Jaden

249 posts

Jaden

@MiamiAnalyst1

Kiwi Market Analyst now based in Chile | Uranium bull since COVID | Breaking down U stocks, commodity news & market moves.

Miami Se unió Haziran 2024

152 Siguiendo62 Seguidores

#SPUT @Sprott #Uranium Trust $U.U $U.UN #nuclear #GreenEnergy

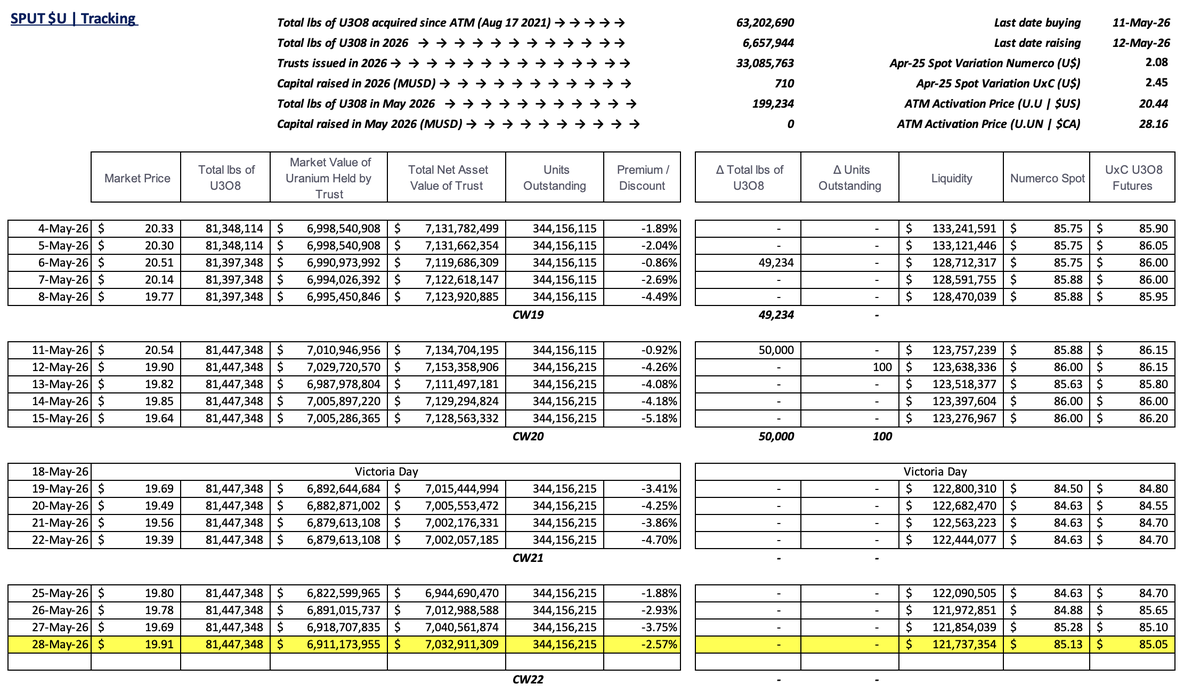

-2.57% discount to NAV

No pounds purchased

No trusts issued = no $ raised

$121.7m in cash!

English

@chrisluxonmp @Keir_Starmer You gonna send over sheep to help win the war or what. Better nz stay out of that stuff

English

Spoke with UK Prime Minister @Keir_Starmer over the phone last night.

We discussed the situation in the Middle East. With high fuel prices causing pain in Kiwis’ back pockets, we agreed on the importance of diplomacy to reopen the Strait of Hormuz and get shipping flowing freely again.

Both the United Kingdom and New Zealand are steadfast in our support for Ukraine, so it was good to compare notes on how to maintain the pressure on Russia.

The United Kingdom is an important partner to New Zealand: we’re doing a lot together to advance our prosperity and build global security.

English

Where is the best place for a long weekend holiday in New Zealand?

