The Joker

119 posts

@zerohedge 5Y break even inflation > 10Y break even inflation meaning - expecting near term shocks such as supply chain disruptions, higher rates, growth pessimism

English

@HayekAndKeynes Unfortunately it's far from being done. Everyone has already lost. Everyone is stubborn, and everyone doesn't see far from their forefinger. Sad.

English

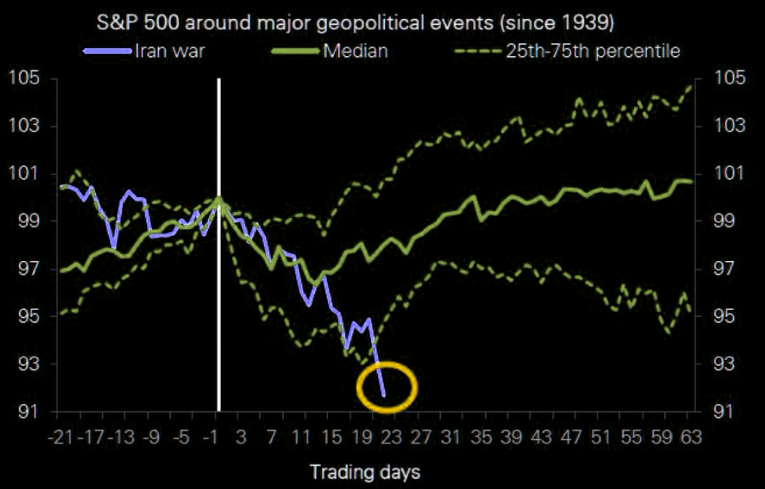

Inching closer to a finale - either a nice peace deal or bomb and bounce. Either way this looks more and more like the prelude to Mission Accomplished.

English

Some of the highest quality businesses in the world are trading at extremely cheap prices. Ignore the MSM. One of the most one-sided wars in history that will end well for the U.S. and the world. And we have the potential for a large peace dividend.

One of the best times in a long time to buy quality.

Ignore the bears.

English

@themarketear It is a potent mix of headwinds - elevated oil prices, private credit stress, technicals.

English

Various folks on Twitter

Perma Bulls max long at the top still buying every dip with made up cash

Price followers max long at the top. Stopped out longs and shorted 6700 and now max short and expecting oil to melt up and stocks to melt down

Perma Bears. "I told you so" "Its over" Max Short again for the millionth time despite constant drawdowns

Actual alpha investors

Raised cash in Q4 and Q1 and now doing okay. Thesis is playing out but jeez. Perhaps scale back in a little if we dip scale in more if we crash or chill if we don't.

English

@thisisatest0007 @dampedspring ROW is usually not owned with ROW capital. Before you go there check twice who owns that index. That's the one who moves that market - what's their narrative? Not that nation, not ROW.

English

@dampedspring How would you include the post conflict dollar decline in your portfolio? ROW equities? ROW bonds? Basket of currencies?

English

Note sent to clients. Overall macro synthesis and update based on war related conditions impact and pricing. What we are doing about it is for clients only.

Based on all things happening in the world my macro view is mostly unchanged since writing the "A Hamburger Today"DSR 11/17/26 (available in comments) The major themes remain in place

1. There is a tremendous overhang of issuance in IPO markets, corporate debt markets, and government deficit funding markets. Share repurchases demand is falling.

2. Asset prices particularly bond steepness and risk premium are inadequate to generate the sort of returns to have commercial banks create money which means all issuance mentioned above will compete with existing private sector assets to create the necessary credit without banks creating money.

3. At the same time as supply of assets is increasing without money creation consumers are NOT seeing wage growth anymore to continue to spend and have maintained consumption at elevated levels by dissaving. That dissaving adds to the supply that those with cash can choose from to buy

4. Spending on AI despite its increasingly optimistic outlook for future impact is no longer being tolerated by investors who are asking when those spending on chips and data centers will generate return from those spending on AI models. Those spending on AI models (real disrupted businesses and real consumers) have yet to cut jobs much

Prior to the war that led us to the idea that assets in general had to reprice cheaper (risk premium expansion) that has been playing out lately but seems less to do with the above and more to do with the war but it's likely that under the hood the damage of the above has begun to seep into markets and the economy.

Prior to the war the RISK to my thesis was

1. Significant sustained reversal on tariffs which would be pro growth and favor equities over bonds

2. AI both generating ROI AND not hitting jobs much

3. QRA and FED manipulation to depress risk premiums

4. Much more rate cuts done by a Trump controlled fed

5. While I couldn't see how Congress could do fiscal stimulus particularly post scotus tariff revenue hit another debt busting tax cut could make me wrong

What's changed since the war.

1. Consumption is further challenged by likely elevated energy prices for the next year AND by negative wealth effect which discourages dissaving

2. Ignoring what CB's will do markets have increased short term rates which is a tightening

3. Central banks have broadly and by bank pivoted from dovish to pause or pause to hike (hawkish pivot) sensibly waiting to see the real slowdown while obviously immediately seeing the inflation spike

4. More issuance and asset selling due to the literal waste of setting money on fire due to war has been piled on the already massive pile of asset overhang

5. Despite all manner of negative growth shocks I saw and now see even more bond yields have risen and risk premiums have expanded which is an almost certain to guarantee a marked real slowdown.

