Tweet épinglé

$PRME Financials Deep Dive and Market Potential Thesis

Prime Medicine is a company that has stood out as having a major potential not only for financial returns, but to the betterment of mankind. This is an absolute core of any investment I make because nothing is guaranteed when investing. If the investment were to fail, being able to hang your head high on the fact that you gave crucial liquidity to a company trying to improve human experience/life, you know that you attempted to push mankind forward in a tangible/meaningful way instead of just accepting the status quo. This is something you can be proud of even if you didn't meet your financial goals with the company. So many of us have/had loved ones that have been told they have incurable diseases that they have to live with or become a subscription model to mega pharmaceuticals, and I have too much faith in humanity that this is the best we can do.

Let me start by saying that this is a high risk/high reward scenario with some competitors and is pushing against current behemoths in modern medicine, which in my mind, treats patients as a reoccurring cash cows that can negate, but not treat many diseases because they are unable or unwilling to.

My initial company love was and is currently $RKLB. I found it as a diamond in the rough as a beaten down stock with a founder that was hell bent on delivering a better launch experience for small satellite companies so that a behemoth monopoly @SpaceX would not control the only keys to space at a time when government entities such as @NASA were faltering to deliver reasonable launch capabilities for the growing private sector. I cashed out my 401k, sold my car, and dropped every dime of liquidity I had into $RKLB and turned a $20k investment into nearly half million shortly after losing my job. I truly think $PRME is the next $3.50 to $35+ story in the making in the market that can benefit human health, as $RKLB is improving human exploration, communication, low/no gravity pharmaceutical development and so much more.

I had people literally laugh in my face as would tell them the market potential of this small launch company, including family and friends. I never circled back for an "I told you so" only engaging with people asking me what's the next company that has the same potential as $RKLB? $PRME medicine has the same precursors as an early $RKLB (which I would highly recommend you check out if you haven't already). Two completely different arenas but very similar when you look under the hood as far as potential.

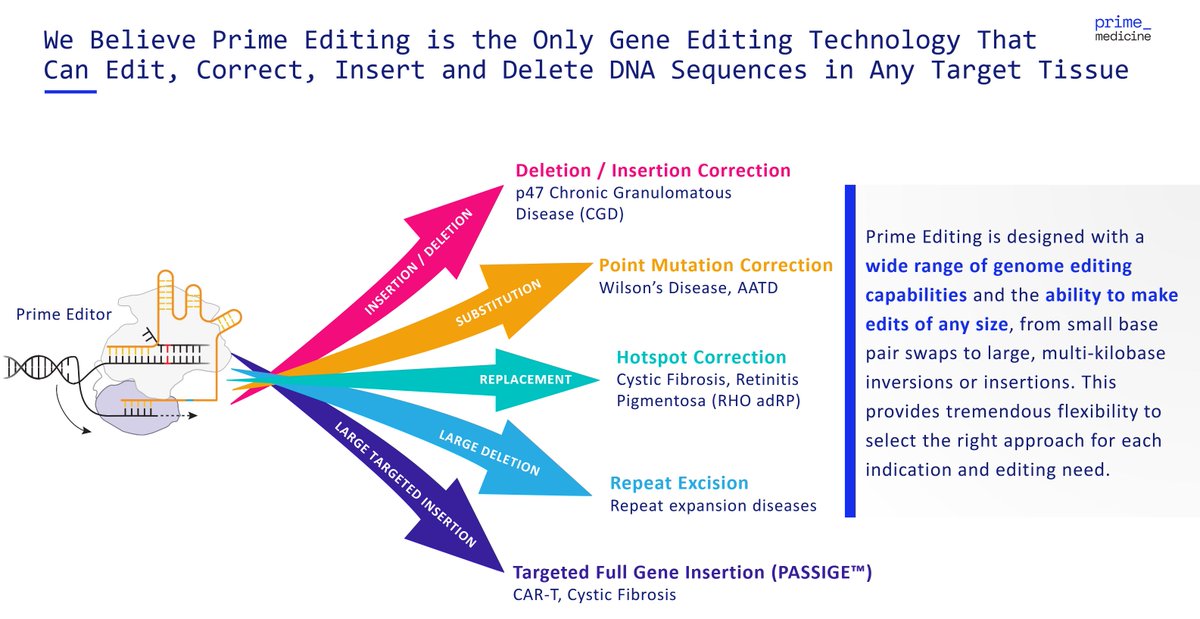

$PRME has the potential to cure many diseases caused by genetic mutations like Cystic Fibrosis, Sickle Cell Disease, Huntington's Disease, Duchenne Muscular Dystrophy, and Hemophilia, Cancer, Diabetes, Alzheimer and so much more. While the proof of concepts are really focusing around Wilson's Disease and AATD (Alpha-1 Antitrypsin Deficiency) currently I see this as the tip of the iceberg that will snowball into all the areas mentioned above and including improving genetics on non-diseases, such as autism, and improving muscular, skeletal and integument (skin) conditions, allergy resistance and SO MUCH MORE. The market cap potential is in the tens to hundreds of billions by 2030.

