Tweet épinglé

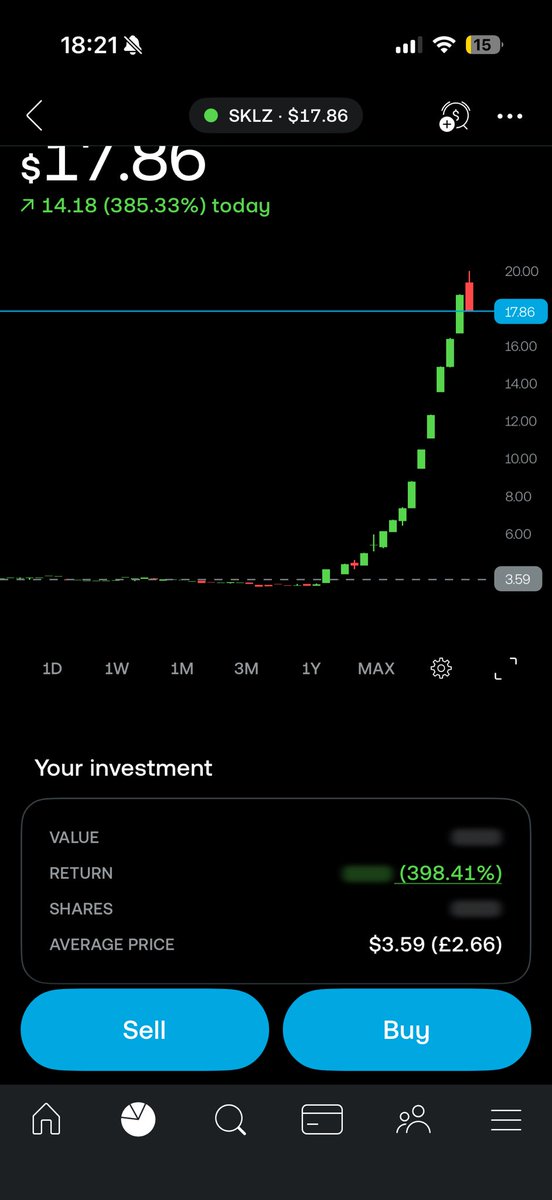

$SKLZ easiest money of my life, got pinged on discord and slapped the ask, 300% gains in just over an hour. swinging it all straight back into $IREN, Owe it all to @JonkooTrades and his discord server

English

ROY

38 posts

@ROYROYltd3

UK swing trader Currently 60% IREN in swing and 80% long term Not Financial Advice $IREN

