Sabitlenmiş Tweet

D

5.2K posts

D retweetledi

Professor Jiang Xueqin on how this war is likely to go and what happens to the world.

(0:00) How Will the Iran War Be Resolved?

(7:33) The 3 Major Trends We Will See Due to This War

(11:28) Will Japan Become a Nuclear-Armed Power?

(16:06) The Future of South Korea

(20:12) The Energy Crisis

(25:23) The Future of the GCC and Iran

(29:57) The Greater Israel Project

(35:11) How US Ground Troops Will Change the War

(36:46) Prof. Xueqin’s Advice to Donald Trump

(38:49) Is It Possible for the US to Get Israel Under Control?

(45:03) What Role Does Trump Play in All This?

(48:21) The Future of North America

(54:59) Are We Seeing the End of Europe?

(1:00:58) How Many Americans Truly Understand What’s Happening in the World?

(1:03:50) The Effort to Destroy Western Civilization

English

先不说蓝狐论断对不对,下面这个反驳的逻辑就很可笑。

就像是一个年轻人有没有前途,要看目前的大佬认不认可。认可了就有前途,不认可就没前途。

神马逻辑?用后视镜开车吗?

Alex Xu@xuxiaopengmint

现在全球最顶的 agents(maas)全都是中心化的,没有看到人家要迁移到链上来的充分动力。投资切忌过度yy。

中文

D retweetledi

polymarket现在能开5分钟BTC涨跌

未来就能改写整个perp逻辑

听懂掌声

真正肃清行业的对手

往往都是来自于另一个次元维度

@Polymarket

中文

D retweetledi

高性能公链之间有什么区别?终局之战即将到来。

Solana、Sei、Sui、Aptos 都叫高性能公链,但他们之间到底有什么区别?

先说高性能鼻祖 @solana 。它的逻辑简单直接,更倾向于原始的“公链”模式,旨在做平台以聚合流量和用户本身。

其底层逻辑是通过海量用户和应用多样性,将链上活动转化为高频消费,进而通过手续费变现,类似于现实中的“超级商圈”。Solana 近年的动作几乎完全围绕消费端展开:手机、支付、社交、游戏、Meme;而近期与 Coinbase 的深度集成,更是补齐了其在原生流动性上的关键短板。

再来看 @SeiNetwork 。Sei 走的是完全不同的路径:它不盲目追求应用与用户数量,而是专注于吸引能带来大体量资产的发行方与机构。其战略是将美债、稳定币、RWA 等“金融底层资产”迁徙至链上,凭借极致的兼容性(EVM 生态可无缝迁移)与毫秒级清算时间,将自己打造为链上金融的底层路由器。

Sei 的工程 Roadmap 充分证明了这一点:

首先是 SIP-3: Sei 官方将其明确描述为“为 Sei Giga 清路”的升级,方向是弃用 CosmWasm 与原生 Cosmos 交易路径,从“双架构”走向更纯粹的 EVM 化路径。

存储优化 SeiDB: 为了支撑机构级并发与高频状态读写,SeiDB 定位于面向 EVM 状态访问模式进行存储优化,旨在解决传统存储层在高吞吐下的状态 I/O 与同步瓶颈。

共识加速 Autobahn: 在 Giga 语境下,Sei 将 Autobahn 作为共识路径的核心,用以实现更高吞吐与更低终局延迟的目标。

这一切布局,都是为了强化其作为“底层路由器”的核心竞争力。

另一方面,RWA 的真正拐点在于,资产一旦上链,便能 24/7 被组合进抵押、借贷、支付与现金管理工作流,且在市场波动时刻仍能快速完成权属确认与风险处置。Ondo Finance 的 USDY 已在 Sei 上线,其官方表述强调了由短期美债支撑的资产安全性,并将其引入了 Sei 的高性能结算环境。

最后是 @SuiNetwork / @Aptos 。它们更像是硅谷精英打造的“链上私人银行系统”。利用技术主权与原生安全性(Move 语言),吸引对安全有极高要求的大户、专业 DeFi 玩家及衍生品团队,定位更趋向于专业的 DeFi 基础设施。

总结:

将这几条公链放在一起对比,你会发现它们表面虽同为“高性能公链”,但在白热化的竞争阶段,各自的定位与商业模式已发生巨大分化:Solana 争夺“消费者入口”,Sei 聚焦“RWA 结算中心”,而 Sui/Aptos 则专攻“高性能 DeFi 范式”。

中文

D retweetledi

“Woomph” is a an essay on my theory about how the Fed could be printing money to manipulate the yen and JGB markets. If true money printer go fucking BRRRR!

open.substack.com/pub/cryptohaye…

English

D retweetledi

D retweetledi

In Defense of Exponentials

I used to tell founders, the reaction you are going to get to your launch is not hate, it’s indifference. By default, nobody cares about your new chain.