English

Jaden retuiteado

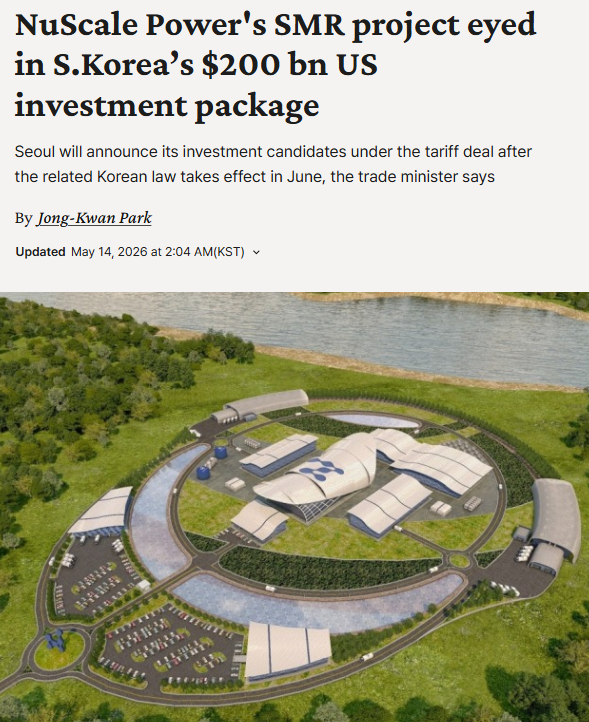

Many have been writing NuScale off for dead. Perhaps tales of its death have been exagerrated. Korea is considering invensting in NuScale, as part of the $200 billion US investment package that they agreed to in tariff negotiations with Trump. Article link in reply.

English

Jaden retuiteado

🇬🇧 A few years ago, “a new era of British nuclear energy generation” was not the kind of phrase you’d hear from the British throne.

👑 King Charles III, yesterday:

“My Ministers will also take forward recommendations of the Nuclear Regulatory Review and encourage a new era of British nuclear energy generation”

English

Imagine if someone told you this morning that #uranium equities will close green 🟢 today after spending part of the morning deep in the red.

🤔

English

Jaden retuiteado

US To Develop Small Modular Nuclear Reactors For Commercial Shipping zerohedge.com/energy/us-deve…

English

Jaden retuiteado

Breaking! Uranium Squeeze! Cameco $CCJ just confirmed FLOODING in Northern Saskatchewan caused the COLLAPSE of the Smoothstone River Bridge, the PRIMARY supply route to McArthur River / Key Lake. THis is the 2nd largest Uranium producer.

This is one of the MOST important uranium mining complexes on Earth. $LEU $UEC $UUUU $SMR $OKLO

Cameco stated

• Key Lake production activities TEMPORARILY HALTED

• McArthur River activity REDUCED

• Timeline for resumption UNKNOWN

• 2026 production outlook now at RISK

People STILL do not understand how tiny and fragile the uranium market is.

This is EXACTLY what happened during the last uranium supercycle.

Back in 2004 the Cigar Lake uranium mine FLOODED in Saskatchewan during an already tight uranium market.

Cigar Lake was supposed to become one of the world’s largest uranium mines.

Instead flooding delayed production for YEARS.

Supply vanished.

Utilities panicked.

Uranium then exploded from roughly $20/lb to $138/lb.

Now history is starting to rhyme again

And this time demand is EVEN STRONGER because

• AI power demand is exploding

• Nuclear restarts are accelerating

• Utilities remain undercovered

• Western nations need domestic fuel security

McArthur River is the world’s largest high-grade uranium mine.

Key Lake is one of the world’s largest uranium mills.

Now logistics are breaking down.

Commodity squeezes happen when:

Tiny markets + supply shocks + rising demand collide.

English

Jaden retuiteado

ARGENTINA LITHIUM ENERGY

$LIT.V

Update:

With 99.5% pure lithium carbonate approaching $28,000 USD, I think it's worth putting into context what this means for Argentina Lithium Energy's Rincon West project.

$LIT.V's operating leverage, or sensitivity to lithium price increases, is very high.

The first phase, projected with Lanshen, anticipates a production of 5,000 tons per year (later increasing to 15,000 tons per year).

If we estimate a direct cost of $5,000 per ton and a revenue of $28,000, the operating margin would now be $23,000 per ton.

$23,000 * $5,000 = $115,000,000 annually in the initial phase.

With Lanshen's integration into the capital structure, which prevents $LIT.V from having to assume a high capital expenditure to reach production, its stake in Rincon West would ultimately be 50%, as stipulated in the agreement.

50% of $115 million = $57.5 million annual operating margin in the first phase.

Argentina Lithium's market capitalization is $12.4 million.

These figures are starting to get absolutely insane.

(This is not a purchase recommendation. There are undisclosed risks.)

