창미니

97 posts

@BryzonX In Q3 2025, Comcast alone accounted for 43% of total revenue. A company with this concentration of revenue in a single customer is structurally vulnerable if Comcast ever slows spending, renegotiates terms, or shifts vendors.

English

창미니 리트윗함

$HLIT has become the exclusive operating system of choice for one of the most important network upgrades in the world with a 90%+ near monopoly

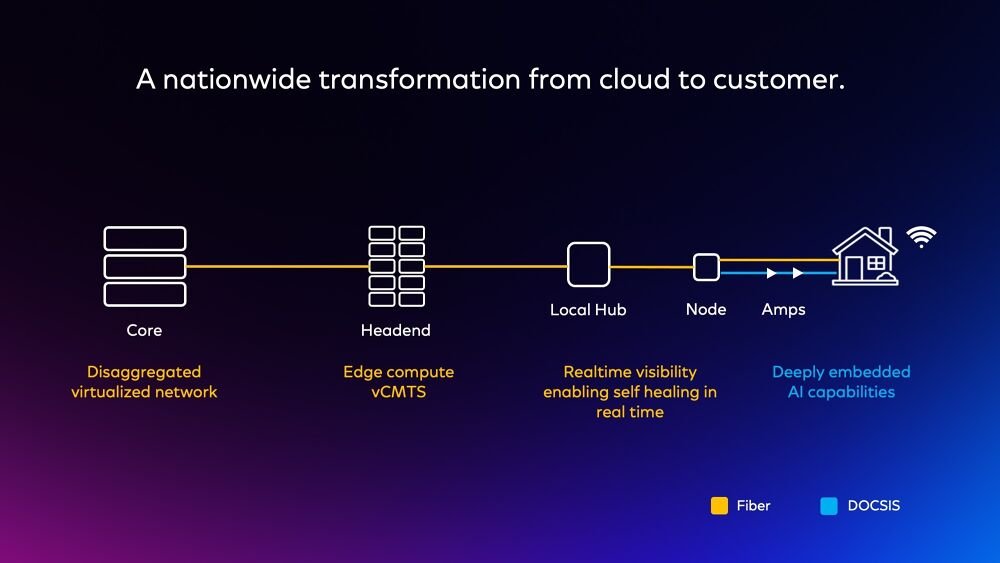

At GTC 2026 Comcast & Charter (The worlds largest broadband company’s) announced a major initiative to embed $NVDA GPU computing directly into their regional network infrastructure

These partnerships aim to move AI processing from distant, centralized data centers to the edge of the network, within milliseconds of customers

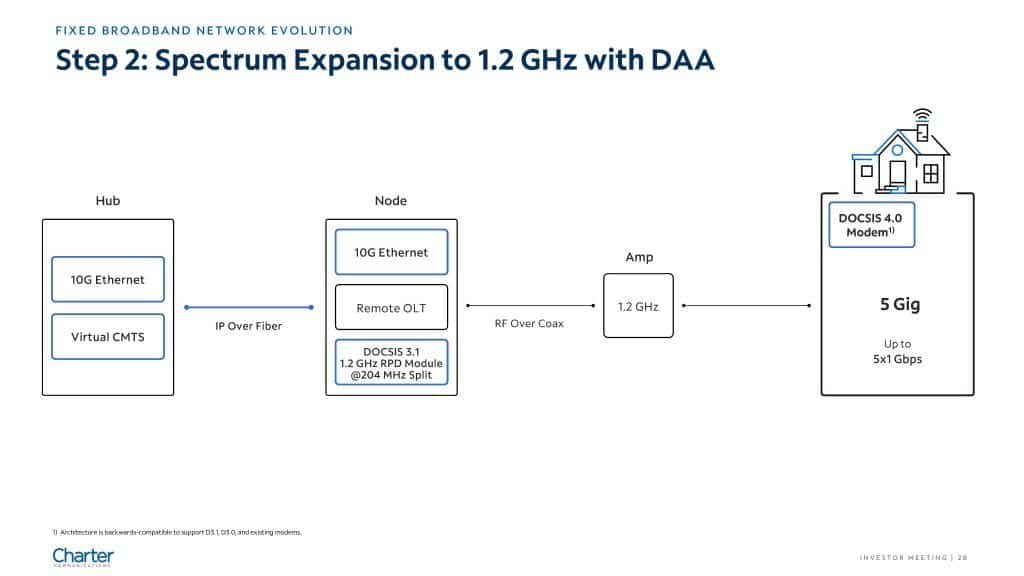

This means every single one of Comcast’s and Carters existing 240,000+ nodes across the US are currently being virtualized using $HLIT ‘s cOS

With Comcast stating:

“Comcast has built a highly distributed and localized network that brings AI based intelligence into neighborhood nodes... At the core of this strategy is our virtualized architecture, enabling an AI Native network that self heals and optimizes.”

