CRDO: 1. Hyperscalers are prioritizing copper connections in compute infrastructure 2. Credo is making rapid progress to launch into a new product category 3. Lower beats on guidance may limit upside 4. Rising earnings expectations and a lower valuation multiple are very attractive 5. Wait for the buyers to kick in at support Get my model for $CRDO from my website (link in bio)

I'm very bullish on Taiwan. Following on from my Browave thesis: > @FT report that "the US tech industry will remain critically dependent on Taiwan for the immediate future." > " $AAPL, $NVDA, $AMD, $QCOM and $AVGO have no viable alternative manufacturer of advanced chips at the scale they need." Taiwan's GDP growth will be crazy high for the next ~5 years given the AI supercycle and near monopolies e.g. mass production of 2nm from $TSM. Also CoWoS - where $NVDA Blackwell & Rubin and $GOOGL TPUs require this specific packaging to function. Taiwan has raised CoWoS capacity targets for 2026–2027 to meet "urgent orders" from $GOOGL and $NVDA. No other country has the scaled infrastructure to perform CoWoS. Also, geopolotics aren't really a concern to me: There's huge global reliance on Taiwan's technology. All major powers (including China) benefit more from Taiwan’s continued operation than its destruction.