固定されたツイート

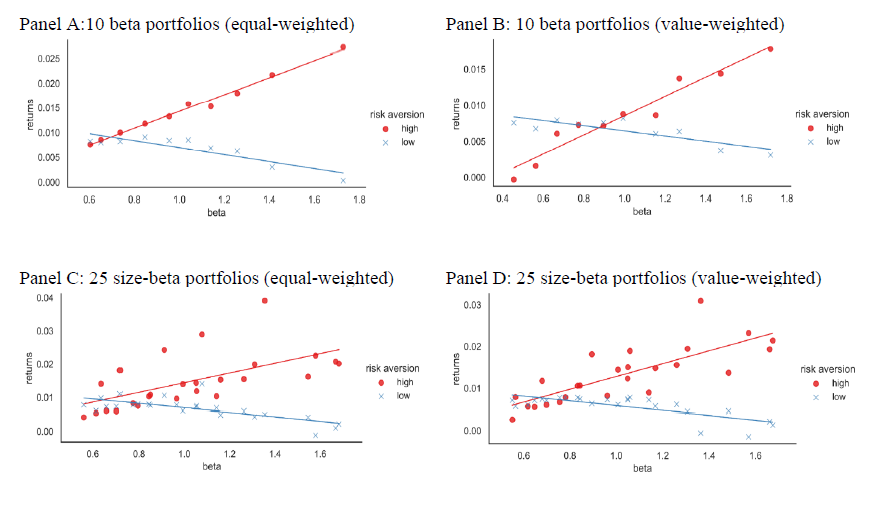

Cue the “Average SP500 Returns After $VIX > 30” charts. Here’s ours: muhat.com/blog/volatilit…

English

Mu Hat Capital

22 posts

@Muhatcapital

Mu Hat is an institutional IM building quantitative portfolios that target superior risk-adjusted returns | Open to QPs only | Not financial advice.

Our editor, working on our "Messy Jobs" manuscript, was not amused when I told him that his beloved em dashes were (mostly) forbidden, because people had learned to read them as a sign of LLMness. After some back and forth, he reluctantly accepted with the following message.

Cue the “Average SP500 Returns After $VIX > 30” charts. Here’s ours: muhat.com/blog/volatilit…

⚙️ New research! "Learning-to-rank vs. predicting expected returns". One works much better. Lin, Su, and Zhu compare two approaches to building long–short equity portfolios: Standard method: estimate expected returns, then sort stocks. Their method: directly optimize stock rankings. Results: → Learning-to-rank: ~1.5–2.3% monthly excess returns, Sharpe up to 1.2 → Standard return models: 0.35–0.7 Sharpe The reason is clean: when you optimize for returns, you optimize for something you estimate poorly. When you optimize for rankings, you optimize for something more robust, relative ordering. The gains come specifically from better identification of top and bottom stocks, and from better hedging. The method doesn't need better return forecasts; it just uses the available information more efficiently. This is a methodological contribution, not a new signal. But methodology is often where the edge actually lives. 📄 Paper: papers.ssrn.com/sol3/papers.cf… --- → Join the newsletter: ivanblanco.ai/newsletter ---

Cue the “Average SP500 Returns After $VIX > 30” charts. Here’s ours: muhat.com/blog/volatilit…