Paulofutre@Milinkoeterno

ARGENTINA LITHIUM $LIT.V (13,4 M $ market cap) Following the agreement with Lanshen announced this week, the path to production and free cash flow (FCF) generation appears clear. The management led by Niko Cacos seems excellent to me. He has successfully brought both the lithium buyers and producers into the company's shareholding structure. I'm referring to Stellantis and Lanshen, respectively. We may still have some minor dilutions. Further exploration is needed to increase resources and to convert inferred tonnage to measured/indicated tonnage. Junior companies aiming to produce lithium face the significant hurdle of the necessary capex to achieve production. It's unthinkable that a company with a market cap of between 10 M and $20 million can reach the production phase only with dilutions. Therefore, the presence of strategic partners is absolutely essential, and Niko Cacos and the management team at Argentina Lithium Energy have demonstrated absolute professionalism in this regard. The market capitalization is currently $13.4 million USD. The fully diluted market cap is higher, but almost all warrants have exercise prices 50% higher than the current share price (0.105 CAD). It's also worth noting that the last recent capital increase was carried out at a price of 0.12 CAD (14% higher than the current price). What is the economic impact of the agreement with Lanshen? The company’s Framework Agreement with Lanshen envisions facility producing 5,000 tonnes per year (tpa) of battery-grade lithium carbonate. The cost of the modular installation will be covered by Lanshen. The agreement values the cost at approximately $95 million USD and will be borne by Lanshen in exchange for 30% of the shares of the company subsidiary of Argentina Lithium that currently owns the Rincon West project. It's important to note that the agreement covers the first phase of production. This is, in my opinion, the most important. Once Rincon West begins production, the free cash flow (FCF) generated will be able to finance the remaining phases, reaching 15,000-20,000 tons annually, without further dilution or changes to the shareholding structure. At current market prices, the financial outlook is as follows: • Gross Annual Revenue: Approximately $117.5M – $126.5M USD (based on ~$23.5k–$25.3k per tonne). • Operating Margin: With DLE (Direct Lithium Extraction) operating costs (OPEX) estimated between $5,000 and $6,000 USD/t, the potential profit margin sits at roughly $18,000+ USD per tonne. The annual operating margin in the first phase would amount to 90 million USD. (18.000*5.000 = 90.000.000 usd) • Strategic Advantage: Having Stellantis (Peugeot, Jeep, Fiat) as a 19.9% shareholder ensures a "built-in" customer, . The Product: Battery-Grade vs. Concentrate It is important to clarify that LIT.V is not producing a low-value concentrate. • The Output: They are targeting 99.5% purity Li_{2}CO_{3}. • The Technology: Lanshen's DLE process allows the company to bypass the 18-month evaporation pond cycle, converting brine directly into a high-value chemical solid on-site. Conclusions: -The agreement accelerates the process to the first phase of production up to the generation of FCF. The FCF generated in the first phase will finance the capex needed to bring production up to the 15,000-20,000 tons per year that they have once mentioned as a reasonable target for the project. -I consider it an absolute success for management to have secured partnerships with the lithium buyer (Stellantis) and the producer (Lanshen) for Argentina Lithium Energy $LIT.V in the project (19,1% Stellantis , 30% Lanshen) The path to production seems clear and management has proven to know how to do it. In my opinion, a market cap of $13.4 M USD does not reflect the progress of Argentina Lithium Energy on its Rincon West project. (This is not a buy recommendation. There are unmentioned risks. Conduct your own analysis and make your own decisions)

English

Jaden retuiteado

Uranium and nuclear energy is now a national security issue.

