Serenity@aleabitoreddit

I've initiated a position in $VLN ($155M MC).

This one is wild.

Valens is a AI semi for self-driving cars and robotics.

I've found that markets messed up on VLS from a ticker collision data error.

And missed new CES 2026 info this week.

VLN has:

1. $93.5M in Cash, 0 Debt.

2. ~$11M inventory

3. High gross margins ~69.1% (CIB/ProAV) margins, 43.2% automotive.

and projected to do $70M+ revenue with blended 63-65% gross margins, jumping from 43% from their automotive pivot from CES.

At $155M MC. What?

This just looked way too off at first glance, so I had to do more research, whether it was revenue collapse, dilution, cashflow problems, or regulatory risk.

What happened?

The mispricing was from an analyst/scanner typo regarding a $82M "inventory burn":

VLN is effectively a company with $93.5M Cash and Zero Debt for an EV of ~$65M, while the market has punished it for an "inventory crisis" that literally does not exist.

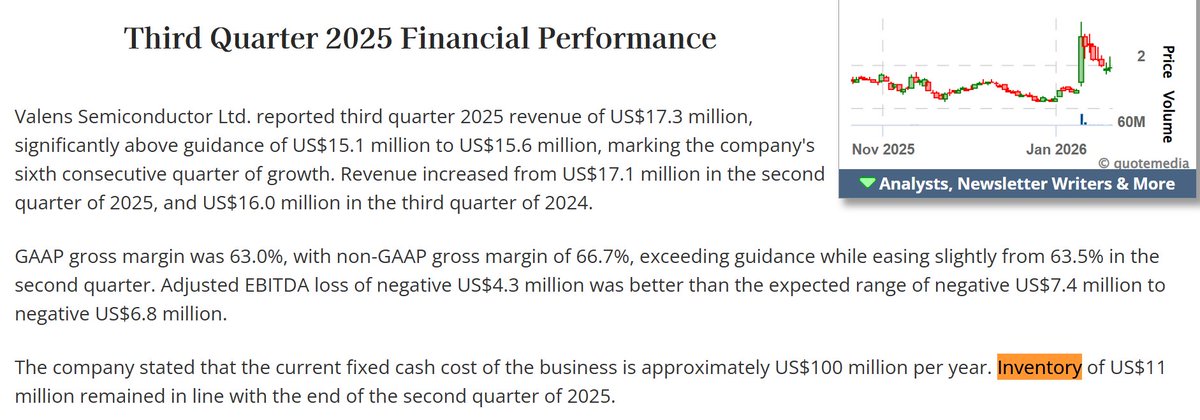

Streetwise's analysis + other scanners around Nov 13, 2025 typo'ed their report when they erroneously stated: "Inventory of US$82 million remained in line with the end of the second quarter".

The market and algorithms that scan for the reports thinks $VLN is sitting on >1 year of dead inventory ($82M) and burnt through their $93.5M cashpile on unsold chips.

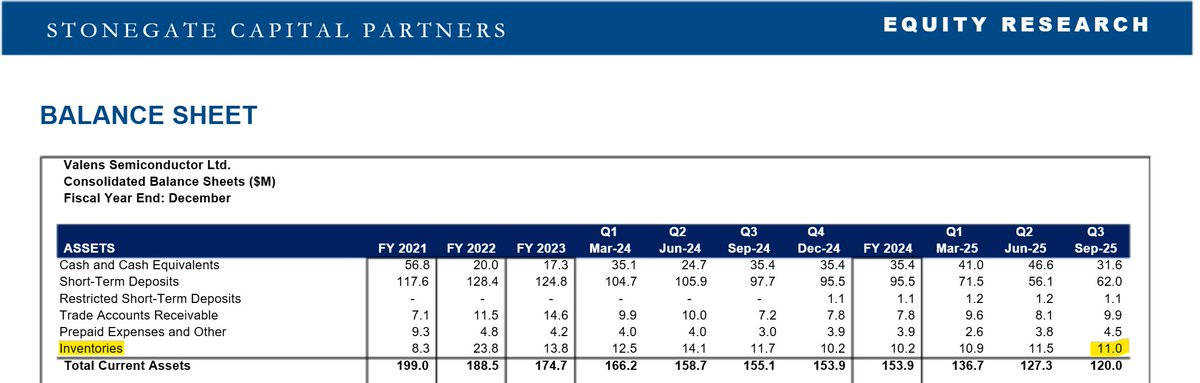

We can mathematically prove this is a typo using the company's official Q3 2025 balance sheet:

Total Assets: $136.7M

Cash: ~$93.5M

Remaining Room for Assets: $136.7M - $93.5M = $43.2M.