They admitted that without this 100% virtualization, they could not support the NVIDIA Blackwell nodes or the massive symmetrical data loads required for 2026 AI standards

For agentic AI to work for local businesses, latency must be under 10ms. You only get that by putting the compute in the neighborhood, not in a data center three states away

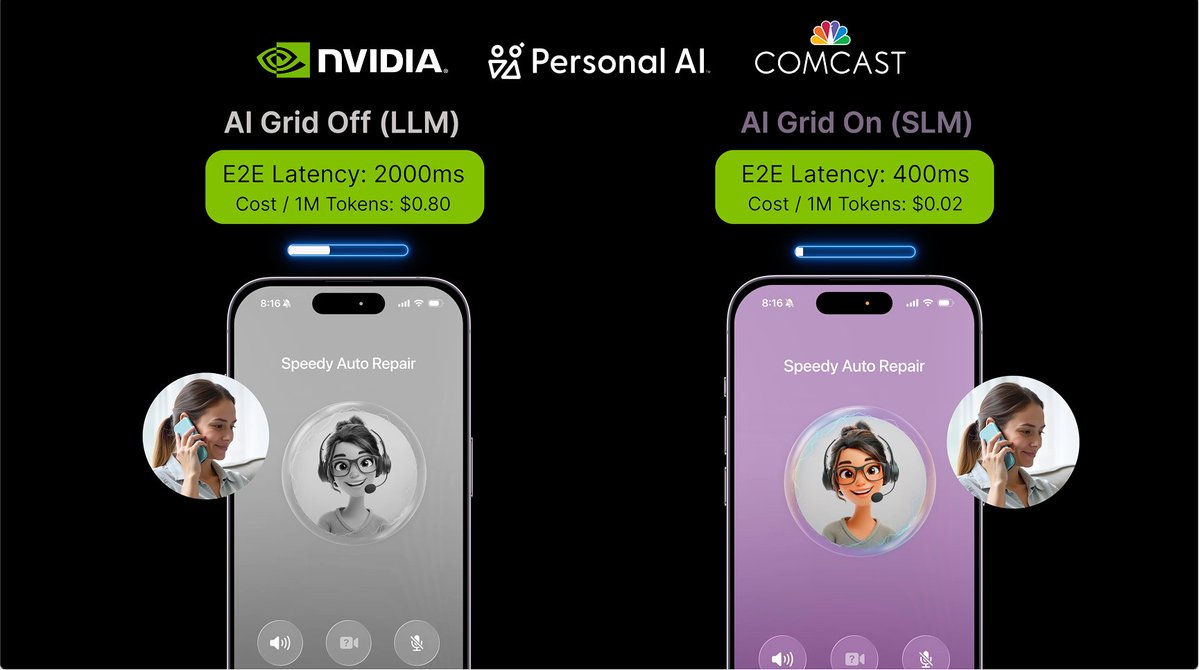

At GTC 26’ Comcast and NVIDIA released benchmarks showing that their distributed AI Grid powered by these Harmonic nodes cut AI costs by 76% compared to traditional data centers (this LOWERS token cost)

They stated that by running Harmonic software in every node, they have “effectively created the world’s largest Edge Compute Cloud”

Because Comcast, Charter and NVDIA are setting the standard, other companies across the world are following suit and starting to spend loads of CAPEX virtualizing their own existing networks

Last earnings call, they recorded a 3.5x book to bill ratio in their broadband segment

Meaning every $1 they bill, they are taking $3.5 in new orders

Rest of world revenue (rev other than Comcast & Charter) is growing 33% and accounts for 41% of Harmonics revenue with a fast growing backlog from 140+ broadband companies across Europe, Latin America, and Asia pacific making them a near global monopoly in vCMTS deployment

It’s 100% clear $NVDA is focused on moving aggressively into Broadband and Edge Infrastructure as they aim to allow ai to process as close to the user as possible

Harmonic $HLIT is the #1 enabler of the deployment of distributed network nodes in neighborhoods across the entire world with a sticky sticky business model

All 240,000 nodes act as "seats" for Harmonic’s software licenses. Every node upgraded represents a permanent, recurring revenue stream for the cOS platform

They are at the forefront of the standardization of the new internet.