I have to stop telling them that now. Monad just launched this week, and I’ve never seen so much hate about a blockchain that just launched. I’ve been investing into crypto professionally for 7+ years now. Before 2023, almost every chain I’ve ever seen that launched was mostly met with enthusiasm or indifference.

But now, new chains are born into a chorus of hate. The amount of haters I’ve seen for projects like Monad, Tempo, MegaETH—before they even hit mainnet—is a genuinely new phenomenon.

I’ve been trying to diagnose: why is this happening now, and what does it mean about the psychology of this market?

The Cure is Worse than the Disease

Forewarning: this is going to be the vaguest blockchain valuation post you ever read. I don’t have any fancy metrics or charts to sell you on. Instead, I’ll be arguing against the zeitgeist of Crypto Twitter, which for the last couple of years, I’ve been constantly on the opposite side of.

In 2024, I felt like what I was arguing against was financial nihilism. Financial nihilism is the belief that none of these assets matter, it’s all memes at the end of the day, and everything we’ve built is inherently worthless.

Thankfully, that’s no longer the vibe. We have broken out of that spell.

But the zeitgeist now is what I’d call financial cynicism: OK, maybe some of this stuff has value, maybe it’s not all memes, but it’s grossly overvalued and it’s only a matter of time before Wall Street finds that out. Not that all chains are worthless. But these things are all maybe worth 1/5th-1/10th of what they’re currently trading at (have you seen these PE ratios?), and so you’d better pray like hell Wall Street doesn’t call us on our bluff, because once they do it’s all getting wiped out.

You’ve got many bullish analysts now trying to conjure up optimistic L1 valuation models, inflating PE ratios, gross margins, DCFs, trying to fight against this mood.

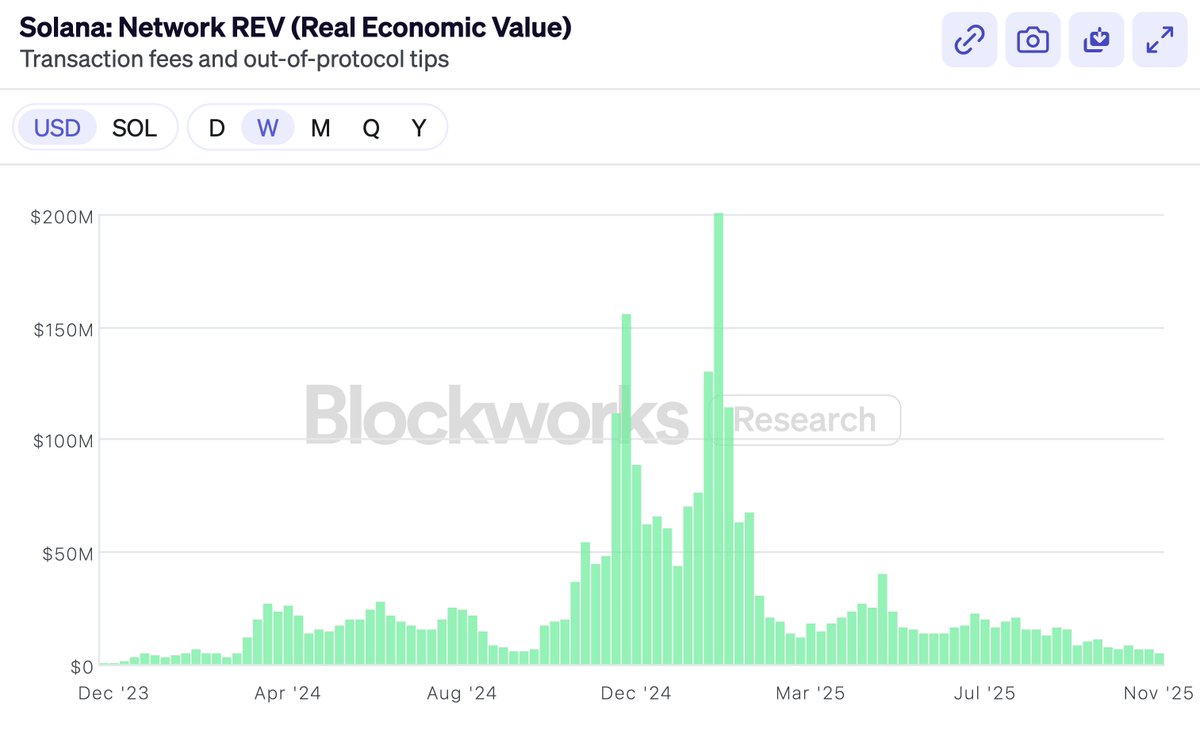

Late last year, Solana very proudly embraced REV as a metric that could finally justify their valuation. They proudly announced: we—and only we—are no longer bluffing to Wall Street!

