Tweet Disematkan

1/N

Li Lu's is only person Munger trusts with his money besides Buffett. He has a simple investment checklist

Is that a good business?

Is that Cheap?

Who is running it?

What did I miss?

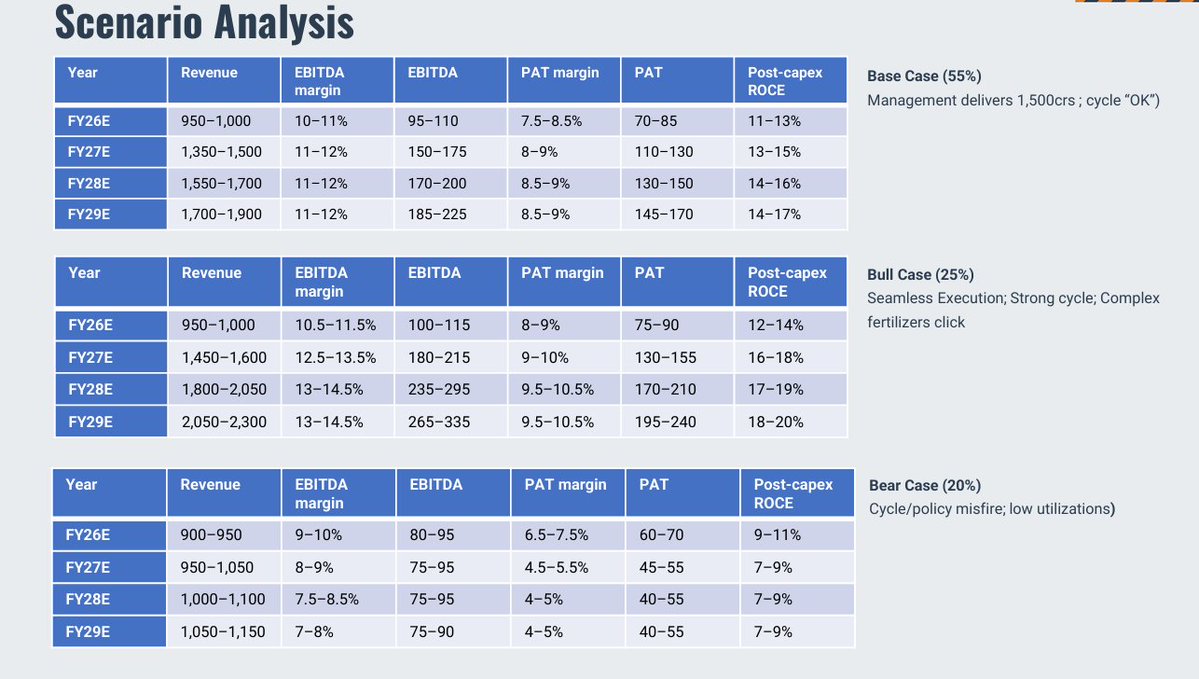

Using this lens, l will look at #Apar Industries

English