Small Modular & Micro Reactors

$XE X-energy

$GEV GE Vernova

$OKLO Oklo

$SMR NuScale

$NNE NANO Nuclear

$RYCEF Rolls-Royce

$BWXT BWX Technologies

Uranium Enrichers

$LEU Centrus Energy

$ASPI ASP Isotopes

Nuclear Fuel Technology

$LTBR Lightbridge

$XE X-energy

Uranium Producers

$CCJ Cameco

$UEC Uranium Energy

$BHP BHP Group

$URG Ur-Energy

$EU enCore Energy

Developers

$UUUU Energy Fuels

$NXE NextGen Energy

$DNN Denison Mines

$ISOU Iso Energy

Services and Equipment

$CW Curtiss-Wright

$MIR Mirion Technologies

$FLR Fluor

$BEPC Brookfield Renewables

$GEV GE Vernova

$BWXT BWX Technologies

Power Producers

$CEG Constellation Energy

$VST Vistra

$TLN Talen Energy

$PEG Public Service Enterprise Group

Uranium+Nuclear ETFs

$NLR VanEck Uranium+Nuclear ETF

$URA Global X Uranium ETF

$URNM Sprott Uranium Miners ETF

$NUKZ Nuclear Renaissance/ETF

English

Jaden retuiteado

Jaden retuiteado

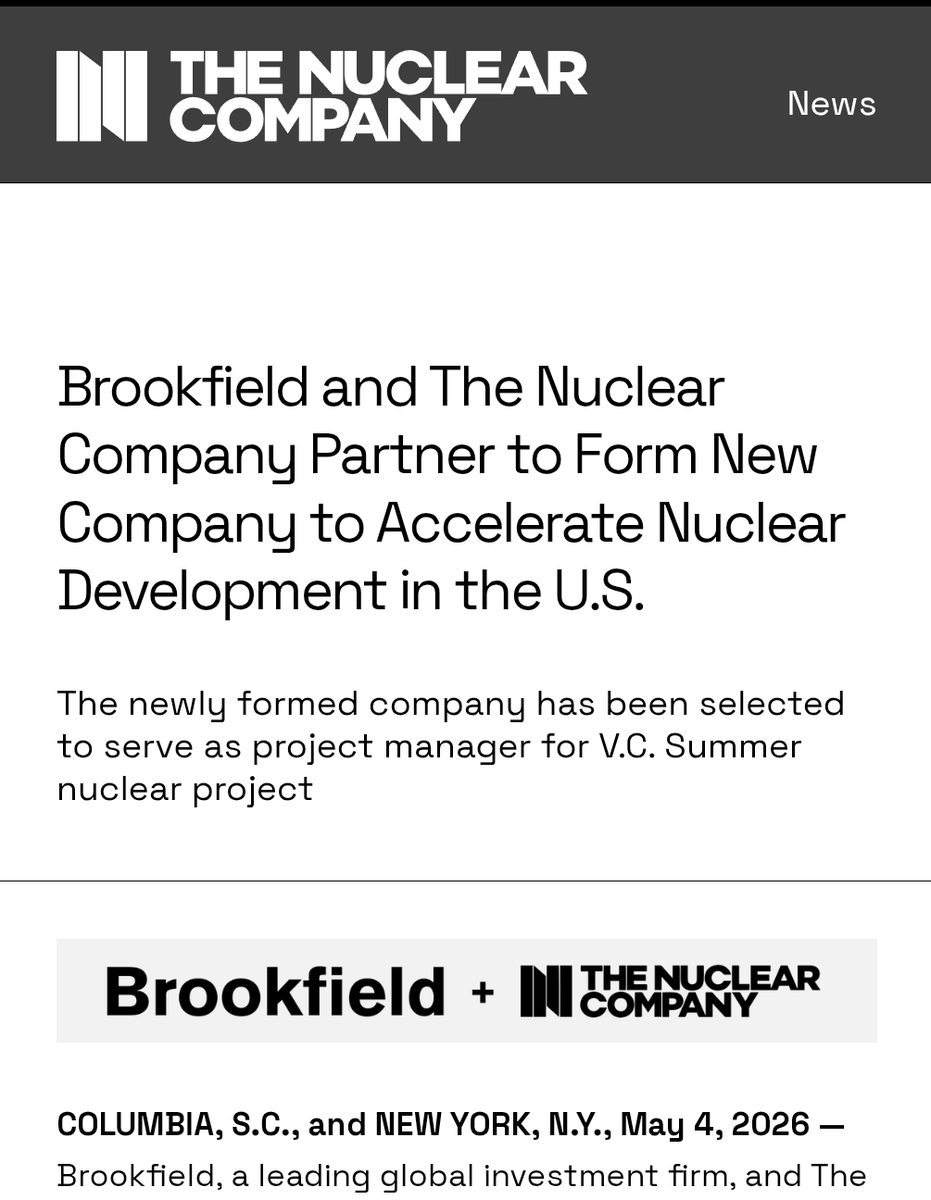

Breaking: Brookfield and The Nuclear Company teaming up to deliver GW-scale nuclear

Proud to announcing a joint venture between The Nuclear Company and Brookfield to deliver Westinghouse reactors, including to manage the completion of AP1000s in South Carolina.

From the day I discovered nuclear energy my goal has been to build as much of it as possible for the world. Today, with my team at @thenuclearco, we're taking a huge step towards that. It's been an honor to work as Chief of Staff for proven builder-CEO @JonathanWebbKY alongside our legendary Chief Nuclear Officer @TheNuclearJoe as we build the team and technology that can finally fix the nuclear plant deployment problem in the West.

I've been an advocate for nuclear energy long enough to see the revolution in public appreciation for this wondrous technology, but just being popular isn't enough. We have to be able to build on-time, on-budget, with proven designs that are repeated over and over with an experienced and disciplined project management team using the best emerging tech.

That is precisely what we're doing at The Nuclear Company. I'll be sharing more going forward as we deliver on the awesome potential unlocked by today's announcement.

