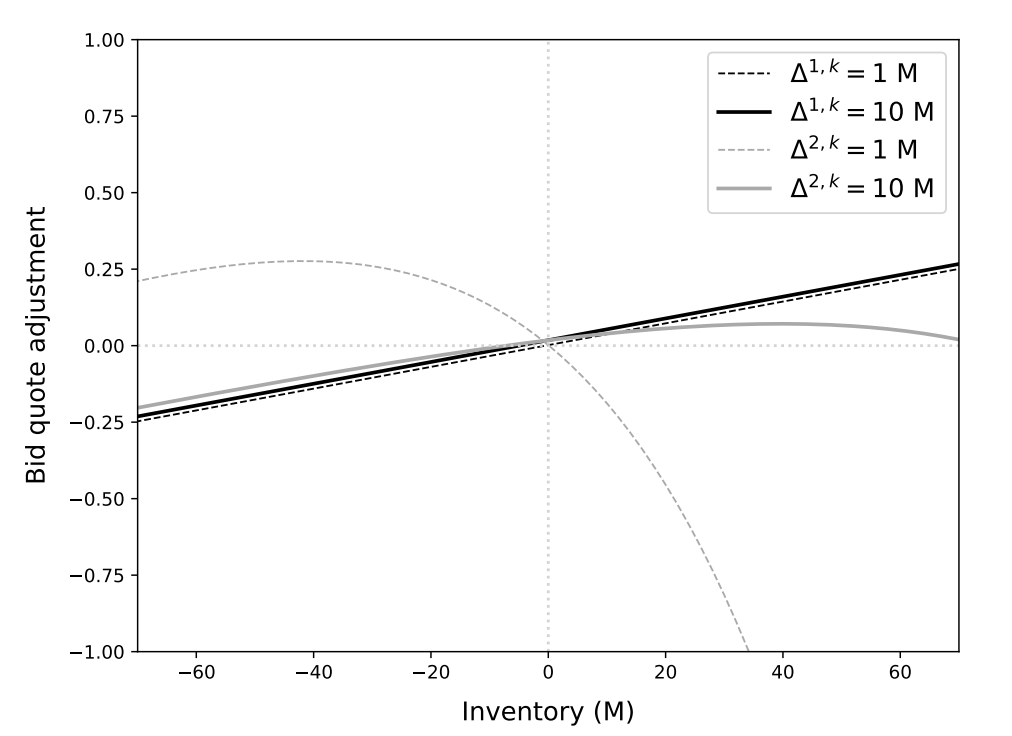

Agree completely...this is one of the principal issues with projects "going public" too soon. One could argue that the token creates too much pressure to reward token holders at the expense of future growth and user experience.

Let's take a profitable Perps DEX for instance: For now they can charge high fees relative to tradFi competitors...but in the history of markets fee compression is the norm, so the current take rates are not sustainable.

They should instead be hoarding balance sheet and investing in lobbying, investing in distribution, and preparing for fee rate wars.

Instead they are buying back tokens to appease token holders who want to see number go up.

Guy Wuollet@guywuolletjr

1/ Buy-and-burn is becoming the default ‘capital return’ strategy in crypto. I think this is a big mistake. Stop it. Get some help. Profitable protocols shouldn’t shrink their balance sheets when they can do productive things instead.

English