Rob!n

4.6K posts

Rob!n

@ro_rademaker

Technology focused investor ~ Ideas not financial advice ~ Put in the work ~ Ask the right questions

Belgium 가입일 Temmuz 2022

672 팔로잉329 팔로워

@MikeLongTerm Yeah, it's ridiculous, Intel trading like all problems will be solved soon

English

$AMD would be $4,500-$11,000 at $INTC PEG Ratio 😲

At Intel's PEG ratio (9-19), AMD's implied share price would be dramatically higher roughly $4,500 to $11,000+ per share

Not Financial Advice! Just some perspective how cheap $AMD is!

Mike@MikeLongTerm

How $AMD is worth $1,200-$1,470| Fair Value🧵 $AMD $NVDA $AVGO $INTC $TSM PEG Ratio COMP Not Financial Advice! When we talk about PEG Ratio, we typically refer to Forward, using forward P/E to measure it. While many are mistaking TTM PEG Ratio. I prefer Forward PEG as they measure earning power for its growth potential. Hence we have expensive stocks like $KO $COST $WMT where boomers overpay. I will link all threads below if you are interested to understand the full picture. Also, many are excluding @AMD Revenue & Earning from @OpenAI and $META 12GW or 2GW in H2 2026 and many other customers like $MSFT $AMZN $GOOGL $ORCL LumaAI G42 and many more AI natives on Forward P/E and P/S. I dont know why they are deleting $50B+ revenue and EPS. Many months ago, bears would say OpenAI has no money, and $META can't finance it. But here are the facts: ~@OpenAI now has $170-$200B Cash after the most recent $122B funding round with potential $50-$70B more going IPO later this year. So yea the "OpenAI Has no money" bear case is nonsense. ~ $META TTM Operating Cash Flow is $83.2B and it is extremely profitable business where AI is proven to increase Ads growth and profit. META also has $81.59 billion USD in cash and cash equivalents Ok now back to PEG Ratio Comp (Forward). Share price is right now, so it can fluctuate when people see this post. Doing FY2026. Fwd P/E is Non-GAAP. PEG less than 1= Super Undervalued for its growth Around 1 = Fair value More than 1= Expensive $AMD: $332/share or $542B Market Cap Forward P/E 22-27x. Revenue growth FY2026 100%+ PEG Ratio= [(22+27)/2]/100= 0.24 1.0 PEG Ratio would be $1,200-$1,470 $NVDA: $210/share or $5.1 Trillion Market Cap Foward P/E 25-28x. Revenue growth FY2026 65% PEG Ratio= [(25+28)/2]/65= 0.40 1.0 PEG Ratio would be $533-$542 a share $AVGO: $398/share or $1.89 Trillion Market Cap Forward P/E 28-36x. Revenue growth FY2026 40% PEG Ratio= [(28+36)/2]/40=0.8 1.0 PEG Ratio would be $450-$460 a share $INTC: $93/share or $468B Market Cap Foward P/E 120-150x. Intel is a bit special as Revenue growth is 7-15%(wide range) ~At 7% | PEG Ratio= [(120+150)/2]/7= 19.2 ~At 15%| PEG Ratio= [(120+150)/2]/15=9 $TSM: $394/share or $1.83 Trillion Market Cap Foward P/E 22-26x. Revenue growth FY2026 40% PEG Ratio= [(22+26)/2]/40=0.6 1.0 PEG Ratio would be $600-$632 a share While AMD has mutiple upgrades this week toward closer to $500, but it is still significantly behind for its fair valuation or potential. Granted FY2026 has an easier comp to FY2025, but Agentic AI is pushing EPYC Venice demand to 15-20m units. And $TSM is ramping up 2nm CoWoS capacity where AMD is 2nd largest customer after $AAPL. AMD has the supply and demand unlike 2023-2024. Under Dr. Lisa Su’s visionary leadership, AMD has engineered one of the most dramatic value-creation stories in semiconductor history delivering a forward PEG ratio that has collapsed to an astonishing 0.24 while the company stands on the cusp of explosive, multi-year growth in the emerging Agentic AI era. Dr. Su’s full-stack strategy uniting cutting edge Instinct GPUs, MI-series accelerators, and next-generation EPYC processors has transformed AMD from a distant challenger into the only credible alternative to NVIDIA with true hyperscaler-scale deployments already live at OpenAI, Meta, Microsoft, and others. This execution has not only crushed gross margins and delivered consistent revenue beats but has also produced a valuation disconnect that the market has yet to price in: at a PEG of just 0.24, AMD is trading at a fraction of its intrinsic growth rate, even as consensus models still undercount the coming CPU demand surge. The Agentic AI wave fundamentally resets the CPU:GPU workload ratio. Where today’s training clusters run at 1:4 to 1:8, tomorrow’s autonomous agents will flip the script demanding 3–5 CPUs per GPU for real-time reasoning, orchestration, memory management, and low-latency inference. With global CPU capacity already tightening and hyperscalers scrambling for EPYC Venice and its successors, AMD is uniquely positioned to capture this structural shortage. The result: consensus FY2026 revenue of $77–94B and EPS of $12–14.70 represent conservative baselines, not ceilings. Compounding this tailwind is the Helios Rack the industry’s most efficient AI-optimized platform. It delivers the lowest TDP, the lowest TCO, and the lowest $/M-token cost of any rack-scale solution on the market today. By slashing power draw and inference economics at scale, Helios doesn’t just win on performance it wins on the two metrics that actually matter to hyperscalers’ P&L: energy bills and token profitability. When every million tokens generated directly hits the bottom line, the lowest-cost rack wins the cluster and AMD is already winning it. Dr. Su didn’t just navigate AMD through near-death; she positioned it at the exact intersection of the two biggest secular forces in tech: the insatiable appetite for AI compute and the physics limited supply of efficient CPUs and accelerators. With a PEG of 0.24 and a clear runway to $1,000+ per share as the Agentic AI flywheel accelerates. The data is clear. The leadership is proven. The future is already being rack-deployed. AMD isn’t just cheap, it is the single highest-conviction AI infrastructure play for the next decade for all Hyperscalers and AI Natives! I'm a firm believer that Price action will follow Fundamental eventually. Not Financial Advice!

