Dean N Onyambu@InfinitelyDean

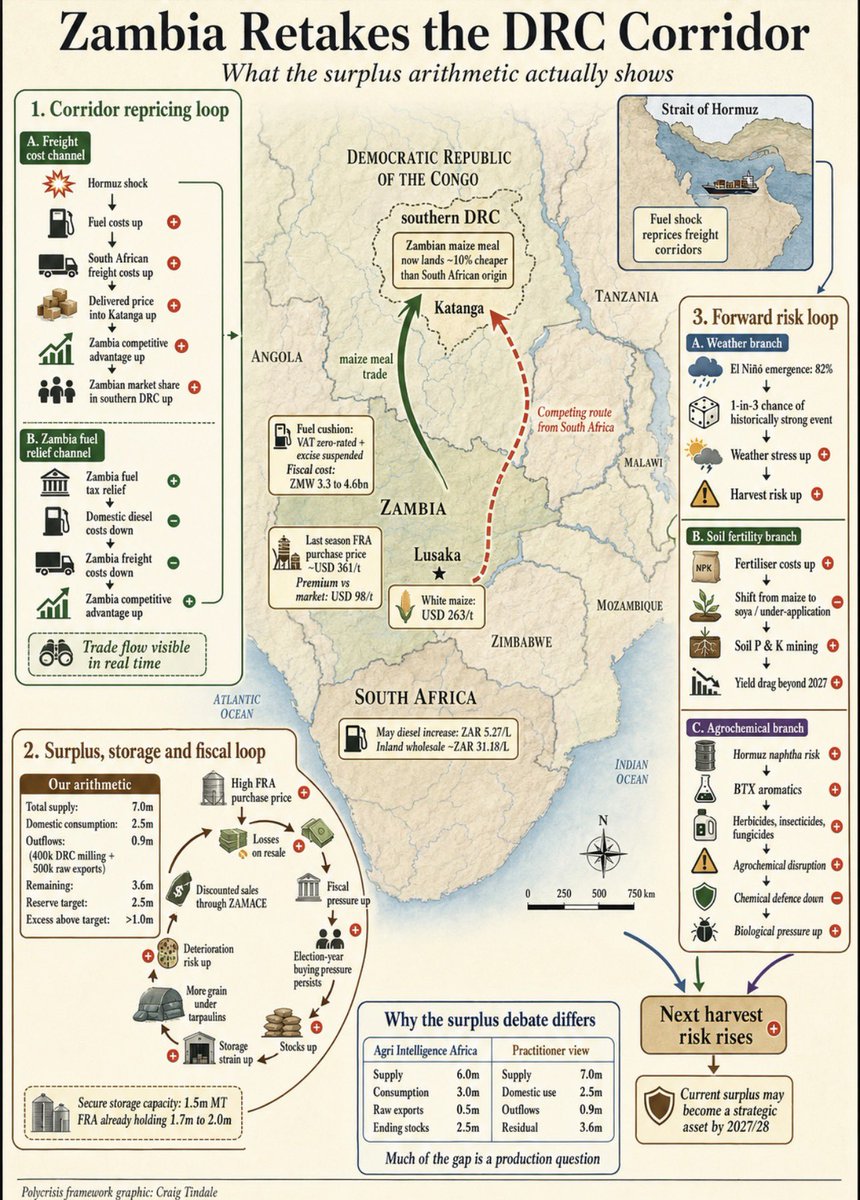

Zambia Retakes the DRC Corridor. What the Surplus Arithmetic Actually Shows.

Agri Intelligence Africa reports Zambian maize meal now landing into southern DRC at roughly a 10 per cent discount to South African origin, with Zambia regaining market share lost in 2024.

Two fuel policy responses explain the shift. South Africa's May diesel increase was ZAR5.27/litre after DMPR's correction, taking inland wholesale to approximately ZAR31.18. Zambia cushioned: VAT zero-rated, excise suspended at a three-month fiscal cost of ZMW3.3 to 4.6 billion. The differential repriced the freight corridor to Katanga in Zambia's favour. The Acid Test on Canary Compass traced this transmission in April: Hormuz reprices fuel, fuel reprices freight, freight shifts competitive advantage. It is now visible in a live trade flow.

Lusaka white maize at USD263/t. FRA's last season gazetted purchase price converts to approximately USD361/t at the ZMW18.86 rate used in our May macro note. The 2026/27 price has not been gazetted. That is a USD98/t purchase price premium against current market, up from USD81 two weeks ago. The loss crystallises when FRA sells into next season below purchase price, as it is already doing with old stock through ZAMACE. In an election year, the pressure to buy more is unchanged.

Agri Intelligence Africa and our supply chain estimates diverge on the exportable surplus, but the consumption gap is smaller than it appears. Their 3.0m consumption figure includes approximately 400,000 tonnes of maize milled in Zambia for the southern DRC meal trade. Strip that out and domestic consumption sits at roughly 2.6m, close to our 2.5m practitioner estimate. The divergence is overwhelmingly a production question: their 4.3m (which they note is conservative) against our supply chain projection of approximately 5.0m from practitioners with direct ground-level visibility. Our beginning stocks estimate was approximately 2.0m against their 1.7m.

In their model, the balance sheet resolves: 6.0m total supply, 3.0m consumption, 500k raw exports, 2.5m ending stocks matching the strategic reserve target. In ours, it does not. Total supply at 7.0m, domestic consumption at 2.5m, even with 900k in outflows (400k DRC milling plus 500k raw exports), leaves 3.6m remaining. The 2.5m strategic reserve still leaves over a million tonnes above target with limited absorption channels. That excess compounds the storage and fiscal pressure.

Secure national storage capacity is 1.5m MT. FRA is already holding 1.7m to 2.0m, with hundreds of thousands of tonnes under tarpaulins. Reaching the 2.5m strategic reserve target itself means holding 1.0m above secure capacity. Building and leasing additional storage from the private sector carries cost. Stock under tarpaulins carries risk of deterioration, particularly with NOAA now placing El Nino emergence at 82 per cent and CNN reporting a one-in-three chance of a historically strong event. FRA is already selling old stock through ZAMACE below purchase price, crystallising losses. In an election year, the pressure to buy into a system already beyond capacity compounds the fiscal drag on the primary balance we documented in Seven Stars.

Three forward risks underneath the surplus. First, those carryout stocks may prove strategic by 2027/28 if El Nino materialises at the upper end. The conditional escape we identified in Seven Stars still holds: if climate and fertiliser shocks hit the 2026/27 planting season, FRA's stock shifts from liability to strategic asset.

Second, the fertiliser-to-planting transmission is already live. The Acid Test documented Zambian farmers weighing a shift from maize to soya because soya's fertiliser requirement is a fraction of maize. As Craig Tindale (@ctindale) has mapped, when farmers under-apply fertiliser due to cost, crops mine residual phosphorus and potassium from the soil. That may buffer yields near term but risks depleting the soil bank, with potential yield drag extending beyond 2027 even if input prices normalise.

Third, the dimension almost nobody in Africa is discussing. Hormuz carries 1.2m bpd of naphtha, the feedstock for the BTX aromatics from which herbicides, insecticides, and fungicides are synthesised. If that agrochemical supply chain is disrupted, crops face the risk of losing chemical defence at exactly the moment El Nino amplifies biological pressure. A surplus today does not fully protect the next harvest if fertiliser, agrochemical, and weather risks converge.

Agri Intelligence Africa link and Craig Tindale (@ctindale) sources will be available in the comments.

Polycrisis framework graphic: Craig Tindale.