Brett Caughran@FundamentEdge

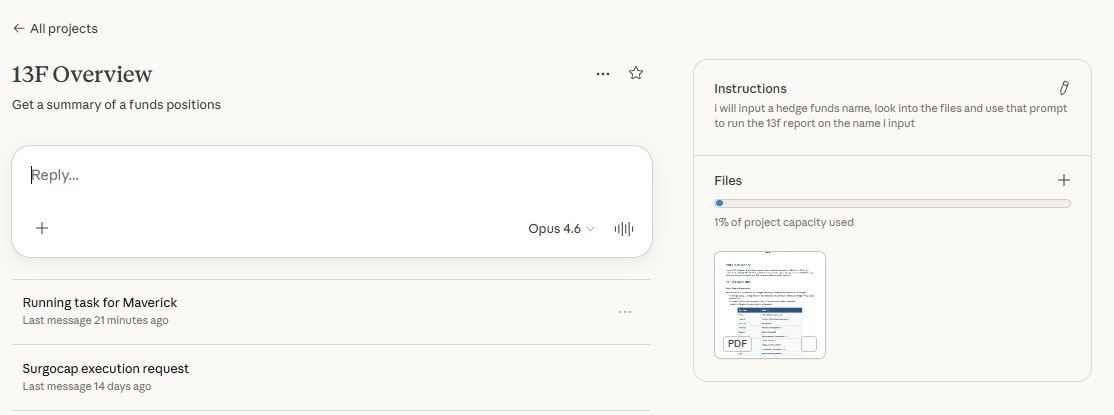

AI Workflow: 13F Top Holdings Report

One thing I like to do when I'm looking for new ideas is to check the 13Fs of a few dozen hedge funds I respect for new & high conviction ideas. While I don't want to outsource my thinking, there is no copyright protection on a great idea, and the funds I choose I know to have strong due diligence and a thoughtful portfolio inclusion process. Which is a positive signal, on balance. (And one of my favorite personal strategies is a biotech 13F overlay which has a crazy good 15 year back test...post-COVID hangover notwithstanding...though XBI breaking out...???).

This is sort of a clunky process in FactSet (and in Bloomberg) where even getting to the right legal entity can be a pain. Pretty much just for UI purposes, I have been a Whale Wisdom subscriber for years (which still isn't great, but better than Bloomberg/FactSet). I've long been searching for a better alternative.

So I've been playing around with an AI workflow solution to this problem, seeking to create:

- A short PDF I can read in 5-10 minutes

- Starting with 13F-sourced data on top 20 holdings

- AI generated summary thesis on those top 20 holdings (i.e. why the fund likely owns the position)

So in 5-10 minutes I can get a quick check on the highest conviction names at a fund and quick analysis on the position. Efficiency is important when doing this ~35 times, 4 times per year. 35 x 45 minutes (i.e. see the position, read 1-2 sell-side notes on the name) is a lot different than 35 x 10 minutes (i.e. quick AI-generated thesis).

The cool part is I can take this report then drop it into my AI "Up to Speed" workflow and go even deeper, such as identifying dates for binary catalysts for biotech ideas, or asking for the 3 key drivers for a name.

This is a pretty challenging task for AI, because I am demanding the LLM identify the correct legal entity from the generic name (which FactSet mostly cannot do) go to EDGAR XML filings, integrate some market data, format it well, the write "Why This Position Makes Sense", "Recent Developments Supporting the Thesis", and "Position Sizing Context".

From my prompt:

I tried this a few months back and it didn't work. I decided to try it again this morning, and here are my results.

ChatGPT 5.2: Awful, and awful in an annoying way. Finally admitted it couldn't do it in a single normal churn task. Overly, annoyingly apologetic, then just keeps not doing what you ask.

Gemini 3: Better, but lazy. Gave me a summary of position 1, 4 and 7, but completely skipped the other ideas. Fail.

Grok: Better, but still not good. I'd say close, but still fail.

Claude Opus 4.5: SHOCKINGLY GOOD. Missed on some of the market data requests (% of ADV), but pretty much fulfilled the request exactly as I requested, creating an easy to read summary of a fund's Top 20 holdings and a guess as to why they hold the idea.

I will drop the prompt and a few sample reports in the replies if you want to re-create this.