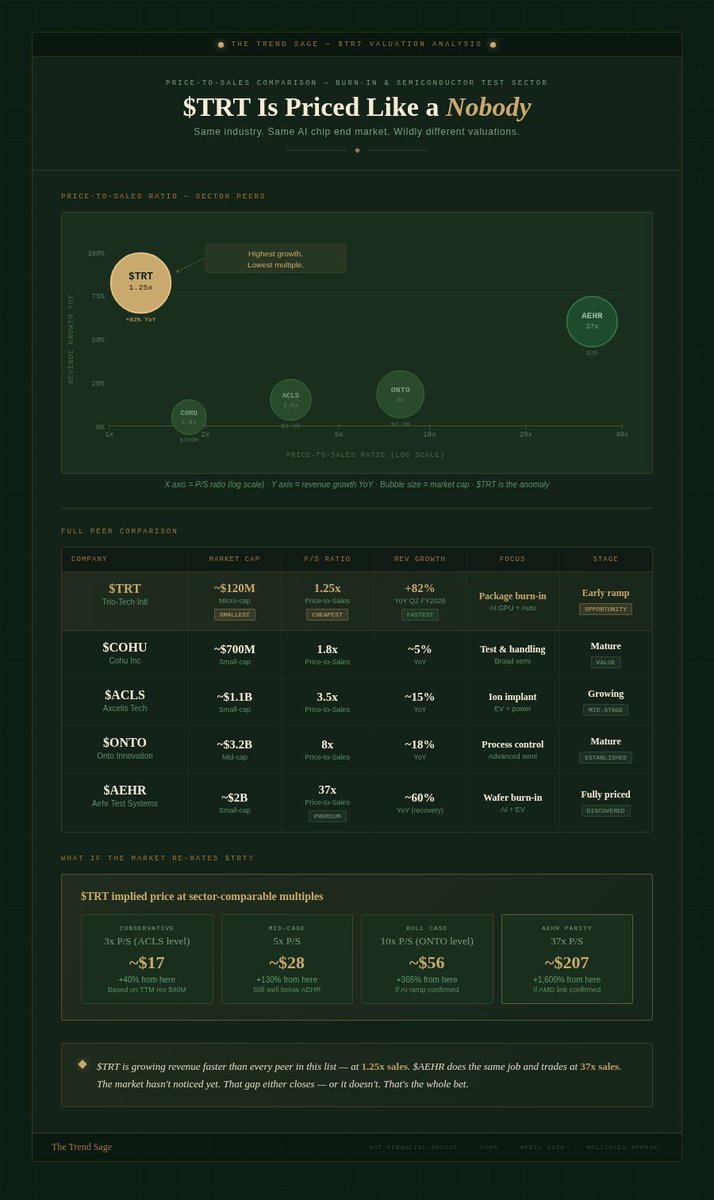

$TRT - Trio-Tech Reports 124% Q3 Revenue Growth, Driven by Strong Semiconductor Reliability Testing Demand Supporting AI and Automotive Applications

$NXT, $CSIQ I believe energy will be the next bottleneck I can't see a world where solar is not a big big winner in that, with these two stocks you have one ready to breakout and one already flying, both with earnings next week could be explosive in either direction.will BUY both

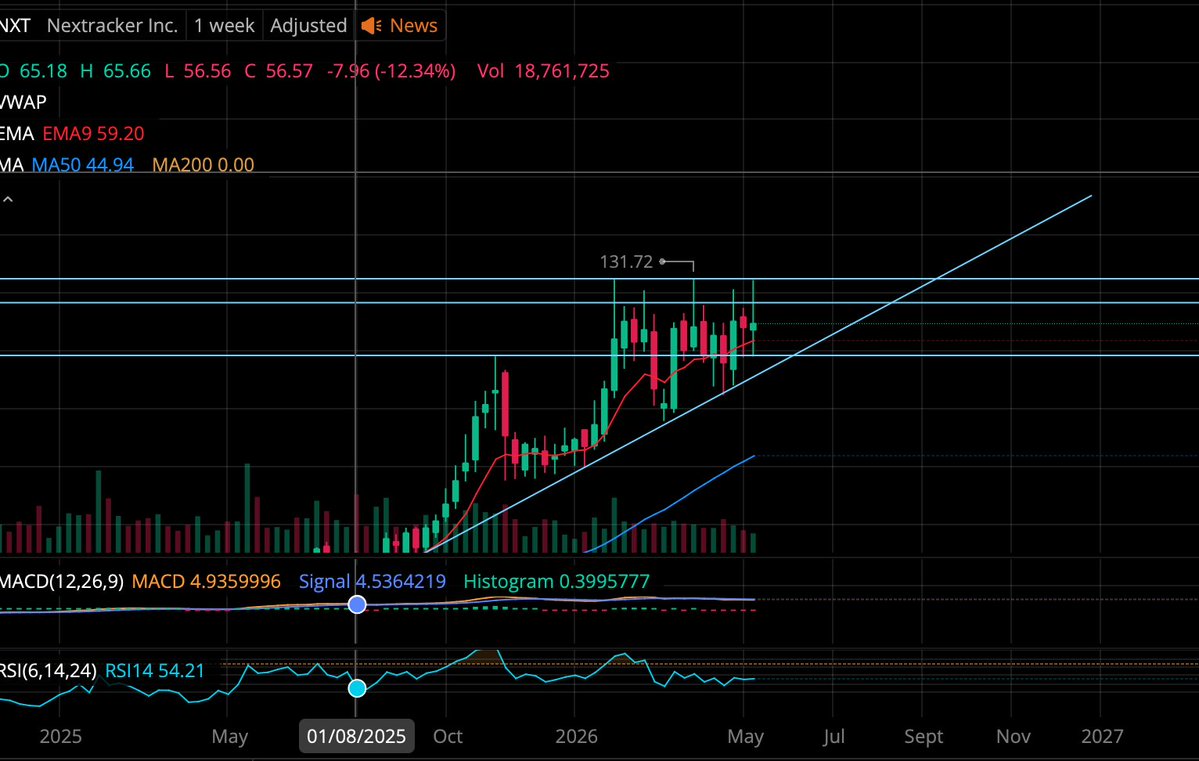

$NXT is reporting earnings today always a scary day to be an investor, i've been loading the 120s now have about 75% of my usual swing size saving the rest for after earnings. The chart is looking super strong and we breached $131.72 yesterday to achieve a new ATH but didn't hold