I am not a genetic scientist, but the multi-prong deletion/insertion, substitution, replacement, large deletion, large targeted insertion approach of $PRME on being able to do what $CRSP does but safer at a much more attractive market cap is highly enticing.

Let's dive into whats under the financial hood shall we? That's why we are all here isn't it...

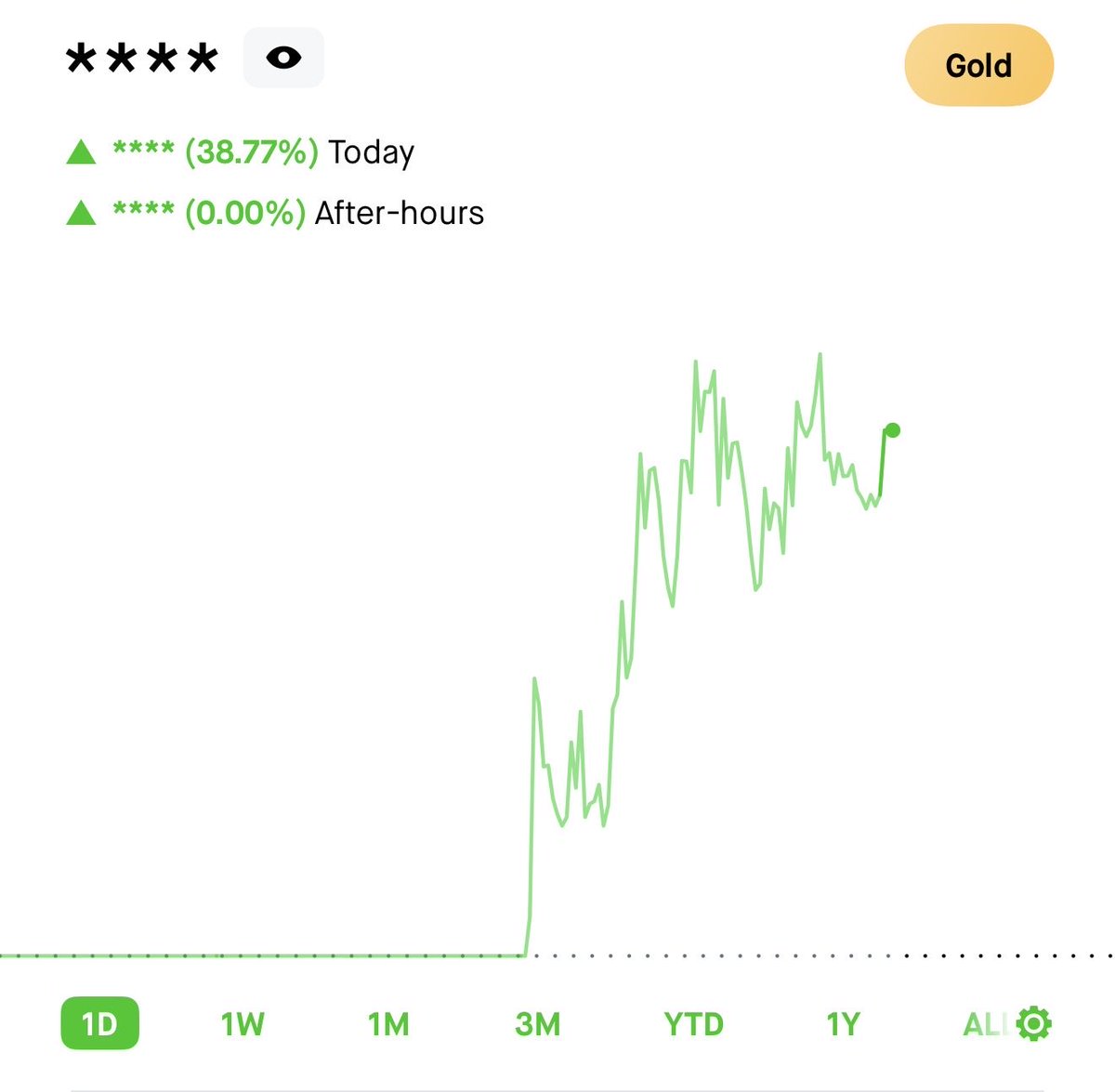

For starters, a relatively low market cap of below 700m as of writing this. A very high short interest of 31.46% reported by fintel, including a off-exchange short volume of 39.64%. Why this is important is I love companies with huge potential that are largely shorted with relatively small market caps so that once the tide turns it can really move against those betting against them in a dramatic fashion ( $RKLB *cough cough* ) and a 8+ days to cover ratio, meaning if an unexpected update were to occur pushing the stock higher, it would take over 8 days to cover the squeeze, especially if it is gamma related (appreciation of calls on the stock).

