Commodity Adjusted EBITDA

145 posts

Commodity Adjusted EBITDA

@FCFNextYear

Always Running Mid-Cycle Pricing. Former Sell-Side Analyst. Roaming around the private markets now. Not Investment Advice

参加日 Ocak 2018

1.2K フォロー中478 フォロワー

$SU has a refining complex geared to take the heavier crude barrels they produce upstream. So, the average distillate yield across their downstream unit is higher than most NAM refiners. With the current conflict, one should expect the diesel premium over gasoline to continue to widen, disproportionally benefiting refiners producing more middle distillates.

English

Been slowly adding to our O&G exposures to hedge out a nasty 1970s oil shock. Not fully committed yet, w/ each escalation, ramping up our exposure. Would love ideas

$SU - Canadian oilsand low cash cost

$DINO - Inland refinery/lube

$XOP - Calls

$JOY.TO - Small cap E&P

English

@compoundpapi Tangible book, beware the goodwill impairments of ye olde roll up strategies

English

@FPLofC Thanks Diaper Lord

Which PE firms in Canada want to go retail?

Besides Brookfield

English

Happening at quite a few shops in Canada.

@OPMWire

Unicus@UnicusResearch

🚩BREAKING: Private Equity is desperate to tap into retail they are offering UBS HNW distribution a cut of the carry. Trust is forever lost. HNI and UHNI must push back. High conflict of interest. “They are very aggressive with how they push this” on fund managers, said another top private equity executive about UBS. At least two other managers of major private capital funds for individual investors declined UBS’s requests to share their fees This is very bad. Now, they are scrambling for exit liquidity. ft.com/content/2a1805…

English

This is basically the defining feature of this entire asset class, not a bug

English

@compoundpapi Flight to quality in times of uncertainty 😂😂😂

English

Commodity Adjusted EBITDA がリツイート

Seeing wider confirmation of this now.

Big deal, especially right now with Iran.

Ukraine either just accidentally really overplayed its hand, or is very intentionally playing serious hardball at a perilous moment for the global oil market.

(((Tendar)))@Tendar

Ukrainian projectiles successfully struck port infrastructure in Novorossiysk, Russia. Likely the terminal for oil loading has been struck.

English

@marketplunger1 what is the life of mine? asking for my PA

English

Claude can now build an open pit copper mine from exploration to production.

Amazing.

English

@ErnestWongBWM Appreciate the engagement as well. I see that you're across the alt managers. If you want to chat about them any time, please reach out.

English

$BAM getting thrown out with the bathwater. The issues are in retail private credit... products that bundle risky loans to retail as safe and high-yield.

BAM/Oaktree's focus is opportunistic/distressed credit for institutional investors and would benefit from weak times.

English

$APO and $KKR both also have attached B/S. $APO harps on this all the time that they are "principals". While I would rather have the alignment than not, credit is ultimately a competitive and commoditized business so, differences in portfolio quality can only go so far. $OWL also has to remain disciplined because they need to be able to raise the next fund etc. $BAM's performance mirrors that of $KKR and $APO which is not "throwing the baby out with the bathwater" given concerns broadly across credit.

English

@FCFNextYear Where we disagree is that the incentives are quite different.

Because BN owns the balance sheet and all the execs have all their wealth in BN stock, they are highly incentivized to be prudent on both underwriting and investment.

If you're just clipping fees, it's all gravy.

English

The difference in earnings growth and ROE motivation is semantic, capital light earnings growth also boosts ROE. Arguably owning the B/S is worse because instead of just loosing the fee stream if u/w is poor, you're levered B/S could get into trouble. Private credit like private and public equity is a commoditized business. All the big players in the arena have great pedigree (survivorship bias). $APO, $ARES, $OWL, $BAM. The $OWL Co-CEO and Co-founder previously founded, built and sold GSO to $BX before starting fresh. Its all one trade and that's why $APO and $ARES and all the alt-managers are suffering. The market is rightfully concerned as the flood of $ esp. insurance capital has led these managers to compete down spread on loans arguably increasing risk across the board.

English

@FCFNextYear I think the bigger issue is around the quality of the private credit book, the valuations, and the ability to raise capital going forward.

In these aspects, I don't see much resemblance between Blue Owl and BAM.

English

Also not how that works. Insurance balance sheets have to be ~90% investment grade fixed income. This is where $APO's concept of private investment grade came from. AEL (BAM's latest acquisition) at YE 23 touted that 25% of their investment portfolio was in private assets (read mostly IG FI). It is not therefore Oaktree's opp./distressed credit. Would also note that $OWL bought part of that loan portfolio with their own AM who manages insurance capital. So, again the businesses are very alike.

businesswire.com/news/home/2024…

English

@FCFNextYear They are investing in their own funds, not stuff like Blue Owl

English

Have really enjoyed the the engagement on X recently, h/t @compoundpapi. I’m a former Canadian sell-side analyst energy analyst that has spent the last few years in private energy/infrastructure investing. I want to stay sharp in public markets and contribute to the community. Thinking of doing some more long form content. What should I write about first?

