Sabitlenmiş Tweet

My new book Soldier of Fortune: Warren Buffett, Sun Tzu and the Ancient Art of Risk-Taking is now available via amzn.to/3JfCPBq

English

Tobias Carlisle

23.6K posts

@Greenbackd

PM, Acquirers Funds® https://t.co/rjHtXEy6u0. Author, Soldier of Fortune (https://t.co/qm4uyNXH4Q) and Acquirer's Multiple (https://t.co/84Cyi4XIC5).

"When investing, pessimism is your friend, euphoria the enemy." — Warren Buffett

BREAKING 🚨: Berkshire Hathaway $BRK.A is now underperforming the S&P 500 by the same margin it was during the run-up to the Global Financial Crisis 🤯👀

S&P 500 Call Volume soars to new all-time high 🚨🚨🚨

we are dying.

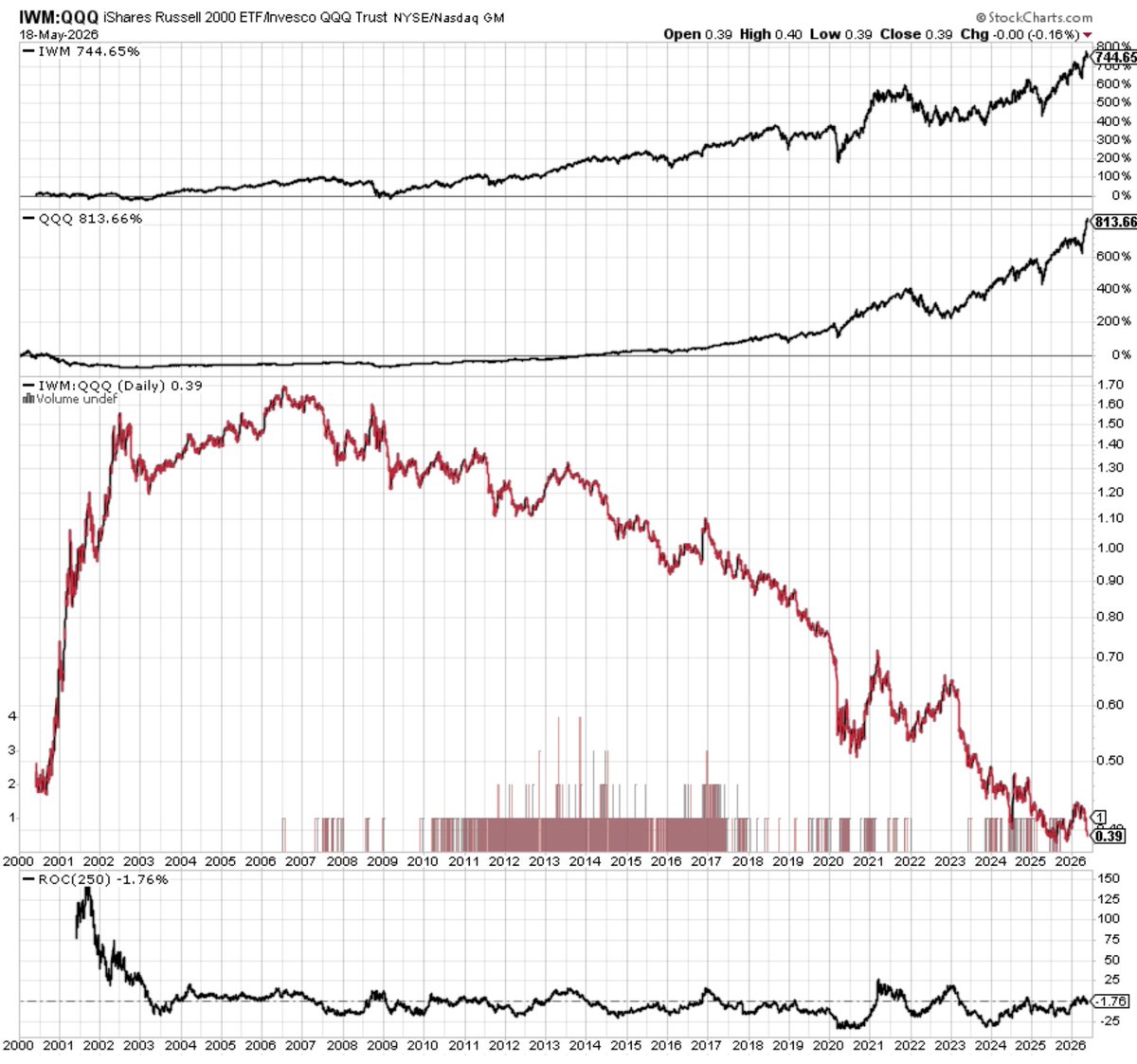

Equal-weighted NASDAQ 100 is sitting right near a record low relative to the cap-weighted NASDAQ 100

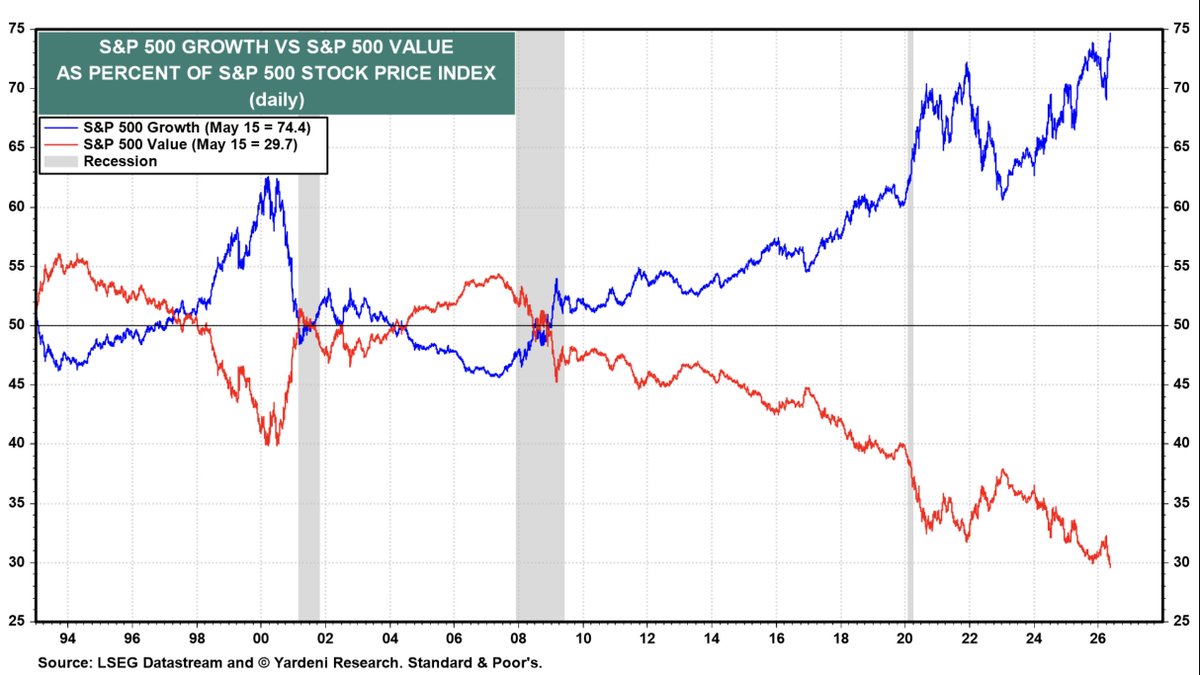

Small Caps are turning into Ignored Caps.. they used to have 10% asset share in ETFs.. that's been chopped down to 4% and now they're finally outperforming and no one cares. Flows non-existent in ETFs and in MFs they've seen $25b in outflows. It's almost not fair. Good stuff today on it from @psarofagis and @DavidCohne

Global value stocks are less than 15x earnings... but that P/E is actually well above the long-term average GS