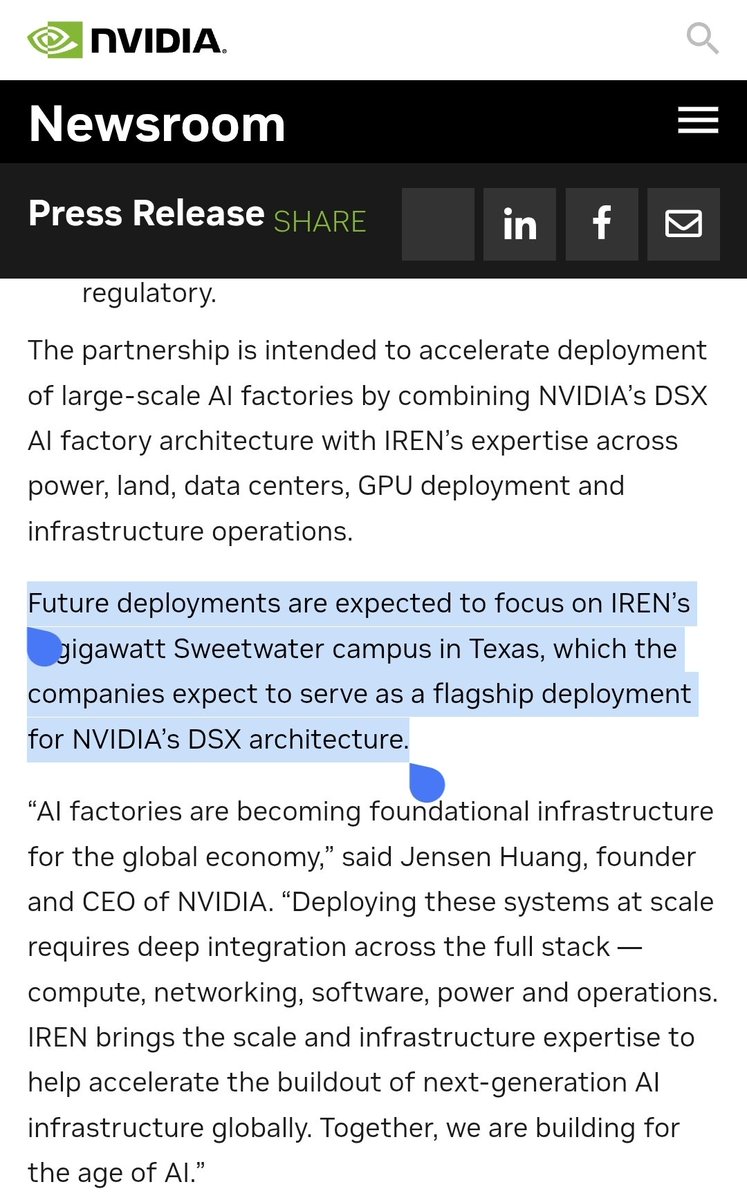

Let’s make a deal with $NVDA so we can hide these numbers - $IREN Big yikes… how do you manage to make less money on AI in this market YoY? $CRWV $NBIS $HUT $CIFR

$NXT, $CSIQ I believe energy will be the next bottleneck I can't see a world where solar is not a big big winner in that, with these two stocks you have one ready to breakout and one already flying, both with earnings next week could be explosive in either direction.will BUY both

Well IREN went off this week, we got a lovely dip and bounce at $42 around the daily ma50 and 200,I reloaded my swing position heavy at 44 and now we wait for earnings and try flip that 63.50.I haven't been this bullish on the stock since the last earnings and that went well.....

my current main swing other than $IREN is $OPEN chart looks very good with a downtrend break and tapping $6 yesterday, swinging this one because of the potential FED change and rate cuts

Sooooo, $TRT just got themselves a new building Let's have a look at the map - where this is located, shall we? Surprisingly enough, it's right across the road with $COHR - one of the biggest potential customers for burn-in they could ask for Coincidence, I don't think so. Now we have 2 massive potential customers: - $AMD - $COHR Yes, I am very long on this. CC: @aleabitoreddit @ParadisLabs @PepInvestStocks

Everyone's focused on $TRT's AI GPU order. They're sleeping on the second engine. Automotive. Here's the thing about cars that most people don't realise: A modern EV contains 1,000+ semiconductors. A fully autonomous vehicle will need 5x more chips than today. And every single one of them has to be burn-in tested. Not optional. Mandated. A chip failure in a phone is inconvenient. A chip failure in a car doing 70mph is catastrophic. The reliability standards for automotive chips (AEC-Q100) are among the strictest in any industry. The market $TRT is walking into: → Automotive semiconductor market: $85B+ in 2025 → Growing to $114B by 2028 (11% CAGR) → Burn-in test equipment market: $789M in 2025 → $1.2B by 2032 → Automotive is the fastest-growing end market in semiconductor testing What $TRT has already done: March 2026 - $2.5M initial manufacturing order for automotive burn-in. This isn't a one-off. Automotive burn-in is a recurring, high-volume contract. Once you're qualified as a supplier, you're in the supply chain for the life of that programme. So $TRT now has two completely separate growth engines: - AI GPU testing, which is already running at $15M+ per quarter - Automotive burn-in, is just getting started Neither is dependent on the other. Both are mandatory. Both are growing. The market is only pricing in one of them.