고정된 트윗

ΞVLVΞ.hl

6K posts

ΞVLVΞ.hl

@EvolveWeb3

You wasted $150,000 on an education you coulda got for $1.50 in late fees at the public library.

가입일 Eylül 2021

2K 팔로잉114.4K 팔로워

@BosevskiGorgi That's impossible it is a Schedule I drug meaning there are no possible medical uses of any kind and you should go to jail

English

Last fall I took MDMA with my entire family.

My dad cried for the first time in my life and stopped drinking. My mom apologized for things from high school. My sister and I finally understood each other.

We've been different ever since. One night undid 28 years of walls.

English

@damskotrades What scale is this? cant find any exchange where price is under that 10/10 level

English

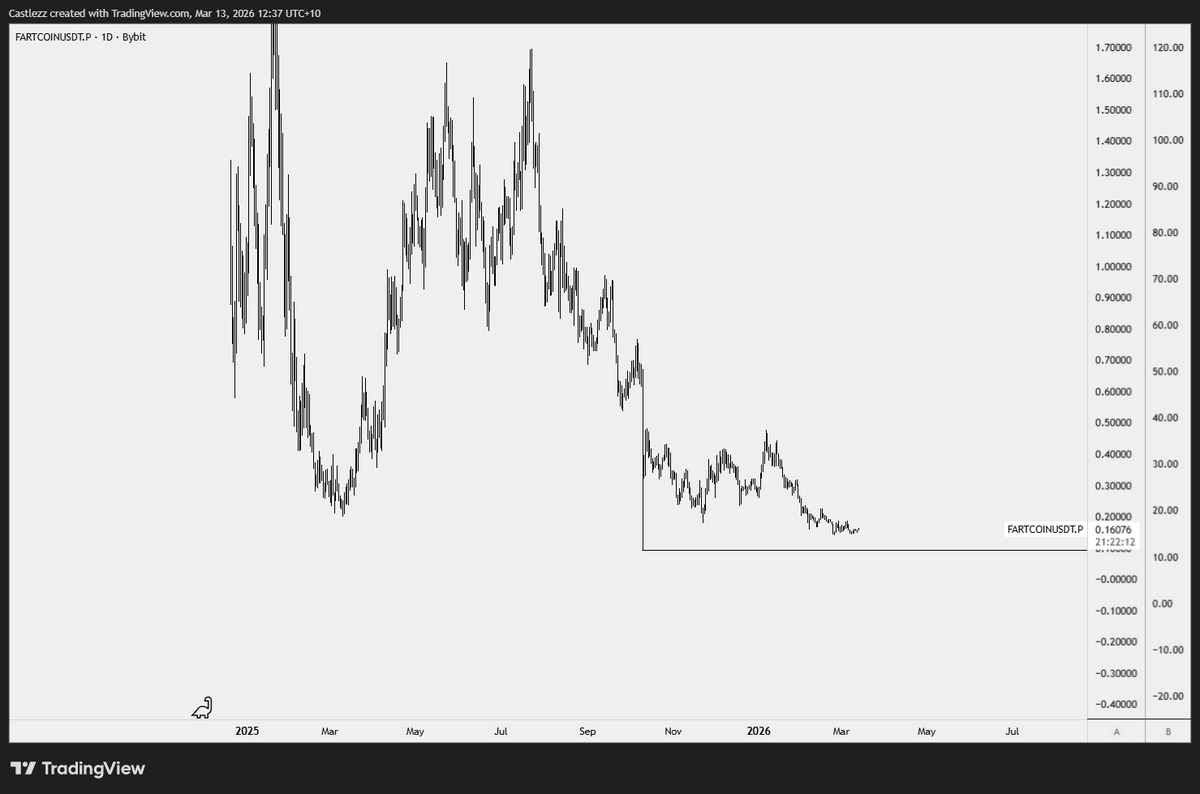

Another example is FART

1. Filled 10/10 wick with slow grind/chop

2. Currently still below the lows

3. Wait for the reclaim and trendline breakout

Bonus: It's around a key level.

English

HYPE pumped 55% on this setup.

→ If we get more relief, this is one of the cleanest setups to watch.

→ More relief → More to print on a similar structure.

1. Fill 10/10 wick

2. Take out lows

3. Reclaim

4. Break structure/trendline/reclaim local level

(1/4)

CryptoAmsterdam@damskotrades

// HYPE Still one of the strongest in our market. Poking above and attacking the $36 resistance again. Clear close above and we’ve got a good case for higher prices. Let's see if we can get that close above.

