DVD@deepvaluedude

$ASTS

There’s a couple things that I find hilarious when reading the bears spewing AI slop.

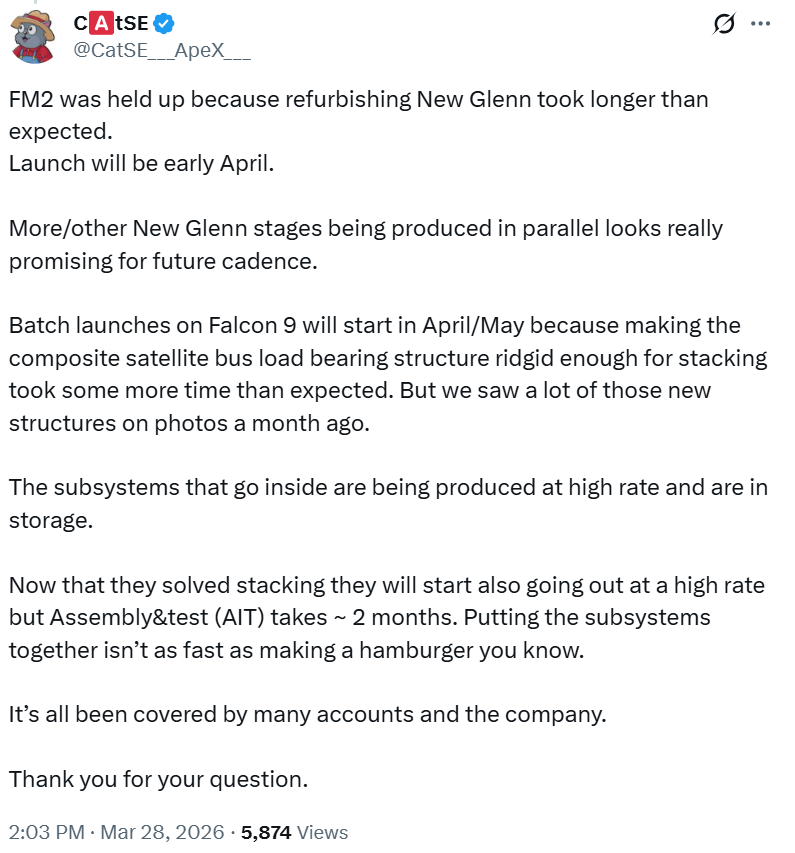

First, they continue to talk delays, manufacturing issues, stacking problems, and other bullshit. These are people that have never built anything in their life or beared the responsibility of running a company that has the opportunity to change the world. These “technical” problems are transitory, which means it’s a matter when, not if. Management isn’t stupid, they are aware of the hurdles well before they run into them and they’ve been expecting delays, but it’s Wall Street and they also know they have to manage their stock, raise capital, and effectively buy runway in a macro environment that may not allow them to do so in the near future. That’s prudent management. If you think otherwise, you’re likely a retail retard or a paid consultant, both of which fall in the same bucket in my eyes.

Second, bear’s assume the business model won’t work because satellite signal can’t penetrate walls. Who the fuck cares? Does it work under foliage, and outside in general? If the answer is yes, that’s good enough to allow MNOs to save (in aggregate) $10s of Billions, and pay AST a couple of billion to maintain an NTN that allows them to compete against SpaceX, reduce churn, and reinvest in sales and marketing to take market share. That’s just the conservative commercial angle (as an MNO cost center), and not including the global military/ intelligence and DoW use case that will alone generate $1-$2B of revenue. Paths to multi-billion in revenue requires mediocre execution and better than average technology. This supports a $50-$75B valuation. What’s the upside? The tech and execution works like management claims. This is where valuations like $1T get thrown around.

Do I care if the stock drops to $50? No. Will I be buying more? No. Because I already own so much, and it’ll still be a multi-bagger. Will I be concerned? No. Amazon, google, Apple, and every other revolutionary company has experienced 90% drops, but where did they end up? Remember, paid consultants aren’t meant to be visionaries. They are expected to be historians, which means if it hasn’t happened yet, they heavily discount the opportunity, and assign failure value to delays. Abel is a visionary. Which means he’s optimizing for effectiveness and long-term impact. See the opportunity. The opportunity cost of not being long is much greater than the potential of 0.

In my world, this is asymmetry.