English

창미니 리트윗함

창미니 리트윗함

Goldman warns semi meltup may be ending:

Semis (which in the midst of a well-publicized +50% ripper since early April) appear to be consolidating this morning, on combination of ARM -9% on sluggish smartphone royalty results (rallied +14% yesterday into numbers) + COHR -5% on softer gross margins than expected + Memory consolidation (Hynix & Samsung “just” flat in Korea overnight. SNDK / MU / STX / WDC all down -2 to -3% in pre).

English

창미니 리트윗함

Kevin Hassett: "The consumer is really, really firing on all cylinders…Credit card spending is through the roof. They're spending more on gasoline, but they're spending more on everything else too."

English

창미니 리트윗함

“글로벌 휴머노이드 군단이 온다”…‘STK 2026 로보테크쇼’ 6월 10일 개막 irobotnews.com/news/articleVi…

한국어

창미니 리트윗함

플리토는 '라이브 트랜스레이션'과 '챗 트랜스레이션' 교육기관 도입 건수가 전년 대비 350%, 전전년 대비 1200% 증가했다고 30일 밝혔다. 단순 통번역을 넘어 강의 전반을 데이터로 전환하고 체계적으로 관리하려는 교육기관의 전략적 수요가 본격화된 결과로 분석된다.

zdnet.co.kr/view/?no=20260…

한국어

창미니 리트윗함

Samsung's Semiconductor Speed Race... Samsung Brings Forward P5 Fab 2 Groundbreaking

Samsung Electronics will break ground in July on P5 Fab 2 (P6), the final production line at its Pyeongtaek semiconductor campus in Gyeonggi Province. The groundbreaking has been pulled forward by roughly six months from the originally scheduled early 2027 timeline. The move reflects a strategy to preemptively build out capacity in preparation for surging high-bandwidth memory (HBM) demand driven by the AI boom and a memory supercycle expected to extend beyond next year.

According to industry sources on the 7th, Samsung Electronics has finalized the July groundbreaking for P5 Fab 2 and has begun preparatory work, including site grading. The target operational date is 2029.

Samsung's all-out push to expand capacity stems from the fact that demand across memory — including HBM-led DRAM and NAND flash — is significantly outpacing expectations. Beyond merely responding to current demand, the move reflects an intent to cement market dominance throughout the multi-year AI semiconductor boom.

P5 Fab 2 will be built on a footprint measuring 662 meters by 194 meters. It is expected to have annual production capacity of 200,000 to 300,000 wafers on a 12-inch (300mm) wafer basis. As a single semiconductor fab, it is projected to have the largest production capacity in the world.

Samsung Goes All-In on Memory Capacity Expansion to Sustain the Supercycle — P5 Fab 2 Groundbreaking Pulled Forward by Six Months

Just a year ago, the clock had stopped at Samsung Electronics' 2.98-million-square-meter Pyeongtaek campus. As an unprecedented memory downturn drove Samsung's Device Solutions (DS) division to a 15 trillion won loss in 2023, construction on the existing P5 Fab 1 was halted entirely roughly eight months after groundbreaking. The vast site — equivalent to 16 soccer fields — turned into an empty lot, with cold winds blowing through where steel framing should have stood. It was a stark visual representation of the "semiconductor winter."

The dormant Pyeongtaek campus has been reignited by AI-driven tailwinds. Samsung Electronics, which announced a triumphant return with 57 trillion won in operating profit in Q1, has launched comprehensive capex investments in step with the HBM supply crunch and rising foundry demand.

◇ Simultaneous Buildout of P5 Fab 1 and Fab 2

Samsung Electronics will begin construction on P5 Fab 2, the final production line at its Pyeongtaek campus, in July. The schedule has been pulled forward by roughly six months from the originally planned early 2027 timeline. This construction will proceed in parallel with P5 Fab 1, which resumed late last year. Total investment across the two lines is estimated at 120 trillion won.

Samsung's accelerated timeline reflects the explosive demand from AI infrastructure expansion overwhelming supply, deepening the memory shortage. According to market research firm DRAMeXchange, the contract price for legacy PC DDR4 DRAM surged from $1.65 in April last year to $16 in April this year — a nearly tenfold jump in a single year.

