𝐀𝐠𝐫𝐢𝐩𝐩𝐚 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭𝐬@Agrippa_Inv

New $IREN Deep Dive: Childress Unlocked

I’ve spent the last couple of weeks writing the most important $IREN deep dive I’ve published to date.

Air-cooling at Childress is a MUCH bigger deal than the vast majority of investors and analysts realize.

Honestly, $IREN price targets across the board should be well above $100 at this point. But Wall Street missing the forest for the trees is nothing new.

I’ve extensively modelled out the company’s near-term pipeline using conservative assumptions (below management’s guidance), and it’s clear as day that the market isn’t properly pricing in $IREN's industry-leading earnings power.

$IREN is going to make BILLIONS of actual net income over the coming years… not just meaningless EBITDA or top-line figures, but real profits flowing to the bottom line.

If anyone is the next hyperscaler, it’s $IREN.

Remember, real hyperscalers are actually profitable…

At the same time, every investor should be aware of looming industry risks that affect all neo-clouds in the sector and evaluate how they could impact the investment thesis.

That’s exactly what I’ve done for all our readers.

These are the topics this new report covers:

➞ Breaking down the new GPU orders + new guidance

➞ Implications of air-cooling

➞ Extensive pipeline modelling

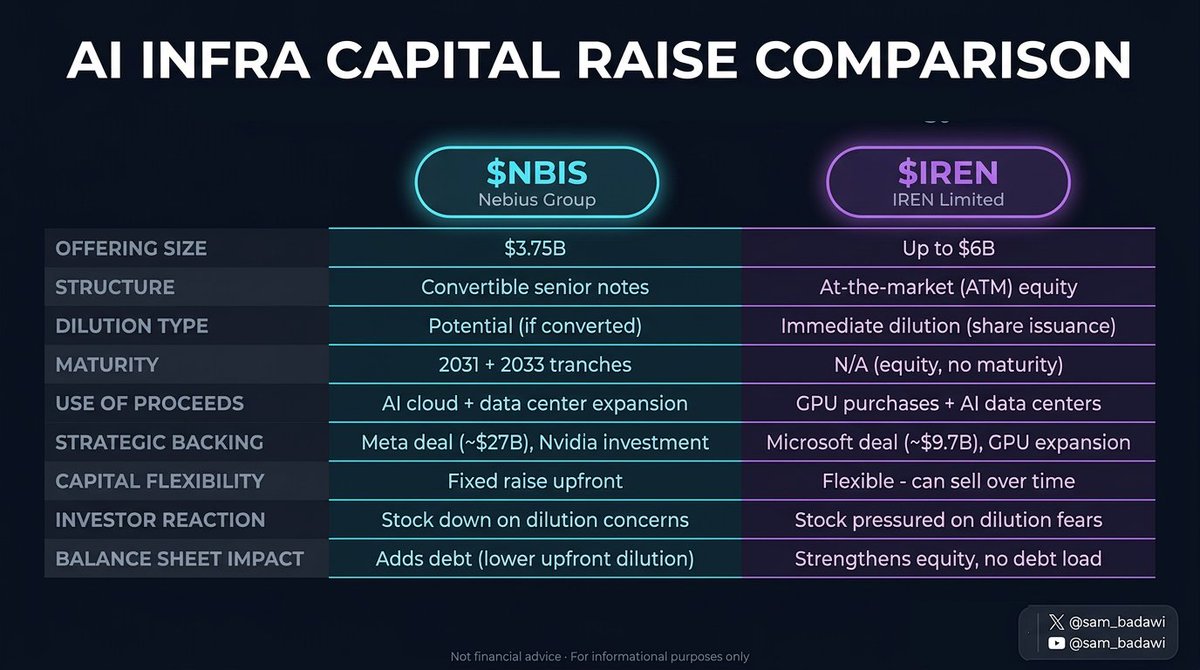

➞ Comprehensive analysis of the new $6b ATM

➞ Risks to the investment thesis

➞ + Plenty of bonus topics

This 40+ page mega deep dive covers everything $IREN investors should be aware of today.

It’s written in a very reader-friendly way, with many graphics & embedded video clips throughout.

I chuckle when I read so-called “analysts” on X give their takes on $IREN after doing nothing more than surface-level analysis (at best).

Most investors have no idea where this is heading…

If you’ve read the new deep dive, I’d love to hear your feedback in the comments.

Appreciate all of you, cheers! ✌️

agrippa.investments/p/iren-childre…