English

@ThinkingUSD there are a tone of small accounts long with smart money short against them

English

@ThinkingUSD dollar-weighted positioning at 24th pctile suggests negative funding reflects smart money short, not crowded

English

If you're the guy running the PURR DAT you should probably rip it in here and keep the funding rate negative on HYPE. There's no reason to wait. As of the last earnings report they still had $150,000,000 of cash. If you need extra income you could sell covered calls but nobody wants a DAt that's half cash.

English

Massive drop.

Heavy negative delta.

Liquidations into the low.

Looks aggressive.

But is it enough?

When you pull the volume profile, one thing is clear:

We’re trading outside value.

That changes the question.

It’s no longer:

“Was that a big selloff?”

It’s:

“Can we reclaim value?”

Because acceptance back inside value

= the selloff was emotional.

Failure to reclaim

= this wasn’t panic. It was repricing.

Liquidations alone don’t confirm direction.

Negative delta alone doesn’t confirm continuation.

What matters now is acceptance.

Reclaim the value area → balance returns.

Stay below → inventory shifts lower.

Wait out the storm.

Let the auction show you where business is accepted.

English

ΞVLVΞ.hl 리트윗함

$FIGHT Airdrop Eligibility Checker is now LIVE 🔥

Powered by @jup_mobile

See if you are eligible 👀👇

English

@SemanticLayer @Polymarket any $POLY rewards that are earned as a result of me using season 2 will be claimable by me?

English

Prophet Arena Season 2 is live and user agents are finally in the arena.

For the first time, you can deploy an onchain intern that mirrors or fades the big AI models on @Polymarket

Spin up your copy or counter trading strategy at: 42.semanticlayer.io/prophet-arena

GIF

English

@yunaintern Man sorry to hear this, did you have that 300k in a hot wallet or was it ledger secured?

English

I have been working on a momentum scalp strategy based on your scanner you did with BTC Charlie.

Scanner and how the candles interact and close within the vicinity of a cross is the main trigger, with filtration via band distance, Individual slope trajectory of fast and slow MAs within the entry criteria.

Once in a trade active management takes over with small adjustments to an advanced ATR as the trade progresses to maximise each trade individually.

Spent almost 200 hours on it as each time frame needs to be researched across many Alts with different starting settings to build a library, and it already has positive expectancy.

English

As someone who’s transitioning over to systematic trading - this has been a fab listen…

Mike Bellafiore@MikeBellafiore

You’re staring at a P&L that looks like an EKG in a horror movie. We’ve all been there. It’s not just frustrating; it’s exhausting. 🛑 But here’s the cold truth: The "secret" isn't a magical indicator. The real edge lies in knowing which trades to skip. The Trading Floor: SMB Capital Podcast sat down with Dave Mabe, who’s been automating since 2005. He treats backtesting like a superpower—not because it predicts the future, but because it challenges his ego. If your backtest doesn't hurt your feelings and tell you you're wrong, you aren't doing it right. Stop hunting for the "perfect" entry. Start building a "Column Library" that filters for trading edge while casting a wide net. The market can reward systematic traders who trade like machines but remain curious like students. Your breakthrough just might be one rigorous backtest away. Let’s get to work. 📈 Executive Summary for Systematic Traders Core Objective: Shifting from "Guess and Check" loops to a robust, scalable optimization process that treats indicators as a library and backtesting as a source of truth. What you will learn: 1. The First Blanket Backtest: Why your initial test should "cast a wide net" with weak thresholds to generate the maximum amount of data for optimization. 2. Column Library Architecture: The power of building a reusable library of 300+ indicators/columns that can be applied across all future strategies. 3. Ownership of Edge: Why you cannot "borrow" confidence; you must do the work to understand the drawdown profile to survive live trading. 4. Strategic Collaboration: Treating networking as a trading skill and being a "default giver" to find synergies with other quants. Systematic Trader Notes: The Breakdown Subject: Heuristics of Systematic Strategy Optimization (Dave Mabe Case Study) I. The Thesis: The "Skipping" Alpha The Problem: Discretionary traders and hobbyists often seek the "perfect signal." This leads to overfitting and low trade counts. The Systematic Solution: Professional edge is often found in the optimization phase—identifying which subsets of a common signal (e.g., Opening Range Breakouts) are statistically inferior and "skipping" them. The "Ivy" Insight: In a zero-sum environment, your advantage isn't what you know; it's the mechanical discipline to avoid the negative expected value ($EV-$) trades that others take out of boredom or bias. II. Technical Framework: Casting the Wide Net Threshold Dilution: Instead of testing a 5% gap, test a 3% gap. This increases the N-count, providing more "surface area" for the optimization engine to identify meaningful correlations. Universe vs. Predictive Filters: * Universe Filters: "Fencing in" the tradable assets (volume, ATR, price). Predictive Filters: The specific indicators (yesterday's range, position in range) that actually generate the alpha. The Column Library: Treat trading code like a software library. A "bug" or "feature" found in one strategy should be able to optimize all other strategies in the portfolio simultaneously. III. Behavioral Finance & Heuristics The "Gun to the Head" Experiment: If forced to trade the opposite side of your favorite signal, how would you do it? This prevents confirmation bias and often uncovers powerful counter-trend strategies. The Partial Profit Trap: Scaling out for "psychological comfort" is mathematically inferior for the majority of trending strategies. Traders often trade off P&L for "feel-good" moments, destroying their long-term expectancy. Confidence Ownership: Confidence is the byproduct of the backtesting process. If you haven't built the strategy, you will abandon it during the inevitable first drawdown. IV. Key Takeaway for Discretionary Traders using Tech Quantifying Intuition: If you "feel" like Tesla is a good buy, find a way to measure that feeling as a column (indicator). If you can't measure it, you can't manage it. Backtesting as a Mirror: Use the data to challenge your "truisms." If the data shows a "dead" strategy still works, the market is signaling an inefficiency. Conclusion: Professional systematic trading is less about "being right" and more about being the most rigorous scientist in the room. Success is the inevitable result of a refined process applied to a massive library of data points. Your Trading Strategy Will Fail Until You Understand This ONE Process youtu.be/pPIPvyticq4?si… via @YouTube @davemabe @GarrettDrinon @smbcapital

