Wall St Engine@wallstengine

$HOOD Q1’26 EARNINGS HIGHLIGHTS

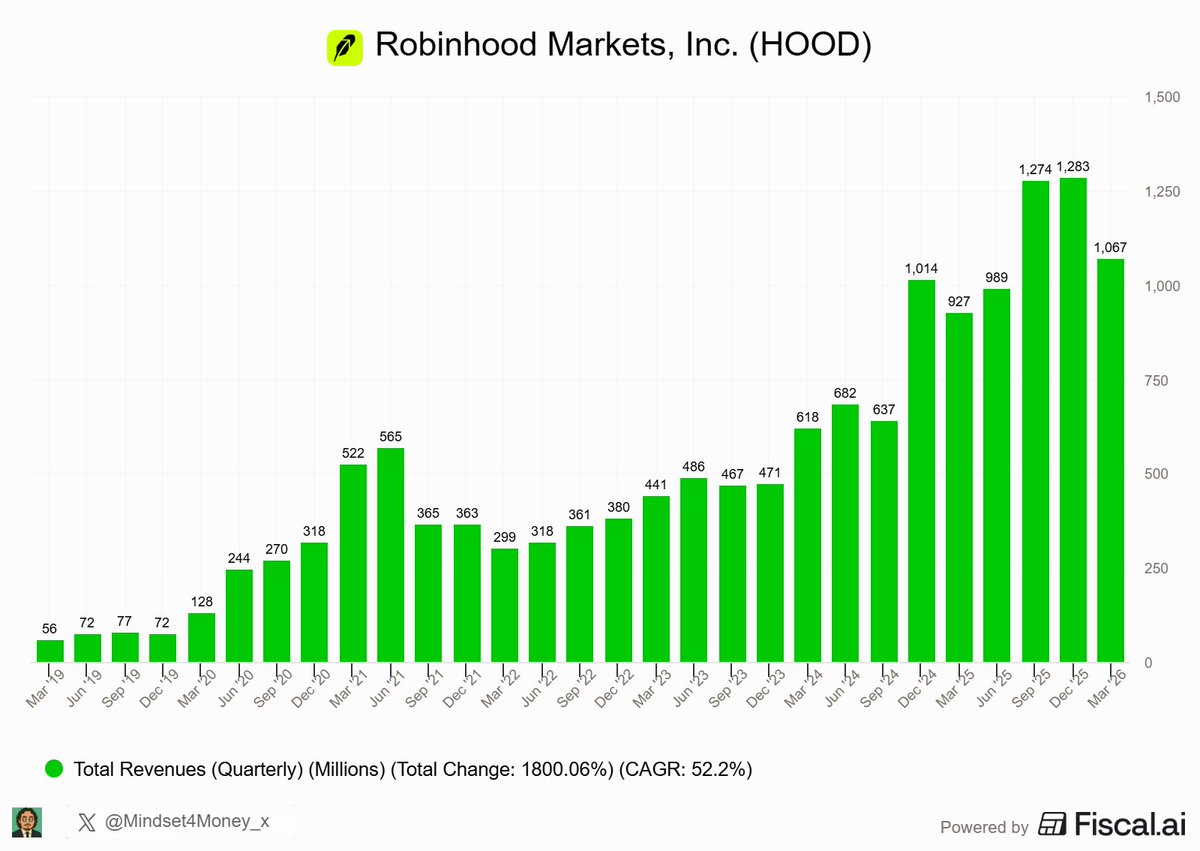

🔹 Revenue: $1.07B (Est. $1.17B) 🔴; +15% YoY

🔹 EPS: $0.38 (Est. $0.41) 🔴; +3% YoY

🔹 Net Deposits: $17.7B; 22% annualized growth rate

🔹 Gold Subscribers: 4.3M; +36% YoY

🔹 Total Platform Assets: $307B; +39% YoY

🔹 Funded Customers: 27.4M; +6% YoY

FY Guide:

🔹 Adj. Operating Expenses + SBC: $2.7B-$2.825B

🔹 Prior Adj. Operating Expenses + SBC Guide: $2.6B-$2.725B

🔹 Trump Accounts Investment: Additional $100M

Segment Performance:

🔹 Transaction-Based Revenue: $623M; +7% YoY

🔹 Options Revenue: $260M; +8% YoY

🔹 Equities Revenue: $82M; +46% YoY

🔹 Crypto Revenue: $134M; -47% YoY

🔹 Other Transaction Revenue: $147M; +320% YoY

🔹 Net Interest Revenue: $359M; +24% YoY

🔹 Other Revenue: $85M; +57% YoY

🔹 Robinhood Gold Subscription Revenue: $50M; +32% YoY

Other Metrics:

🔹 Investment Accounts: 29.1M; +8% YoY

🔹 ARPU: $157; +8% YoY

🔹 Robinhood Retirement AUC: $27.4B; +90% YoY

🔹 Margin Book: $17.0B; +93% YoY

🔹 Cash and Deposits: $16.7B; +71% YoY

🔹 Cash Sweep: $26.0B; -8% YoY

🔹 Equity Notional Trading Volumes: $638B; +54% YoY

🔹 Options Contracts Traded: 586M; +17% YoY

🔹 Crypto Notional Trading Volumes: $66B

🔹 Event Contracts Traded: Record 8.8B

🔹 Robinhood Banking: Over $2B in deposits from over 125,000 Funded Customers

🔹 Robinhood Strategies: Over 285,000 Funded Customers with over $1.6B AUM

🔹 Robinhood Gold Card: Over 800,000 Funded Customers

Financials:

🔹 Net Income: $346M; +3% YoY

🔹 Net Income Attributable To Robinhood: $350M; +4% YoY

🔹 Operating Expenses: $656M; +18% YoY

🔹 Adj. Operating Expenses + SBC: $607M; +14% YoY

🔹 Adj. EBITDA: $534M; +14% YoY

🔹 Cash and Cash Equivalents: $5.0B

Capital Return:

🔹 Buybacks: $250M, representing 3.1M shares at ~$81/share

🔹 Total Buybacks Since Q3’24: $1.2B, representing 25M shares at ~$46/share

🔹 Authorization: Refreshed to $1.5B, expected over next ~3 years

Commentary:

🔸 “Driven by our relentless product velocity and innovation, Robinhood is increasingly positioned at the center of our customers’ financial lives, just as we enter the early innings of the Great Wealth Transfer,”

🔸 “In Q1, customers remained engaged and rapidly adopted new products, leading to a 20 percent-plus annualized net deposit growth rate, double digit growth across equities and options, and record volumes for prediction markets, futures, and index options,”

🔸 “And Q2 is off to a good start in April, as equity and option trading volumes are on track to be the highest month of the year, and even with tax season, net deposits are approximately $5 billion month-to-date.”