Sabitlenmiş Tweet

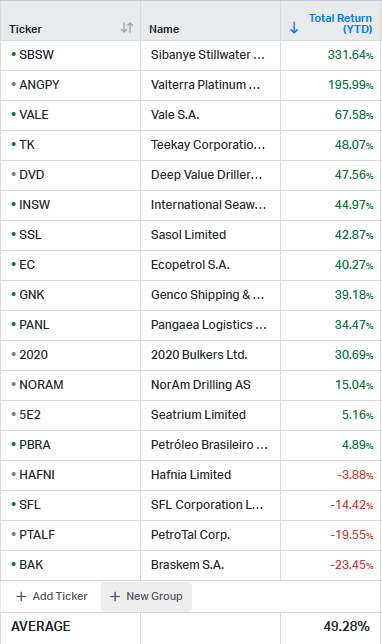

And 2025 is a wrap! Here were our 2025 picks

Not pictured is Seabird Exploration, which was acquired mid year up > 50% (good for 100% TWR)

Average pick returned ~50% for 2025, with 4/20 names providing a negative return

Best pick returned > 300%, worst pick returned -23%

English