And, of course, almost immediately after REV was embraced, it fell off a cliff (though $SOL, tellingly, did better than REV did).

Not that there’s anything wrong with REV. REV is a very clever metric. But the point of this post is not metric selection.

Then came the launch of Hyperliquid. A DEX that had real revenue and buybacks and PE multiples. And the chorus said—look, look I told you! Finally, for the first time ever, a token that has some real profits and a proper PE multiple. (Nevermind BNB, we don’t talk about that.) Hyperliquid will eat everything because obviously Ethereum and Solana don’t make any real money, we can stop pretending to value them now.

Hyperliquid, Pump, Sky, these buyback-heavy tokens are all great. But the market always had the ability to invest into exchanges. You could always buy Coinbase, or BNB, or whatever. We own $HYPE, and I agree that it’s a fantastic product.

But that’s not why people were investing in ETH and SOL. The fact that L1s don't have exchange-like profit margins is not why people were buying them—if they wanted that, they could’ve bought Coinbase stock.

So if I’m not critiquing blockchain financial metrics, maybe you think this post is going to be chiding the sinfulness of the token-industrial complex.

Obviously, everyone has lost money on tokens in the last year, VCs included. Alts are down bad this year. And so the other half of the zeitgeist on CT is arguing about who's to blame. Who’s become greedy? Are the VCs greedy? Is Wintermute greedy? Is Binance greedy? Are the farmers greedy? Are the founders greedy?

The answer, of course, is the same as it’s ever been.

Everyone is greedy. Everyone. The VCs, Wintermute, the farmers, Binance, the KOLs, they're all greedy, and you are greedy too. But it doesn't matter. Because no functioning market has ever required anyone to act against their self-interest. If we're right about crypto, we can all be greedy and the investments will still work out. Trying to analyze a market that has gone down by figuring out “who’s greedy” is going to be about as fruitful as commissioning witch trials. I guarantee you, nobody just started being greedy in 2025.

So this, too, is not what I’m going to be writing about.

Many people want me to write a post about why $MON should be valued at X or $MEGA at Y. I’m not interested in writing this post, or advocating that you buy anything in particular. In fact, you probably shouldn’t buy any of them if you don’t already believe in them.

Will any new challenger chain win? Who knows. But if it has a material chance of winning, it's going to be priced on that basis. If Ethereum is worth $300B or Solana is worth $80B, a project that has a 1-5% chance of becoming the next Ethereum or Solana will be priced according to those probabilities.

Somehow CT is scandalized by this, but it’s no different than Biotech. A drug that has less than a 10% chance of curing Alzheimer's is priced by the market as worth billions of dollars, even if 90% chance it won’t pass stage 3 trials and will go to 0. That's how the math works—and turns out, markets are pretty good at doing math. Binary outcomes are priced on probabilities, not on run rates or moral turpitude. It’s the “shut up and calculate” school of valuation.

I really don’t think that’s an interesting question to write about. “5% chance to win? No way, that’s clearly a 10% chance!” Markets, not articles, are the best way to assess that for any individual token.

So here’s what I am going to write about: CT doesn't seem to believe anymore that chains are valuable.

I don’t think this is because they don’t believe new chains can win market share. We just saw Solana dominate market share after emerging from the ashes less than 2 years ago. It’s not easy, but of course it’s possible.

It’s more that people have come to believe that even if a new chain wins, there’s no prize worth winning. If $ETH is just a meme, if it’ll never generate real revenue, then even if you win, you won’t be worth $300B. The contest is not worth winning, because these valuations are all bunk and it’ll all come crashing down before you go to claim your prize.

Being optimistic about chain valuations has become passé. Not that nobody is optimistic—obviously there must be optimists out there. For every seller there’s a buyer, and as much as CT cool kids love to drag L1s, people are comfortable buying SOL at $140, ETH at $3000.

But there’s a perception now that all the smartest people are over buying smart contract chains. Smart people know the jig is up. If not now, then soon. The only people buying here are suckers—Uber drivers, Tom Lee, and KOLs who say stuff like “trillions.” And maybe the US Treasury. But not the smart money.

This is bullshit. I don’t believe it, and you shouldn’t either.

So I felt like I had to write a smart person’s manifesto on why general purpose chains are valuable. This post is not about Monad or MegaETH. It’s really in defense of ETH and SOL. Because if you believe ETH and SOL are valuable, the rest is straight downstream.

