Through the oil looking glass

pemedianetwork.com/petroleum-econ…

Persian poet and mathematician Omar Khayyám wrote: “The Moving Finger writes and, having writ, moves on.” The initiation of military operations by the US and Israel against Iran on 3 March was a transformational moment not only for the Gulf region but also for global oil markets — one from which there is no return. No matter how this war ends, or what objectives are ultimately achieved, there will be no reverting to the previous status quo.

At the invitation of @PetroleumEcon, I wrote an opinion piece on the current dynamics of the oil market. With new events unfolding by the hour, it was hard to come up with a thematic that would have a shelf life of more than a half a day. So I took on the idea of how the market achieves equilibrium in these trouble times.

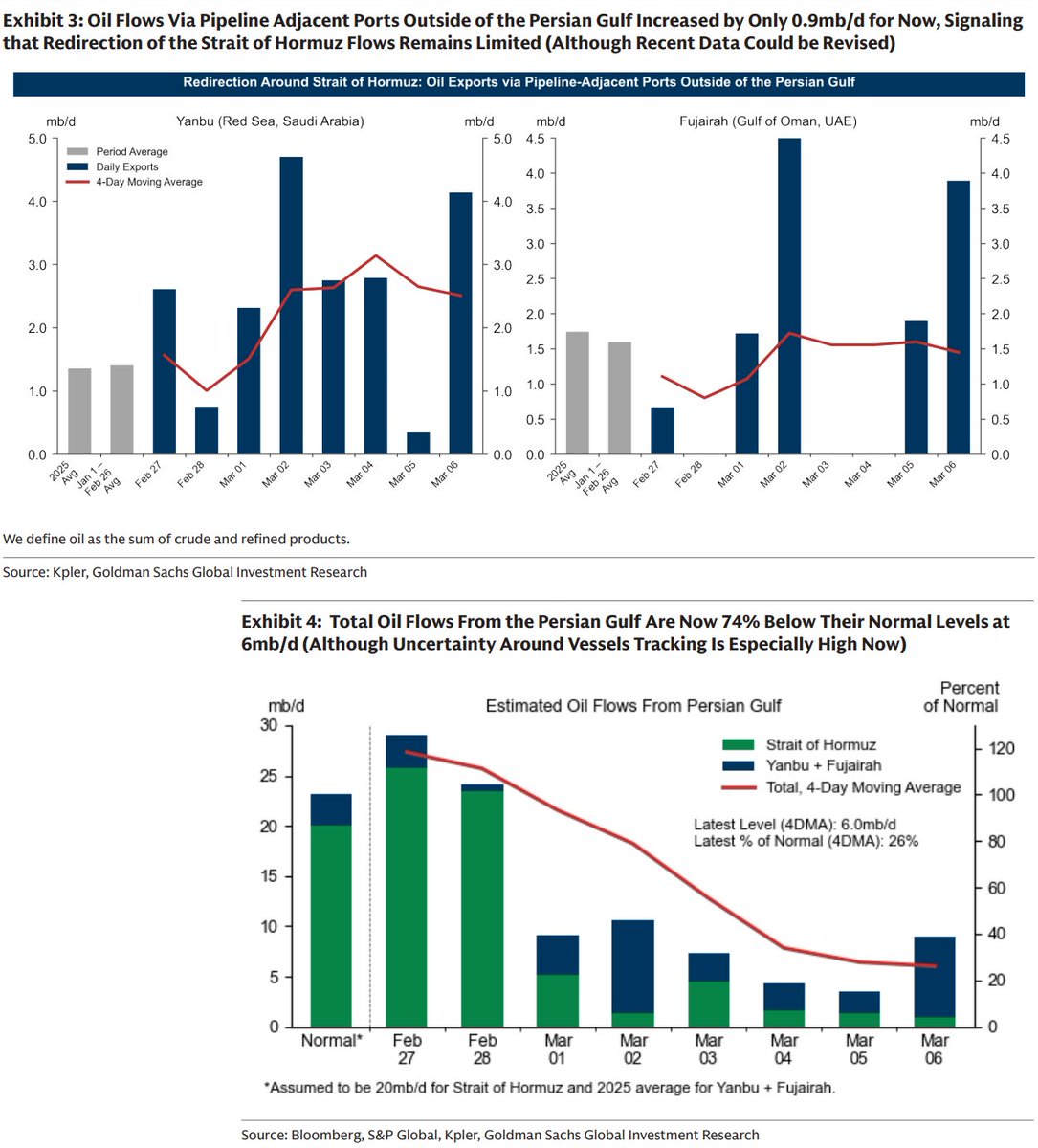

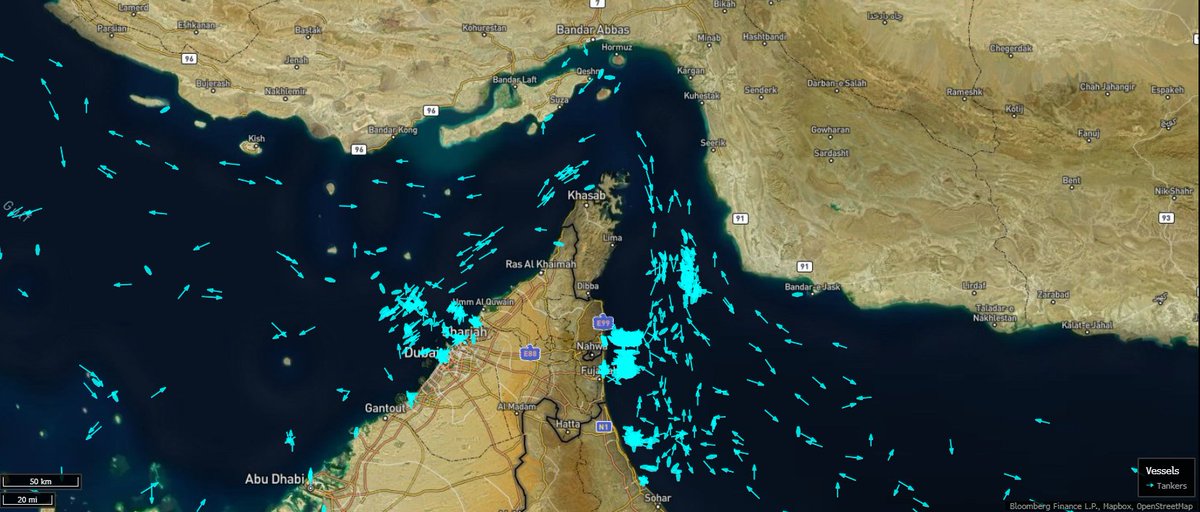

With little scope in volumetric adjustments in current state of supply and demand fundamentals, it is all down to price changes to bring about a equilibrium, albeit even fleetingly. For the lost volumes through Hormuz, quantity-wise, there is no immediate replacement solution to allow the oil price to deflate with speculators selling the fact, having bought the rumour.

The price adjustment in the coming weeks will inevitably be messy as the market tries to separate signal from noise. Brent futures may well ultimately converge towards the physical Dubai benchmark, with a potential move towards $150/bbl. However, in the near term, it is more likely, if no de-escalation takes place, for Brent futures to converge first towards UAE’s Murban crude valuation, which recently crossed above $125/bbl, before it takes aim at catching up with Dubai. This, in my opinion is likely to come even as Treasury Secretary Scott Bessent dismisses rumours of intervention in financial oil markets and raises the possibility of easing sanctions on Iranian crude already on water and conducting unilateral US SPR releases.

#OOTT #OIL #BRENT #US #IRAN

English