English

Collaboration with Exostellar (announced/expanding in early 2026) is QCOM's direct play for the AI Data Center market

By integrating Exostellar’s expertise in data center scale orchestration and virtualization, QCOM aims to provide a full-stack solution

$QCOM

Rob!n@ro_rademaker

Although there is no official announcement yet? @Qualcomm $QCOM confirmed this by replying: Welcome to #TeamQualcomm, Exostellar. 👏

English

Rob!n 리트윗함

Magnificent 7' earnings rush reveals AI spending surge, with hyperscaler capex set to reach $725 billion in 2026

finance.yahoo.com/markets/articl…

English

Rob!n 리트윗함

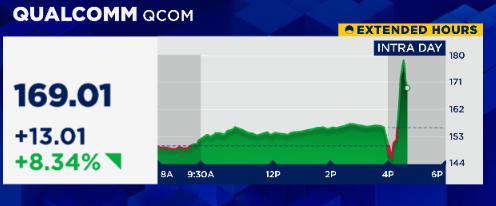

$QCOM swung from -7% to +14% in after-hours after CEO Amon called Q3 the bottom for Chinese handset revenues and said the company will begin shipping to a large hyperscaler data center customer this calendar year — earlier than the fiscal 2027 timeline previously guided.

English

Leading Hyperscaler Custom Silicon Engagement 🤓

Rob!n@ro_rademaker

$QCOM 👀 up big in premarket

English

$QCOM expectations were modest this week quarter and it delivered.

I stand by my assessment that what will move the needle for the company will be its data center entry with a portfolio of XPU, CPU, Custom, and Networking chips.

The sooner it can confirm customers and ship product the more sentiment may change in its favor.

TrendSpider@TrendSpider

$QCOM Down on a Double Beat EPS: $2.65 vs $2.56 est REV: $10.599B vs $10.593B est 🟥 -3.36%

English

Rob!n 리트윗함

$QCOM Q2 FY26 EARNINGS HIGHLIGHTS

🔹 Revenue: $10.60B (Est. $10.56B) 🟢

🔹 Adj. EPS: $2.65 (Est. $2.55) 🟢

🔹 QCT Automotive: $1.33B; +38% y/y

🔹 QCT Automotive + IoT: +20% y/y

🔹 New Buyback Authorization: $20B

Q3 Guide:

🔹 Revenue: $9.2B-$10.0B (Est. $10.26B) 🔴

🔹 Adj. EPS: $2.10-$2.30 (Est. $2.43) 🔴

🔹 QCT Revenue: $7.9B-$8.5B

🔹 QTL Revenue: $1.15B-$1.35B

Segment Performance:

🔹 QCT Revenue: $9.08B; -4% y/y

🔹 Handsets Revenue: $6.02B; -13% y/y

🔹 Automotive Revenue: $1.33B; +38% y/y

🔹 IoT Revenue: $1.73B; +9% y/y

🔹 QTL Revenue: $1.38B; +5% y/y

Capital Return:

🔹 Q2 Capital Return: $3.7B

🔹 Buybacks: $2.8B through 19M shares

🔹 Dividends: $945M, or $0.89/share

🔹 1H FY26 Buybacks: $5.4B

🔹 New Authorization: $20B

Commentary:

🔸 “We are pleased to deliver results in line with our guidance, reflecting solid execution as we navigate a challenging memory environment.”

🔸 “We are in a period of profound industry transformation — the rise of AI agents is reshaping our roadmap across every platform we develop.”