Defending ETH and SOL valuations is generally not my job as a VC, but fuck it, if nobody else is willing to do it, then I’ll write it.

Feeling the Exponential

My partner Bo experienced the Chinese Internet boom first-hand as a VC. I’ve heard how “crypto is like the Internet” so many times now that it doesn’t even register for me anymore. But when I hear his stories, it always reminds me how costly it is to be wrong about these things.

A story he often tells is about when all the early e-commerce VCs (it was a small group back then) got together for coffee in the early 2000s. They debated: how big is the market for e-commerce going to be?

Is it going to be mostly electronics (maybe only techies will use PCs)? Could it ever work for women (perhaps they’re too tactile)? What about food (maybe impossible to manage perishables)? These were deeply important questions for early VCs to decide what to invest in and what prices to pay.

The answer, of course, was that literally every single one of them was devastatingly wrong. E-commerce would sell everything, and the target audience was the whole fucking world. But nobody at the time actually believed it. And even if they did, it would be too absurd to say out loud.

You just had to wait long enough for the exponential to show you. Even among the believers, very few thought e-commerce would become as big as it became. And those few who did, almost all of them became billionaires from just not selling. Every other VC—as Bo tells me, since he was one of them—sold too early.

It has become passé in crypto to believe in the exponential.

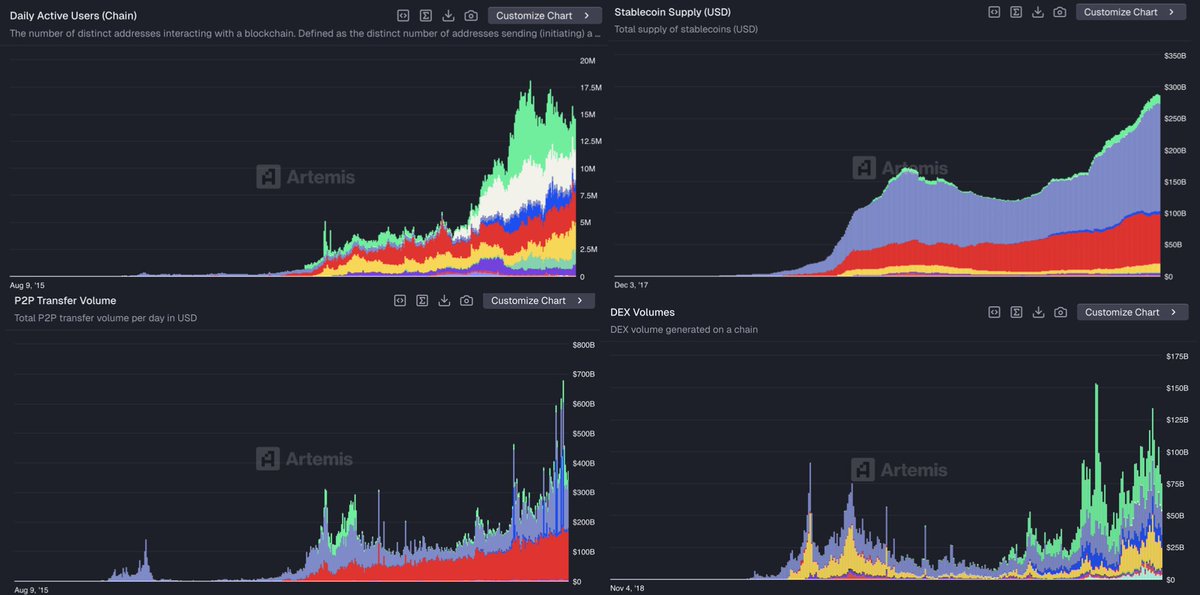

I believe in the crypto exponential. Because I’ve lived it.

When I started in crypto, nobody used this stuff. It was tiny and broken and awful. TVL on-chain was in the millions. We invested into the first generation of DeFi, MakerDAO, Compound, 1inch, back when they were science projects. I remember playing around on EtherDelta back when DEXes traded single digit millions a day, and that was considered to be a huge success. It was complete dogshit. Now we routinely trade in the tens of billions on-chain every day. I remember believing it was crazy that Tether hit a billion dollars in issuance and was being written up in the NYT as a ponzi scheme on the brink of shutdown. Now stablecoins are over $300B and regulated by the Federal Reserve.

I believe in the exponential because I’ve lived it. I’ve seen it over and over again.

But you might respond—well, stablecoin growth might be exponential, maybe DeFi volumes are exponential, but they don’t accrue to ETH or SOL. The value doesn’t get captured by the chains.

To which I answer: you still don’t believe in the exponential.

Because the exponential’s answer is always the same: it doesn’t matter. This stuff is going to be so much bigger than it is today. And when it’s absolutely enormous, you’ll make it up on scale.