If inventory were actually $82M, Total Assets would have to be at least $175M ($93M cash + $82M inv). This inventory figure is mathematically impossible.

After looking at their financial reports, they are sitting on just ~2 months of inventory ($11M), only selling what they make.

The analyst + algorithms wrote spread the report confused Valens Semiconductor (VLN) with Velan Inc. (VLN.TO), a Canadian industrial valve manufacturer (with that inventory amount).

Even LLMs that read this, completely messed up and required manual review.

$VLN actually only has ~$11M in inventory as a fabless chip company and did not burn through $82M.

This looks like a genuine market inefficiency because you are looking at a clean balance sheet ($93M cash, $11M inventory, $0 debt) that has been artificially suppressed because of $82M cash burn fears on dead inventory due to the type.

_

Now, the secondary aspect is new CES information that came out.

$VLN spent years and millions on R&D for DSP engines for Mercedes, which presented single customer concentration risk for the automotive segment.

But from the CES release this week, they've effectively took the same that exact same engine, and managed to sell it to many hot verticals that have the exact same physics problem. They've also managed to scale their previous automotive segment with new T1 automotive OEMs.

But regarding their (VS6320 vs. VA7000) chipset, they are using the same Core IP (DSP).

Medical Chip: They took the same engine from the auto chip and stripped out the car-specific features to create a Extender for the medical segment .

And my favorite is the Machine Vision/Robotics vertical:

The new information is that with the RGo Robotics partnership they announced, RGo integrated Valens chips which allowed RGo to design robots where the cameras are far away from the brain without signal loss. And at CES they also announced one with CIS Corporation (a Japanese camera maker) for another specific robotics win.

They've effectively diversified their automotive segment into multiple other high growing + higher margin verticals for robotics computer vision to others.

Again, the alpha is that their new robotics segments announced at CES, operate on a 6-month sales cycle, not the 5-year automotive cycle. So revenue actually hits this year too.

Also, analysts were using blended automotive revenue (Mercedes, etc.) has lower gross margins (~42-45%).

The new growth coming in now (Robotics/Medical via VS6320) has significantly higher margins (VS6320 Gross Margin: ~69-70%), so the the blended gross margins will likely come in significantly higher than street consensus.

_

Now the downside?

Extremely heavy dilution at $11.5 Strike from warrants (which is 10X+ from here).

This will cap upside if it ever increases 1000% from $1.5 to $11.5

_

TLDR:

The market expected 2026 with high cash burn from inventory risk from a ticker collision typo. Instead, they are likely to get:

Revenue and earnings beat (driven by new verticals and much higher blended margins ~69%+ from new chip). As well as an $70M+ cashflow beat from the typo.

We could see $85-$92M revenue off 63-65% blended gross margins and that $82M+ in cash modeled back into this $155m company.

The algorithms are pricing $VLN as if it has <1 year of runway due to a phantom $82M inventory pile (off of a poison pill data point). So this is my own personal thesis from public information synthesis on why I entered this trade, NFI.

So while I don't expect this to be a $2B+ company, the current MC is just completely irrational pricing for a

$155M MC semi:

- with $93.5m in cash

- $11m in inventory,

- est. $80m+ revenue (growing 20%-30%+ Y/Y)

- with 60%+ gross blended margins.

Fabless semi companies with 60%+ gross margins typically trade at 4x–8x EV/Revenue and sector average valuations would be $493.5M, from $155m as a conservative base case.

Just slight "AI/Robotics" Premium, could value it at $653.5M with 7 E/V (~320%+)

TLDR: Found that this company likely got artificially suppressed because of a typo + ticker collision from false $82M inventory burn and is about to enter a newer higher margin + growth cycle from new verticals.

I am taking advantage of a database collision error.