🔸 “We are equally excited by our entry into the data center, where a leading hyperscaler custom silicon engagement is on track for initial shipments later this calendar year.”

English

Rob!n 리트윗함

Rob!n 리트윗함

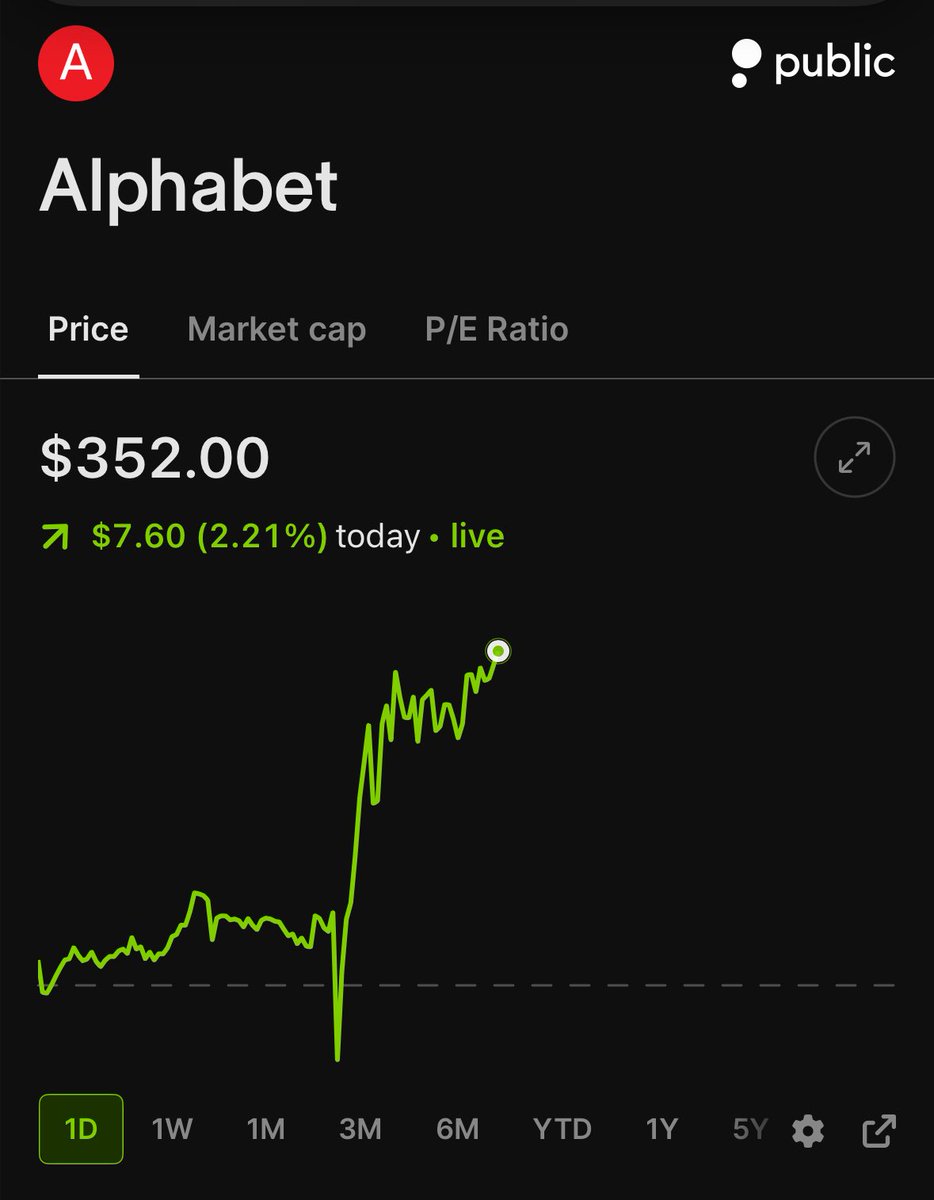

$GOOGL earnings:

- Google Cloud up 63% YoY! (backlog now $460 billion)

- $GOOGL Search far from dead up 19% YoY (wow)

English

@ondrejslunecko I stopped caring about what she is doing, it is not our style of investing, in, out, in out..

Haven't found a lot of value in what she is vocal about, except Tesla and Bitcoin, bjt could have figured that out without them

English

Rob!n 리트윗함

You can now ask Gemini to create Docs, Sheets, Slides, PDFs, and more directly in your chat. No more copying, pasting, or reformatting, just prompt and download.

Available globally for all @GeminiApp users.

English

Rob!n 리트윗함

$SNAP and $QCOM signed a multi-year deal to power future Specs eyewear with Snapdragon XR chips.

Snap says the standalone AR glasses launch later this year with a focus on on-device AI, graphics and shared experiences.

English

Rob!n 리트윗함

Rob!n 리트윗함

Oh hey I guess my $QCOM investment isn't dead money after all! Possible OpenAI smartphone supplier within the next couple of years.

English