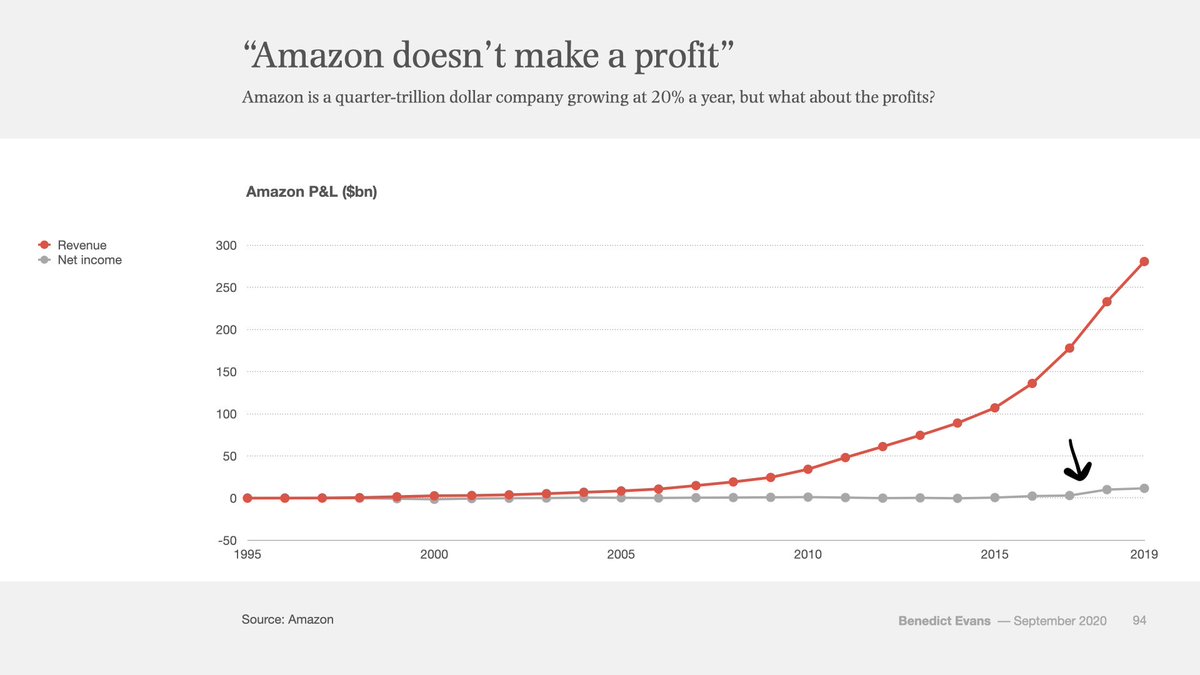

Study this chart.

This is Amazon’s P&L from 1995 to 2019. That’s 24 years. Red is revenue, gray is profit. You see that little blip on the end where the gray line goes up? That’s when, 22 years in, Amazon started actually making a profit.

Amazon was 22 years old when this little gray line of net income first peeled off of 0. Every single year before then, there were op eds and critics and short sellers claiming that Amazon was a ponzi scheme that would never make any money.

Ethereum just turned 10 years old. This is what the first 10 years of Amazon stock looked like:

10 years of chop. All along the way, Amazon was beset with doubters and non-believers. Is e-commerce a VC-subsidized charity? They’re selling underpriced cheap low-quality knick-knacks to bargain hunters, who cares? How are they ever going to make actual money, like Walmart or GE?

If you were arguing about Amazon’s P/E ratio, you were in the wrong regime. That’s the regime of linear growth. But e-commerce was not a linear trend, and so every single person for 22 years arguing about P/E ratios was devastatingly wrong. No matter what you paid, no matter when you bought, you were not bullish enough.

Because that’s what exponentials do. When it comes to truly exponential technologies, no matter how big you think it’s going to get, it just keeps getting even bigger.

This is the thing that Silicon Valley has always understood better than Wall Street. Silicon Valley was raised on exponentials, while Wall Street was raised on linearity. And over the last few years, crypto’s center of gravity has migrated from Silicon Valley to Wall Street. You can feel it.

Granted, crypto growth doesn’t look as smooth as e-commerce’s growth. It’s burstier, it goes in fits and starts. This is because crypto, being about money, is deeply tied to macro forces, and it also has more violent regulatory push and pull than e-commerce. Crypto strikes at the heart of the state—money—and so it’s more unnerving to governments than e-commerce ever was.

But the exponential is no less inevitable. It's a crude argument. But if crypto is exponential, then the crude argument is correct.

Zoom out.