P5 Fab 2, set to begin operations in 2029, will be built as a multi-fab capable of flexibly responding to market conditions. It will house everything from HBM and next-generation DRAM — Samsung's mainstay — to NAND flash and advanced-node foundry lines. Combined production capacity of P5 Fab 1 and Fab 2 will reach 600,000 wafers per month (on a 12-inch wafer basis). This is an overwhelming scale, comparable to Samsung's current total DRAM production (650,000 wafers per month).

Tectonic shifts in the foundry market are also seen as influencing Samsung's accelerated push. Big Tech firms such as Nvidia, Tesla, and Qualcomm — previously fully reliant on Taiwan's TSMC — have substantially strengthened their cooperation with Samsung Foundry to diversify their supply chains and disperse risk. Securing the production base to accommodate these customers has become a critical variable that will determine the outcome of future market share battles. An industry official said, "Once Samsung Electronics begins pumping out volume in earnest, it will be able to overwhelm competitors on cost competitiveness through economies of scale."

◇ Global Expansion Race in Full Swing

Competitors are mounting a fierce chase. SK Hynix plans to fill its new M15X fab in Cheongju, North Chungcheong Province, with 70,000 wafers/month of DRAM production equipment within this year. The opening of the Yongin cluster's first fab cleanroom has also been moved up by three months — from May to February next year. This site will become the core mass-production base for 6th-generation (1c) DRAM, which will form the foundation of next-generation 7th-generation HBM (HBM4E).

SK Hynix CFO Kim Woo-hyun stated on last month's Q1 earnings conference call, "This year's capex is expected to increase substantially year-on-year due to expanded future infrastructure investment."

US-based Micron has joined the race as well. Micron is building advanced memory fabs, including for HBM, in New York and Iowa. Including its Hiroshima, Japan fab expansion, Micron's production capacity is also expected to grow rapidly within two to three years. An industry official said, "Whereas past expansion races were simply chicken games to grab market share, the current battle is over who can complete infrastructure faster and prove their AI chip supply capability."

English

창미니 리트윗함

요약:

- 내러티브만 있는 개잡주로 어렵게 먹는 것보다, 숫자가 찍히는 우량주로 먹는 게 쉬운 장세

- 국장의 삼성전자, 하이닉스 모먼트가 크립토에서는 하이퍼리퀴드에서 나타날 것

-----------

1. 이번 AI 사이클에서는 게임의 메타가

코로나와 같이 실적이 없어도 기대감만으로 GME 같은 개잡주까지 폭등하는 Everything Rally가 아니라

실적이 숫자로 찍히는 놈들 위주로 어텐션이 몰리고, 실적 상향 조정과 수급 몰림이 겹쳐 가격이 순식간에 대폭등하는 패턴이 반복되고 있음.

때문에 국장 사례처럼 시총이 크다고 삼성전자/하이닉스를 버리고, 레버리지 개념으로 시총 작은 밸류 체인 내 중소형주로 갈아타는 전략이 오히려 언더퍼폼하는 중.

결과론적으로는 전닉에 레버리지나 미수/대출을 레이어링 하는 게 위험조정수익률이 훨씬 좋았음.

이건 크립토 시장에서도 나타났던 패턴인데, 비트코인이 바닥에서 몇 배씩 오르는 동안 알트코인이 언더퍼폼했던 것과 유사.

2. 요점은 코로나 때와 달리 수익률 때문에 내러티브에 의존하는 개잡주를 매수해서 어렵게 먹는 것보다,

숫자가 찍히는 우량주로 플레이하는 게 오를 확률도 높고, 시총이 높아도 수익률을 꽤 안겨준다는 것.

지금 열심히 개잡주 플레이하는 사람들도 메모리 오른 거 보고 묘한 박탈감(?)을 느낄 것임.

이런 현상을 고금리라 그렇다, 유동성이 부족해져서 그렇다는 설명이 있는데.

나는 그보다는 코로나(메타버스)나 닷컴(인터넷)과 달리 이번 AI 사이클에는 눈에 보이는 숫자와 실물이 있기 때문에

시장참여자들도 자연스레 이를 기준으로 투자하니 쏠림이 나타나는 것이라 봄.

3. 그리고 이건 제도권에 편입되면서 성숙하고 있는 크립토에도 똑같이 적용되리라 봄. 그 대상은 하이퍼리퀴드라 생각.(지극히 편향적)

현재 크립토 프로젝트 중에서 유의미하고 지속가능한 매출을 뽑아내고 있는 건 사실상 하이퍼리퀴드가 유일함. 나머지는 거의 내러티브 기반임.