6. The mechanics of a dollar squeeze are clear to most and dollar has bounced and ROW assets are being puked after a massive move BUT the conditions for the dollar have perhaps NEVER been worse and the secular get out trade is once again supported by cheaper risk parity in ROW which if and when hostilities tame will snap back with a vengeance.

Given my synthesis, now we look to what's priced in.

Risk premiums are medium wider but not wide. Adjacent to risk premium markets like asset vols, correlations, swap spreads and credit spreads are medium wider but NOT wide

From a pure synthesis of all these things long term treasuries are still NOT cheap enough to be max levered long in both alpha and beta BUT they are far more interesting than equities. My synthesis above is clearly STILL bearish growth, margins, and equities. The above is bearish all but cash but most bearish equities. It is also extremely bearish USD and by definition somewhat bullish gold.

English

@dampedspring Andy if banks aren't creating new money, and if the money supply is fixed, the only way to fund new debt without a crash is for the same dollar to change hands much faster (velocity up). Is that realistic within this environment? And why FED as a last resort won't step up?

English

@SwiftMacro @grok @zerohedge That is a fair scenario, but I would say - it makes sense if we don't have a systemic event. Even we don't, it's hard to me to see catalysts to fuel SPX upward. With oil prices, and MOVE at these levels it's hard for me to be positive at least one more week. Technicals are nuts.

English

Those are real pressures, but they are symptoms, not drivers.

Oil spikes and private credit stress both trace back to liquidity tightening into a late cycle.

When liquidity stabilizes, those pressures tend to ease, not compound.

That is why this looks like a transition, not a breakdown.

English

"We Ran The Numbers": Goldman Trading Desk Warns "What Happens Next Isn't Encouraging" zerohedge.com/markets/we-ran…

English

@SwiftMacro @grok @zerohedge Two strong forces have been pushing SPX downward - elevated oil prices & private credit. On the top of that technicals look red for a little bit more.

English

@grok @zerohedge This is what a handoff looks like.

Mega-cap leadership fades, liquidity stabilizes, and capital starts looking for its next destination.

That is not bearish. That is rotation.

The next cycle starts where attention is not.

English

@dampedspring MOVE is suggesting a potential credit stress event - I think this is a majority portion of the current weighted average downside equation. The oil prices shock is the rest.

English

I'm in the midst of covering all of my equity shorts and going long. But jeez just checked SPX NTM Bloomberg consensus earning of 334 vs 277 trailing or 20.6% expected earnings growth. Honestly is there a legitimate case for earnings beat vs expectations

English

@dampedspring Andy, check the differences in 5Y 50 EMA for the Spoos index vs spy, and again vs their current prices. Different pic.

English

Context. This was 1. But market today has yet to truly correct.

Andy Constan@dampedspring

On 8/2/90 Iraq invaded Kuwait. The SPX which was already dealing with a recession fell 18%. On 1/9/91 the world was panicked about a U.S. attack. James Baker said "Regrettably" and the most famous sell the rumor buy the fact trade of my lifetime occurred No one on Twitter knows a thing

English

What's the most bullish scenario for stocks in order

1. Overwhelming attack

2. Escalation attack not overwhelming

3. Ceasefire

English

@dampedspring Mechanics:

We're still in elevated TACO mode

Sending ground troops = markets price the state of potential oil supply control = downward pressure on oil = immediate tailwinds for stocks

That scenario will just postpone the inevitable spike in oil prices again

English

@PaulKrueger_ @zerohedge Tactical allocation - meaning timing-based within the investment management world

English

JPMorgan Traders Close Highly Profitable 'Tactical Bearish' Trade zerohedge.com/markets/jpmorg…

English

@GaryStoneSWS If you claim something like this - why don't you trade for yourself and make $bn? Why do you go online and do these things?

English

Screw it.

I'm giving away the latest version of the mechanical trading system we've spent 30 years refining.

The same system that trained over 2,000 traders.

No fee until you've seen results.

Like this post + Comment "ACCESS" and I will DM you.

(Must follow, 24 hours only)

English

@SpecialSitsNews Gold (selling & mining) depends on oil and gas. Among others. Within the importance scale structure, Oil is above Gold, that's why the biggest energy shock pressures Gold prices right now

English

Markets Just Cracked. The Follow-Through Is What Matters Now.

zerohedge.com/the-market-ear…

English

@nntaleb This is the starting 5 for the world's dream team

Noam Chomsky,

John Mearsheimer,

Jeffrey Sachs,

Novak Djokovic,

Gregg Popovich,

Bench:

Nassim

Stan Druckenmiller

Howard Marks

Bob Dylan

Leonard Cohen *

You're setting tough tasks - hypocrisy in the world is the highest ever

English

Now I am curious: which well-known people (currently alive) you think are close to 0.

Nassim Nicholas Taleb@nntaleb

On a bullshit scale of 0-10, where 0 is maximally rigorous and 10 is maximally bullshitter, Sam Harris stands close to 10.

English