Financial assets want to be free. They want to be open. They want to be interconnected. Crypto turns financial assets into file formats, makes it as easy to send a dollar or a stock as to send a PDF. Crypto makes it possible for everything to talk to everything. It makes it all 24/7, global, interconnected, and open.

That will win. Open always wins.

If there’s no other lesson I've learned from the Internet, it’s that. Incumbents will fight against it, governments will huff and puff, but eventually they will give up against the adoption, the generativeness, the sheer efficiency that this technology enables. It’s what the Internet did to every other industry. Blockchains are how that same trend will gobble up all of finance and money.

Yes—with enough time—all of it.

An old saying goes: people overestimate what can happen in two years, but they underestimate what can happen in ten.

If you believe in the exponential, if you zoom out enough, then it’s all still cheap. And it should humble you that every day, the holders outlast the sellers and naysayers. Big capital has a longer time horizon than CT swing traders might lead you to believe. Big capital has been trained through history not to fade big technologies. You know, the big gushy story that originally got you to buy $ETH or $SOL? Big capital believes that story and hasn't stopped.

So what exactly am I arguing?

I am arguing that applying P/E ratios to smart contract chains (the “revenue meta,” as it’s now called), is giving up on the exponential. It means you have consigned this industry to the regime of linear growth. It means you believe 30 million DAUs on-chain and <1% of M2 is it. Crypto is just one of the things in the world. A sideshow. It did not win. It was not inevitable.

More than anything, I’m arguing to be a believer. Not just a believer, but a long-term believer.

I’m arguing that this exponential will be bigger than anything else you’ve been a part of in your life. That this is your e-commerce. That you will look back when you’re old and tell your kids—I was there when it all happened. Not everyone believed it was possible, that whole societies could change, that all of money and finance would be transformed by programs running on decentralized computers that we collectively owned.

But it actually happened. It changed the world.

And you were a part of it.

Disclosure: These are my own views. Dragonfly is an investor in $MON, $MEGA, $ETH, $SOL, $HYPE, $SKY among many other tokens. Dragonfly believes in the exponential. This is not investment advice, but is advice of another kind.

English

D retweetledi

D retweetledi

1/12

Bitcoin Core v30 放开 OP_RETURN 限制,大家都在说是因为"Ordinals 铭文限制无效"。

过去三个月,我深入研读了 Bitcoin Core v30 的邮件列表、Citrea 白皮书和相关技术文档。 发现一个被所有人忽视的真相: OP_RETURN 政策改变的真正原因,根本不是 Ordinals。 是 BitVM。

这个故事比 Ordinals 叙事更重要。这个视角,中英文社区都没人讲过。🧵

中文

D retweetledi

Coin Center 的 Peter 在前天 Devconnect 回顾了他们为 Tornado Cash 辩护的法律细节,还一针见血地指出透明性才是 MEV 泛滥和验证者审查风险的真正元凶。

他强调隐私不再是可选项,而是以太坊维持中立性、避免因「知情」而被定罪的唯一生存底线。

这场演讲被安排为 Devconnect ARG 开幕式的压轴环节,本身就释放出一种强有力的信号,是对整个社区的一次严肃倡议。这不仅是一次法律层面的剖析,更是一份捍卫以太坊核心价值的行动宣言。

如果你不熟悉的话:其实 Coin Center 已经成立 11 年了,Peter Van Valkenburgh (@valkenburgh)是执行董事。他们在华盛顿捍卫比特币、以太坊以及后续加密货币技术的开发者和用户,使他们免受不当政府监管的侵害。

他们是挑战美国政府制裁 Tornado Cash 的主要参与方之一,在为链上隐私和开源软件自由辩护上起到了非常关键的作用。

Peter 还提到了一个有趣的观点:

> 如果你去读比特币白皮书的开头,你会惊讶地发现它几乎全是在讲「不可逆性」(Reversibility)。它不是真的在讲去中心化,也不是讲工作量证明,更不是讲区块链。

中本聪的目标实际上是中立性,正如它是不可逆性一样。对他来说,逆转的能力是与信任相关的巨大交易成本的根源。

他还提出了区块链中关于知识和权力的两条基本的规则:

1️⃣ 任何透明的事物都无法保持中立。

2️⃣ 任何中立的事物除非足够庞大,否则无法生存。

所以他认为:

1️⃣ 以太坊应该拥有基础层隐私,或者至少成为拥有盲化且真正去中心化排序器的 L2 的根账本。

2️⃣ 我们需要开发出兼顾隐私与执法的新工具,向政府证明:不通过大规模监控,同样可以有效预防犯罪。

他的演讲其实细节非常多,还解读了最近 MEV 三明治攻击的案件:

substack.chainfeeds.xyz/p/coin-center

中文

D retweetledi

$AZTEC token sale all details 👇

- total supply : 10.35B

- total token for sale : 1.547B (14.95% of the total supply)

- sale format : CCA

WHAT IS CCA ?