English

List of Hyperliquid competitors (so far):

Lighter, Aster, EdgeX, Apex, Gains, GMX, Paradex, dYdX

Jupiter, Avantis.

Now Throw in Coinbase and Robinhood.

There's virtually no moat for Perps, and the UX is only improving across the board.

Where does this leave $HYPE?

English

ΞVLVΞ.hl 리트윗함

aVault - 2nd Batch Details & Schedule

We’re opening the second aVault batch this week and increasing the total TVL cap to $1M.

Access will be divided into two phases:

Phase 1 - Whitelist

This phase is only open to $SIRE holders who applied through the form we previously shared, with a $30k limit per wallet.

If you want to verify whether your wallet is eligible, please check the sheet shared in the comments and use Ctrl + F to search for the last 5 characters of the wallet you applied with.

Phase 1 will start at 8 PM UTC Dec 19, and will remain open for 6 hours, until 2 AM UTC Dec 20.

Please note:

Based on the amounts declared in the form we shared, Phase 1 is overallocated by ~30%, meaning not everyone on the whitelist will be able to join and allocations will be FCFS.

Phase 2 - Public

If the TVL is not fully filled during the whitelist phase, the public phase will start at 2 AM UTC and will remain open until the $1M TVL cap is reached.

If you have any questions, please reach out in our Telegram group or on Discord.

If you believe your wallet should be included on the whitelist but don’t see it in the sheet, please open a ticket on Discord.

English

@ashoswai @TulsiGabbard Hindus and Buddhists don't go on murderous rampages in the name of their god.

English

The tragic Islamist terror attack against those at a Hanukkah celebration in Australia sadly should not come as a surprise to anyone. This is the direct result of the massive influx of Islamists to Australia. Their goal is not only the Islamization of Australia but the entire world—including the United States. Islamists and Islamism is the greatest threat to the freedom, security, and prosperity of the United States and the entire world. It is probably too late for Europe—and maybe Australia. It is not too late for the United States of America. But it soon will be. Thankfully, President Trump has prioritized securing our borders and deporting known and suspected terrorists, and stopping mass, unvetted migration that puts Americans at risk.

English

Ggz. Seen this time and time again. Still like the product but they are gonna need HYPE like adoption to have any hope.

Almanak@almanak

Our team is still gathering all relevant data and will share a full report shortly. We appreciate your patience and fully understand how frustrating this situation has been for everyone.

English

ΞVLVΞ.hl 리트윗함

When I pointed out problems with Tarun's understanding of Hyperliquid, he challenged me to read the rest of his paper, suggesting I was too dumb to understand it.

I don't like obscurantism or gatekeeping. So I did what he asked. Here's what I think:

* The paper is wrong about what ADL is, even more fundamentally than what I pointed out yesterday.