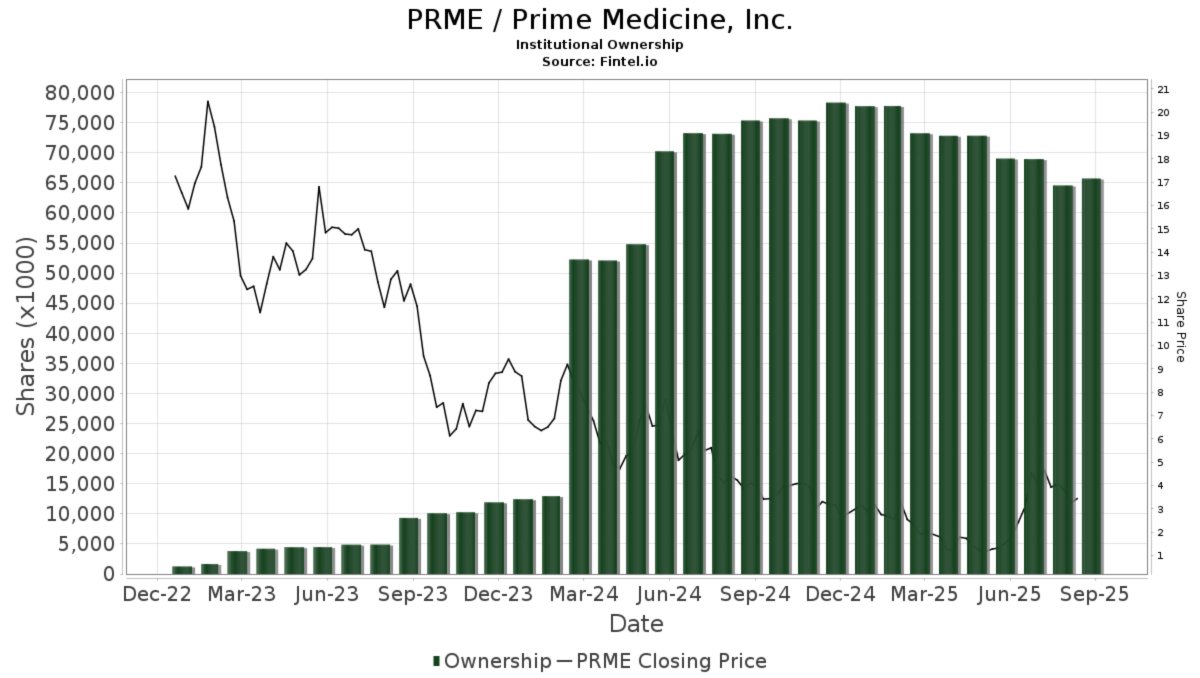

Who has a large stake backing the company? oh Alphabet company, the parent to $GOOGL owns 15m+ shares.. that's an interesting stake in a company that has a 94m public float 🤔👀 now what could they be doing with such a large stake in a genetic editing start up. Don't know, but I like it 😈 also $BMY having a 11m+ size position as of 10/24 is no data point to overlook either.

Not to mention the obvious blocks owned by large institutions like Vanguard and BlackRock who own nearly 10m shares combined. This is pretty obvious, because they own everything that exists, but furthers the core ownership locked in by institutions.

Arch Ventures Partners X and XII who buy disruptive scientific companies has a commanding stake they have only added to which appreciated to over 34m shares. Between Alphabet, Bristol Myers Squibb, BR, VG and Arch Ventures Partners own nearly 70m shares of a 178.2m total float company AND MANY MORE OWN MILLIONS OR TENS OF MILLIONS OF SHARES.

Cash raise just occurred at the end of July/early August to securing delivery of operation runway for the near term foreseeable future.

The CEO is laser focused on delivering on the two pipelines currently that are trying to leap from human testing to developing and procurement. After this occurs it can secure a portion if not majority of the pipeline for 40-50B TAM on Wilson's Disease and AATD which would secure funding for further development of new DNA editing on larger TAM improvements without need for further dilutive offerings.

Now what happens when a company comes out with a permanent cure to a disease that is truly debilitating and under any current traditional medical trajectory would cost tens or hundreds of thousands of dollars for a side effect inhibitor/limiter? I would think that the company could charge astronomical fees in the hundreds of thousands or near millions for cures to these previously incurable diseases/genetic debilitations which I'm sure insurance would be responsible for a large portion of. This would be an insane cash generator for a company that can provide a permanent cure or prevention of millions of patients who would much prefer a permanent solution over a reoccurring subscription pharmaceutical or surgical subsidization.

I have a fairly substantial stake in this company at this point with multiple hundreds of $4-$5 4/26 strikes that will only slam as new chains with further dates are added.

THIS IS NOT FINANCIAL/INVESTMENT ADVICE

PERFORM OWN DUE DILIGENCE/MARKET RESEARCH

I will continue to elaborate on my thesis as my research and understanding develops. This is an initial dive into the company to pique interest and drive your own research.

English