- well to understand this , check the below example :

In the open auction, there is 4 different time period, u can say these as epoch as well. In each epoch, different amount of token will be allocated for bidding on different price depending on the market demand.

According to the FAQ, there will be 4 epochs in total and in each epoch, there are multiple periods :

- Epoch 1 = 53,680.9 tokens per periods

- Epoch 2 = 0 tokens per periods

- Epoch 3 = 21,348.6 tokens per periods

- Final Epoch = 622,512,800 tokens in total

So, let's say there is total 3 bidders : A, B , C

1/ Period 1 of Epoch 1

In this period, the floor price of $AZTEC is set by Aztec itself which is ~$0.33, users can choose market clearing price or can set the price at which they want to buy

Now let's say -

A bids $20,000 and chooses market clearing price

B bids $5,000 and sets a max price of $0.6 per token

C bids $5,000 and sets max price of $0.4 per token

Period 1 calculation : Total money bidding in Period 1 = $20,000 + $5,000 + $5,000 = $30,000

Step 1 : Check clearing price using all bids

Clearing price = total dollars ÷ tokens available = 30,000 ÷ 53,680.9 = 0.5589 per token, this is the clearing price in this period

Check caps :

- A accepts market price so eligible

- B max is $0.60 so eligible

- C max is $0.40 which is below $0.5589 so not eligible

C must be removed from the demand set.

Step 2 : recompute clearing price with only eligible bidders

Eligible bids now :

- A : $20,000

- B : $5,000

Total Eligible dollars = $25,000

Check caps again :

- A is clearing market price so ok

- B max $0.60 is above $0.4657228 so ok

- C would be allowed only if price dropped to $0.40 or below which is not the case so C stays excluded

This price is now stable and valid. Final clearing price for Period 1 = $0.4657228, This is above the $0.33 floor so the floor does not affect this Period.

Step 3 : allocation of tokens

Allocation is always pro rata by dollars among eligible bidders at the uniform clearing price. Total eligible dollars = $25,000

▫️ A’s share

= [20,000 ÷ 25,000]

= 0.8

A will get total = 0.8 × 53,680.9 = 42,944.72 tokens

▫️ B’s share

= 5,000 ÷ 25,000

= 0.2

B will get total = 0.2 × 53,680.9 = 10,736.18 tokens

C will get his refund. The floor price for the next Period becomes the higher of :

either the initial floor set by Aztec which is $0.33 or the clearing price from Period 1 which is $0.4657228

between them which is higher become the floor price for the next round.

So the new floor price for the next Period is $0.4657228 per token.

WHAT IS LOCK UP CONDITION?

- Token purchased in this sale will be locked but the lock duration can follow two different cases.

1/ Case 1 : 3 month lock

After 3 months, only the participants of this sale can vote on whether to unlock the tokens. If the majority votes yes then the tokens unlock after 3 months.

2/ Case 2 : 12 month lock

If the majority votes no at the 3 month vote then the tokens stay locked and unlock after 12 months instead.

I just focussed on discussing the most confusing topic of this sale, if u want to participate or want to learn more, u can check here : sale.aztec.network

English

D retweetledi

区块链行业发生了什么 2

关于1011

- 在换手量上,20251011的BTC,ETH,SOL换手处于一个1%分位数事件(类似于20240805,20250407),并不是一个0.1%分位数事件(20200312,20210519,20170904)

- 主流币仅仅清除了高倍杠杆的玩家,虽然绝对数量也并不少,但是从价格表现上依然非常坚韧。表现了长期持有者对币整体的信心。

- 对于山寨币,同样的,虽然价格波动非常剧烈,但是换手整体上也是处于一个1%分位数的事件,但是振幅格外剧烈,只要你的钱在合约账户且杠杆>1.5,基本上很难幸免于难,无论是散户,二级基金,还是MM,都是一样的结局。

- 对于持有现货多头,在合约做空保证账户没有风险敞口的被动做市商而言,因为ADL的设置和在多个币种采用了联合保证金账户,价格极端的下跌导致连环清算,账户上的仓位不断减少又无法快速补仓,同时因为仓位减少更无法布置足量的订单簿,其他合约用户因为需要去合约补保证金继续抛售现货,导致现货价格瞬时抛压巨大而买单约等于0,导致价格直接下跌50%-99%。