Poll is glitchy please comment or DM suggestions. Was thinking:

1. Current sector outlook

2. Single Name Deep Dive

3. Investment Philosophy

4. Active Management vs. Private Assets

English

@compoundpapi @Greenbackd $HRX.TO (Platinum Equity), DNTL.TO (GTCR) and $NVEI (Advent) immediately come to mind. Quality businesses, unique business models (in the TSX context)

English

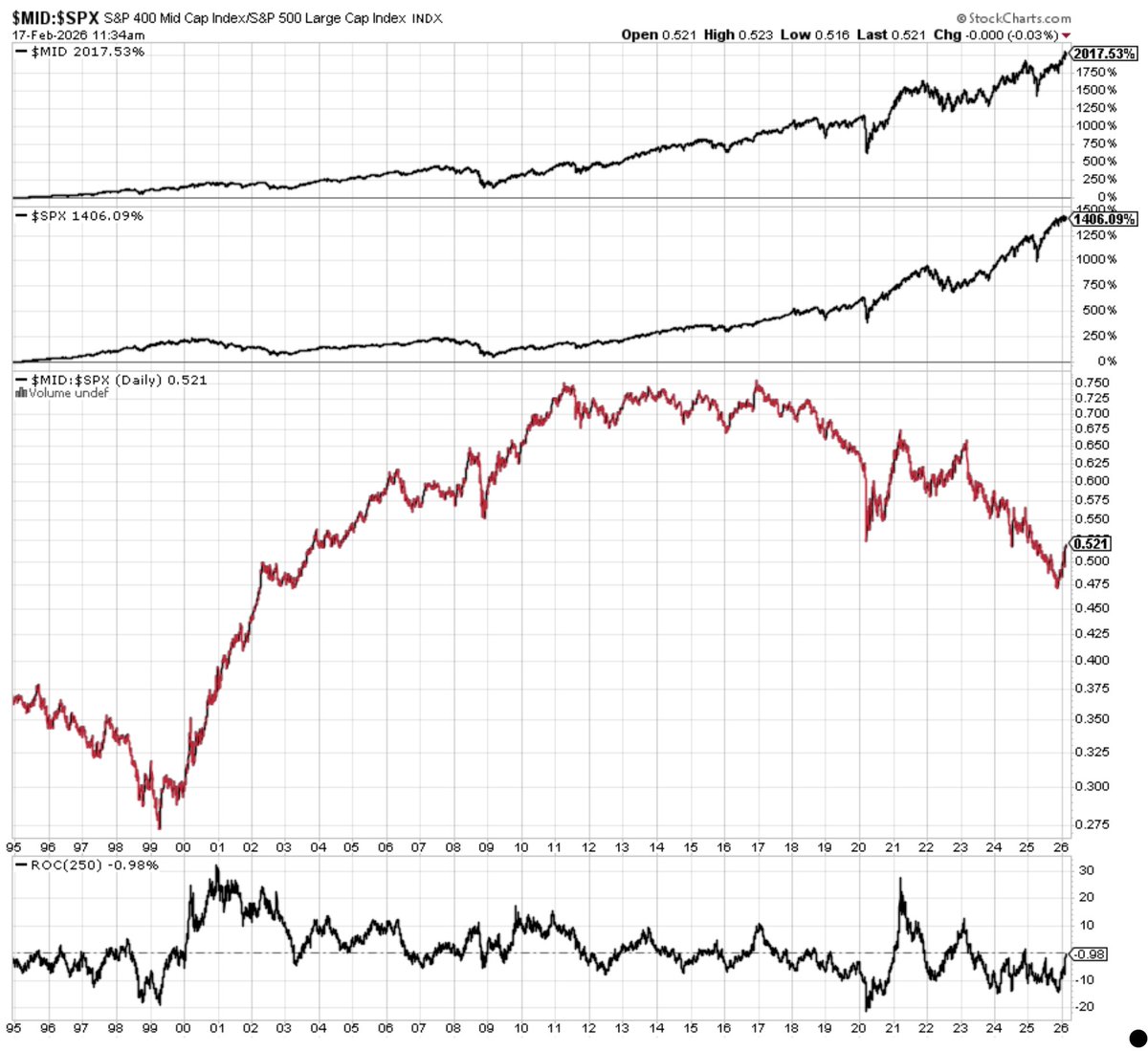

Midcaps have outperformed the S&P 500 over the last three decades but have underperformed since 2011-2017.

Mids have looked a little perkier since late last year.

Is the midcap renaissance here?

English

Commodity Adjusted EBITDA がリツイート

Haven’t followed closely for years. Pitched $CMG.TO as a short many years ago to land my first job. The concept that this was gonna be O&G CSU was beyond laughable to me. That said, it is a cyclical business, growth will be lumpy and swinging the target multiple around when you hit trough earnings doesn’t really make sense. I Always run mid-cycle pricing on normalized earnings for cyclicals. Whether 18x is the correct figure I have no idea because I have no context on underlying EBITDA forecast.

English