* The paper proposes that exchanges should sometimes take on platform-level insolvency risk, which I think is not a good idea.

* And the core “ADL trilemma” is basically a restatement of its own assumptions, including an explicit assumption that insurance funds won't work.

🧵

Tarun Chitra@tarunchitra

@danrobinson You still didn’t read the theoretical results (skill issue?), are acting like an asshole and pretending you’re totally right without more than a little substance

English

Claim Delays, Wallet Deployment Issues & System Instability

Today’s airdrop claim event encountered two primary issues that affected the user experience: a delayed claim window and failures in wallet creation. Below is a clear breakdown of what happened, why it happened, how it impacted users, and what we’ve done to make sure no tokens were lost.

Issue 1: Claim Delay (12.15pm UTC → 12.35pm UTC)

The first issue was a manual operational error.

During the initial surge of activity, one of our engineers made a decision under pressure that unintentionally prevented us from enabling the claim function at the planned time. Out of caution - and to avoid activating claims in an uncertain state - we opted not to proceed until the situation was fully verified.

Impact:

Claiming was delayed by approximately 20 minutes.

Once enabled at 12.35pm UTC, many users were able to claim immediately without any further issues.

This was a straightforward mistake made in a high-stress moment. We’re implementing safeguards to prevent similar errors during future high-volume events.

Issue 2: Wallet Creation Failures

The second and more significant issue involved wallet deployment failures, impacting users who had not yet created an Almanak Wallet prior to the airdrop.

What happened:

DDoS Attack During Peak Load

Our infrastructure came under a heavy DDoS attack right as new wallets were being deployed. This disrupted backend services responsible for verifying wallet creation and processing state transitions.

Users With Existing Wallets Were Unaffected

Anyone who had already created an Almanak Wallet before the event was able to claim normally once claims were enabled.

~1,100 Users Experienced “PENDING” Wallets

For users creating a wallet during the attack, some deployments successfully broadcast on-chain but our backend was unable to confirm them due to network instability.

As a result, wallets remained stuck in a “PENDING” state.

In some cases, our systems did not register that the transaction had already been signed, leaving users unable to complete the process until we intervened.

For part of this affected group, generating a fresh wallet allowed the deployment to bypass the earlier disruption and proceed normally.

We’ve since cleared stuck states, restored the deployment pipeline, and mitigated the DDoS activity. Wallet creation and claiming are now functioning as expected.

Claim Success After Activation

Once the claim function was enabled and wallet creation stabilized, a large number of users were able to claim successfully right away. We are compiling complete metrics and will share a more detailed breakdown to give full visibility into how things unfolded.

Market Impact

The issues during the claim window had a clear and immediate effect on market sentiment. When users were unable to claim their tokens or create wallets reliably, uncertainty grew, and that uncertainty translated into short-term downward price pressure.

It’s important to emphasize that the market response was driven largely by access frustration and lack of clarity, not by any flaw in the underlying token economics or by any loss of user funds.

The Almanak team remains committed to continued communication, data transparency, and stable system performance that help guide the market back toward equilibrium as users complete their claims and regain trust in our product.

Summary

Our engineering team:

- Enabled claims once the system state was confirmed stable

- Mitigated the ongoing DDoS attack

- Scaled backend services to handle extreme load

- Unblocked wallets stuck in “PENDING”

- Validated the entire end-to-end claim and wallet creation process

All core functionality is now fully restored.

Your tokens were always safe.

No allocations were lost or compromised at any stage.

We appreciate everyone’s patience during a stressful and high-traffic launch. The challenges today highlighted both the incredible demand for the airdrop and areas where our infrastructure and processes must continue to improve. We’re already implementing fixes and safeguards to strengthen future high-volume events.

A more detailed data-rich follow-up will be shared in the upcoming days.

English

ΞVLVΞ.hl 리트윗함

KOLs + VCs tried to convinced you to sell your $BTC for $ZEC because it is "the new BTC." It's not. You became exit liquidity.

XMR is the only true privacy coinand blockchain privacy will be achieved thru smart contract networks like @chainlink or @RAILGUN_Project not thru separate and distinct privacy chains.

Tom Capital@Tom__Capital

$ZEC KOL distribution completed 🫡

English

This is not bullish as we head into the busiest shopping season of the year. Labor is going to tank harder in Q1 2026

*Walter Bloomberg@DeItaone

$AAPL - APPLE CUTS JOBS ACROSS ITS SALES ORGANIZATION IN RARE LAYOFF

English