oneatom12 がリツイート

Looks like a strong growth sector

😎😂👍

Barefoot Student@BarefootStudent

Job and employment scam losses jumped from $90 million in 2020 to $501 million in 2024, per Forbes.

English

oneatom12

545 posts

Job and employment scam losses jumped from $90 million in 2020 to $501 million in 2024, per Forbes.

@Guv999 Thank you again for all the call outs. My wife is now asking me if she can go shopping……

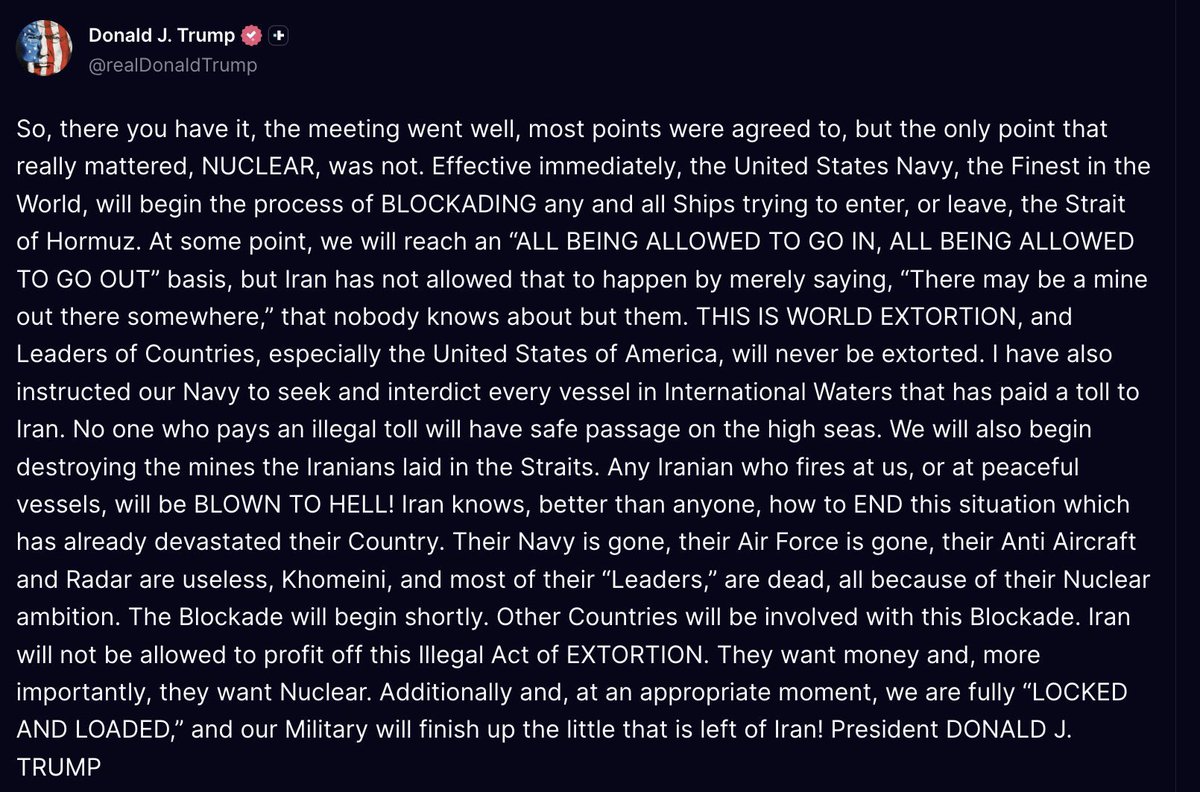

JUST IN - Trump orders the U.S. Navy to blockade the Strait of Hormuz to "any and all ships trying to enter, or leave." Also instructing the U.S. Navy to seek and interdict every vessel in international waters that has paid a toll to Iran: "No one who pays an illegal toll will have safe passage on the high seas."

There is our sweep of the .20 lows and a beautiful reaction thus far. We can see that the purple zone acted as resistance (as expected) three times, ultimately leading us to that sweep we were looking for, and now we are testing the purple zone for the 4th time. Clearing this zone could trigger a strong move up as we have now built up liquidity all the way up to .27-.30 and we have finally taken the liq to our downside. $CRV

IRAN'S PRESIDENT PEZESHKIAN SAYS ISRAELI STRIKES ON LEBANON VIOLATE CEASEFIRE AGREEMENT IRAN'S PRESIDENT PEZESHKIAN SAYS ATTACKS ON LEBANON WOULD DEEM CEASEFIRE NEGOTIATIONS MEANINGLESS