English

Jaden retuiteado

China is developing a 10 MW micro-reactor that can be mounted on a truck and shipped to places that need power (remote areas, data centers, etc..). China continues to lead in the nuclear sphere. Article link in reply.

English

Jaden retuiteado

Another article by Ted Nordhaus that expresses my views more eloquently than I can. (Saves me the trouble.) A must read. If you're short on time, read the introduction section at least. Article link in reply.

English

@Wildnfree1984 Now they open the indian market up to ship our dairy products there. Ridiculous

English

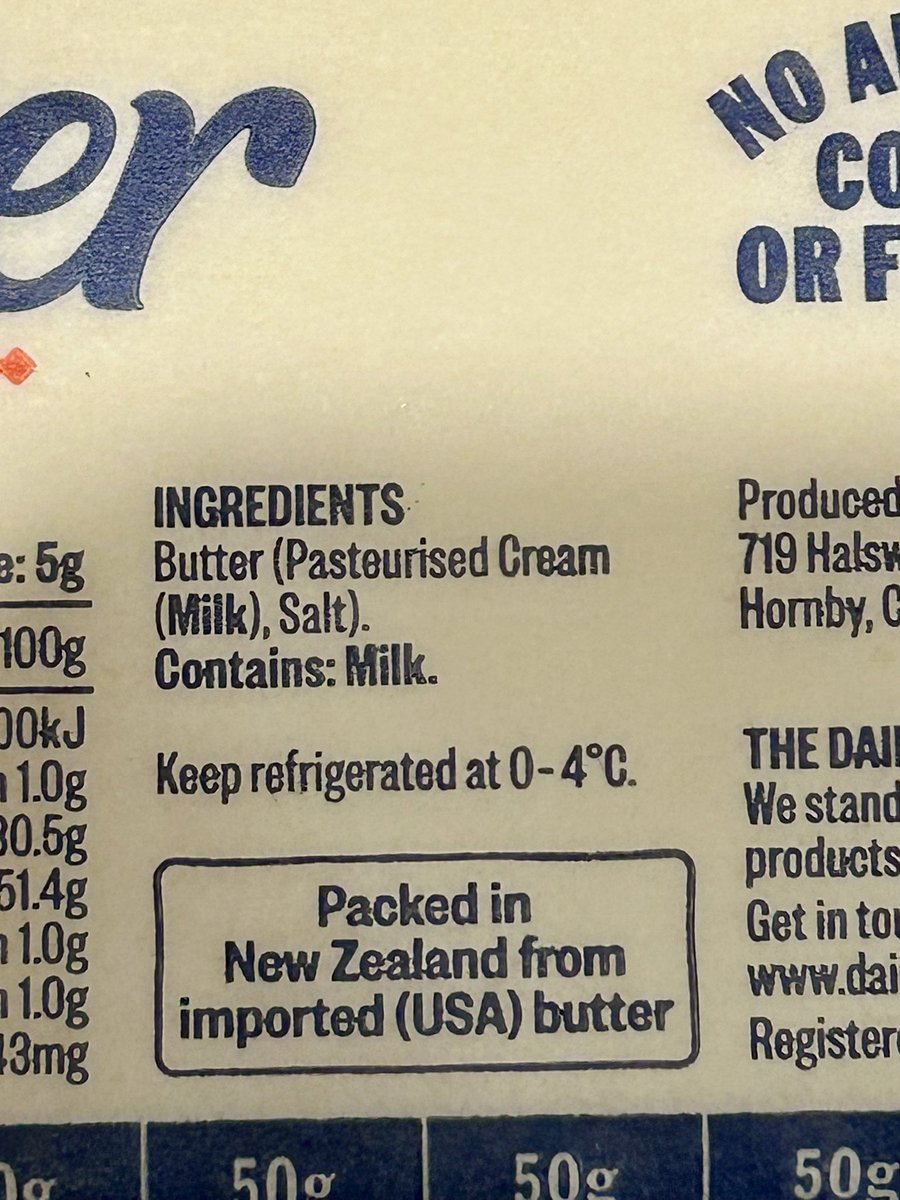

Everything that is wrong with New Zealand 🇳🇿 in 1 product 🥴

Pam’s New Zealand butter

$7.19

Burtfields’s USA imported Butter

$5.99

How the hell can it be cheaper to ship butter all the way from

USA pack it & sell it $1.20 cheaper than our own home grown product?

#nzpol

English

Jaden retuiteado

Jaden retuiteado

Not broken. Just breaking records for clean energy. 😎

English

Jaden retuiteado

I was chatting with Grok about investments and asked this question...

Appin, New South Wales 🇦🇺 English