Tweet Disematkan

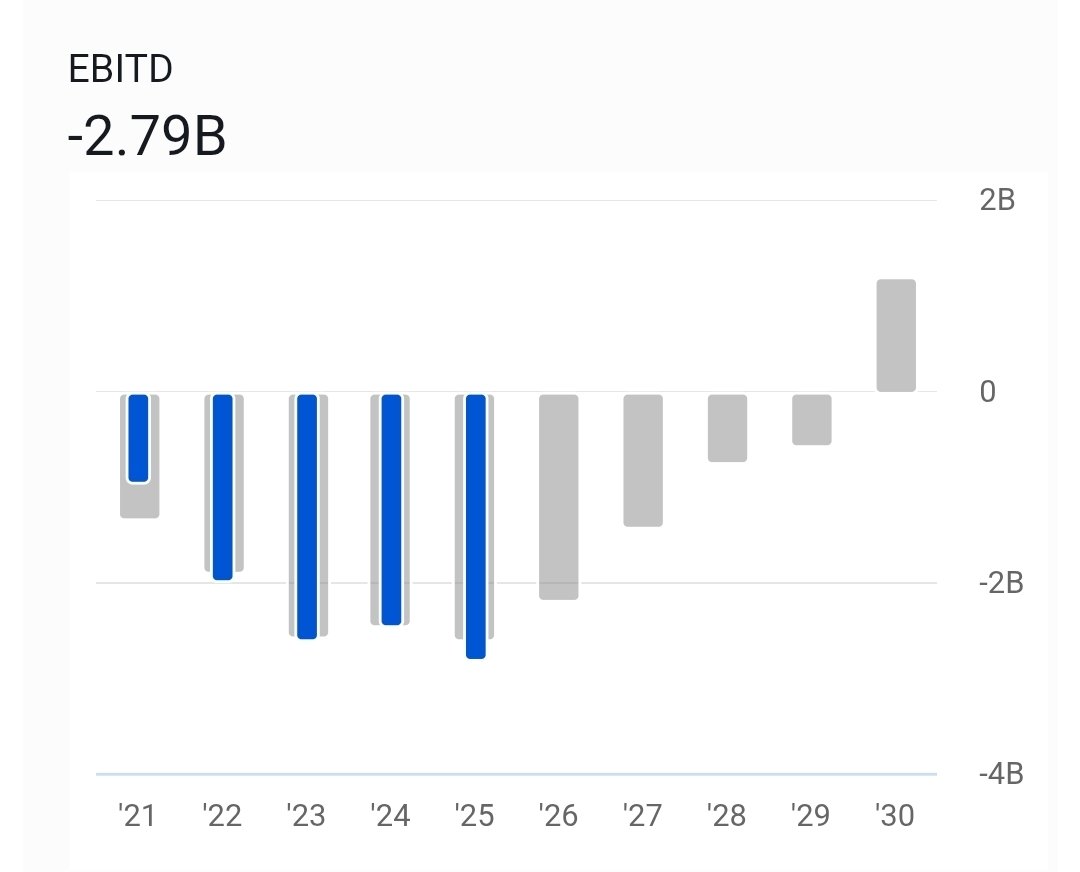

Most EV analysis covers who's winning. Very little covers why the losses exist, what they actually mean, and which companies are being misread by the market.

Spent weeks going through filings, Investor Day presentations, and building scenario models. Sharing the most surprising findings — one per day. Full research package follows, including scenario models with breakeven timing, dilution analysis, and stock price implications.

$LCID $F $GM $STLA

English