하이퍼리퀴드의 가장 큰 약점은 무엇보다 높은 FDV인데, 수수료 97% 바이백을 고려해도 FDV가 높은 건 어쩔 수가 없음.

다만 오히려 이런 고시총 우려 때문에, 하이퍼리퀴드에 대한 센티멘트 대비 실제 홀더들의 포지셔닝은 온체인상 매우 저평가된 것으로 보임.

국장에서 개미들이 전닉 말고 코스닥 기웃거리다 전닉 상승 놓친 것과 유사한 조건이 갖춰지고 있다고 봄.

4. 특히 알트코인 투자자들은 25년 4분기 - 26년 1분기 큰 돈을 잃은 사람들이 많기 때문에

OO 배 이상 수익을 안겨줄 가능성이 낮다고 생각되는 고시총 종목에 관심을 두지 않고, 아직도 잡알트를 홀드하는 경향이 있는 것으로 보임.

상승하는 실적, 가벼운 포지셔닝은 시총이 무거워도 가격을 올릴 수 있는 조건임.

5. 때문에 26년 내 전략은 알트 순환매나 비트, 이더 선물이 아니라 하이퍼리퀴드와 이를 레버리지하는 전략으로 장기 홀드하는 것임.

나는 일부 알트코인과 밈코인이 폭발적으로 잠시 상승하며 개미들을 우량주에서 하차시키고

그들이 고점에 몰려있는 동안 우량주를 순식간에 쳐올리는 가속화 모먼트를 먹으려는 것.

6. 물론 잡알트 중에서도 10배 100배 짜리가 나올 것임.

그러나 나는 여기서 실수 한 번 더하면 한강행이기 때문에

라메잇 노인네처럼 루나에 전재산을 박을 수가 없어 아쉬움.

한국어

창미니 리트윗함

복수의 IB 업계 관계자들은 "원래 나스닥행을 타진하던 초대형 팹리스들이 최근 국내 유턴으로 가닥을 잡을 것 같다"며 "정부의 입김이 강하게 작용하면서 국내 기업 입장에서 정책 당국의 눈치를 보지 않을 수 없는 상황"이라고 입을 모았다. m.thebell.co.kr/m/newsview.asp…

한국어

Current favourite CPO plays:

- $AAOI for vertical laser + full engine integration (earnings today should be fun)

- $SIVE for premium CW DFB arrays

- $LITE for nvidia’s CPO programs + they dominate CW/EML laser arrays (yet to properly digest earnings tbh)

Also really really like $AVGO as a boring compounder:

- since they're already shipping cpo switches

- integrated directly with $TSM COUPE platform

- probably capture highest margins if CPO hits the penetration that Goldman fcst (ASIC + optical engine combo

Bobby Axelrod@BobbyAx99479964

@ParadisLabs Thanks for you posts there are so educational for someone starting out like me 🙏🏾. What would you say are your top 3 CPO plays that would benefit the most if this GS CPO forecast plays out?

English

I'm still laughing how much Swedish hate their own frontier companies so much.

That they write hit pieces every day on $SIVE.

This one was entertaining: Local journalists show up to an empty $SIVE administrative building uninvited.

Because they can't fathom the CEO is in Silicon Valley or design team is working on US Gov CHIPS act dev in the US. And because there weren't many cars parked outside + CFO wouldn't take questions about secretive hyperscaler deal financials.

They wrote a random negative hit piece.

By repeating "There are several who make lasers like these and Sivers are far from alone".

Several like $LITE, $COHR, $60B+ companies.

and reported earlier that "CPO is nothing special, it's been around for years."

While GS projects CPO going from $1B -> $91B TAM over the next two years.

Even put "Plans" in quotation marks because they didn't think Sivers is supplying lasers to $JBL 1.6T LRO.

IMO, $SIVE ends up as a $10B+ company next year, especially if they follow what $LITE / $COHR did with downstream IP integration to capture more of CPO module BOM.

Just don't think Swedish people understand hyperscaler supply chains, concept of forward growth, or the fact that employee count doesn't equate to revenue.

Transfer of control from local Swedish -> West is always appreciated, as this was a majority owned local retail company before.

English

창미니 리트윗함

제조업의 끝판왕은 로봇 + AI 스마트팩토리

반도체 관련으로 이미 시행중인 기업들이 있는데, 기술력을 잘 선별해서 투자해야할 듯

news.samsung.com/kr/%EC%82%BC%E…

한국어