Dean N Onyambu@InfinitelyDean

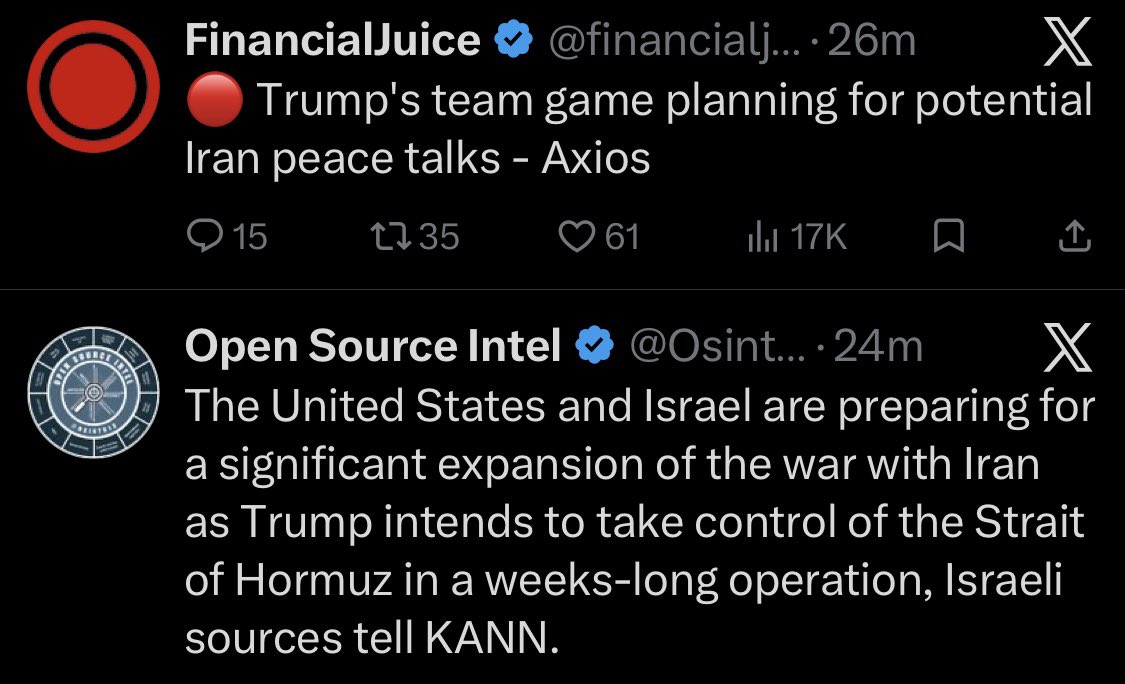

The Trump Administration has begun initial discussions on what a potential peace deal with Iran might look like, per Axios. The Kobeissi Letter summarised six reported terms. These are not the full proposal. The actual text has not been published.

The six terms: no missile programme for five years, zero uranium enrichment, decommissioning of Natanz, Isfahan and Fordow, strict observation protocols on centrifuges, regional arms control treaties with a 1,000 missile cap, and an end to proxy financing.

Four questions structure how nuclear agreements should be assessed, each requiring separate evidence: enrichment, weaponisation, delivery, intent.

The 2015 JCPOA scored roughly two out of four. It capped enrichment at 3.67 per cent and monitored weaponisation through the most comprehensive IAEA inspection regime ever applied to a non-nuclear-weapon state. Those were real achievements. But it left the missile programme completely untouched. Resolution 2231 downgraded binding prohibitions on Iranian missile activity from "shall not" to "called upon." It managed intent through incentive structure rather than verification. It contained sunset clauses, with enrichment caps expiring in 2030, centrifuge restrictions between 2023 and 2025, and missile restrictions in 2023. The arms embargo expired in 2020. Iran formally terminated the agreement in October 2025. And the deal did nothing about proxy financing. A deal that constrained one dimension of threat while resourcing another through sanctions relief was a structural flaw.

The proposed terms attempt all four dimensions. Enrichment eliminated, not capped. Facilities decommissioned, not constrained. Missiles halted and regionally capped. Proxy financing prohibited. On paper, it addresses every structural criticism levelled at the JCPOA.

The question is whether these terms are designed to be accepted, rejected, or negotiated down.

Iran rejected zero enrichment in Geneva. It rejected facility decommissioning. It offered instead to reduce enrichment to low levels under IAEA supervision, a position that mediators described as going beyond the 2015 deal. The Omani foreign minister assessed substantial progress and flew to Washington to convey this to the White House. The US negotiating team assessed otherwise. Neither assessment should be accepted uncritically.

There is a third reading. This administration has a documented pattern of opening at extreme positions and settling lower. If that applies here, the question shifts from "will Iran accept" to "what does the settlement look like." Zero enrichment negotiated to capped low-level enrichment under IAEA supervision is a tighter JCPOA. Decommissioning negotiated to mothballing with permanent inspectors strengthens access beyond 2015 levels. A binding missile restriction replacing Resolution 2231's "called upon" language addresses the delivery gap for the first time. A negotiated-down version could be stronger than the JCPOA on all four dimensions while remaining achievable.

Two concerns with the terms as summarised.

First, the five-year missile restriction creates the same sunset problem the JCPOA was criticised for, on a shorter timeline. The JCPOA's missile restrictions ran eight years. This one runs five.

Second, the monitoring language is vague. The JCPOA's verification regime was its strongest dimension: IAEA, Additional Protocol, continuous surveillance. "Strict outside observation protocols" does not specify the IAEA, does not reference the Additional Protocol, and does not address undeclared sites. If the full proposal contains stronger provisions, this concern falls away. If not, the proposed framework may be weaker on the one dimension the JCPOA got right. This caveat applies throughout: we are assessing a summary, not the document.

The terms are more ambitious than the JCPOA. Whether they are more achievable depends on whether they are a final position or an opening one.

#StructureBeforeSentiment