- 主动做市商如果盯盘交易员水平够好程序有一键平仓,或许能够较早的做出动作,而减少损失。

- 事件的起因目前比较靠谱的说法是川普的对华关税言论触发市场恐慌,几十亿美金级别的资金率先砸盘,引爆 BTC、ETH 暴跌。暴跌波及了最大交易所内的杠杆体系,很多巨鲸在交易所内借 USDT 做循环贷(USDE–USDT)遭到连环清算,并且在统一账户共享了保证金,清算引擎usde抛压巨大但订单簿完全不够用导致稳定币脱锚,价格从 0.91(两次循环)打到0.8(4-5次循环)再 一路击穿至 0.66(不知道是多少次了...),形成连锁式流动性崩塌。

- 币圈的内在隐藏杠杆还是太大,非Onchain的借贷规模和内在/民间杠杆,完全是难以统计的,任何一个稳定币通过补贴和机制创新疯狂的提高市占率到一个夸张地步的时候,确实需要思考钱从哪儿来?天底下有10%-30%的无风险收益吗?这样的免费收益真的可以理解为常态收益吗?在音乐结束之前,一切都看起来那么的美好。

- 有牛市就一定有杠杆,有杠杆一定就在累计风险,风险累积到一定程度就会破灭,破灭就会出现熊市。

关于SOL

- 在2024年,SOL的创新不断,Pump.fun / meme是非常伟大的创新,让SOL成为了7/24小时的快速低磨损信息赌场筹码/类股权,SOL一路高歌猛进。

- 基金会和利益相关方因为解锁有大量出货需求,做本币币价激励极大,到处招兵买马,为SOL带来了最大的活力和最能获取眼球的dev,做出了5-6个市值大于1bil的项目,流动性非常充足。

- 2024-2025年SOL想讲的更大故事Payfi,ICM,CCM,DAT都没有成功,除了memecoin以外,没有任何实质创新了。

- 在2025年Trump币后,Binance再也没有在现货上过任何一个和SOL直接相关的资产。

- Binance发现如果继续上SOL上的资产,是在为SOL本身,Axiom,Gmgn等SOL的DEX交易平台做嫁衣,对自己的用户留存和使用习惯的培养,没有任何好处。

- Binance也想做DEX的市场,也想吃这个现金奶牛的生意,为什么要把利润拱手相让?

- 合理推测,Binance在Trump币后,SOL相关的敞口可能已经非常低了。所以没有任何理由帮助SOL,毕竟是自己BNB Chain的竟品。

- SOL现在的核心问题是没有自己的中心化交易所来为其链上资产打开天花板创造巨量的财富效应,如果SOL继续是一个赌场定位,没有了财富效应和流动性,一切都是苍白的。

关于ETH

- ETH经历了一个从理解、相信、信仰、坚守到怀疑、恐慌、人人唾弃、绝望的完整生命周期,浮筹增加了DAT、ETF也就是华尔街的力量来左右涨跌。

- 在25年上半年全部Native把ETH踢出自己的核心持仓,E卫兵变成嘲讽笑话,抄汇率的玩家一次次的痛打自己的脸。

- 四月后在信息流上端的内幕哥开始建仓,多家DAT开始私募,ETH迅速上涨;5-6月Sbet、BMNR出现,Tom Lee疯狂喊单,华尔街正式建仓,群众质疑中,Native继续空仓中,投机客看着一倍溢价的Sbet想来打一枪就跑,没有人真正相信ETH的叙事。

- 随后Genesis Act、Clarity Act 通过,Native依然还在生生质疑中看着自己最痛恨的资产无回调疯狂上涨,只有少部分做严肃研究的人明白,这两个法案意味着美国政府认可了ETH的正统性。

- ETH在可见的未来的上涨动力或者说催化剂主要还是来自于华尔街和各大法案接下来的通过和落地节奏,以及严肃的主要玩家在eth上进行真实世界应用(主要是支付、金融借贷和结算)的创新,以及或许有DAT的超预期融资/买入。

- 就像BTC ETF、MSTR的买盘不会溢出到山寨币一样,ETH ETF、BMNR、Sbet的买盘也绝对不会溢出到山寨币,只会有相关资产的庄搭便车拉盘出货。

- 我不相信ETH在这个周期能做出任何真正普世意义上有价值的金融创新,它还需要非常长的时间来被市场检验,但长期来看,其正统性已经得到了严肃资金的充分认可。

- 但无论如何,严肃的RWA,严肃的国际间金融结算,严肃的稳定币发行,大概率还是只会在ETH上进行,因为他依然是最去中心化,最健壮,有最多一流开发者,最多创新,和最多先进技术的区块链——毕竟,十年它没有一次宕机,也不可能回滚,无可代替,无可争辩。

关于Binance

- 在cz回归后,binance的打法思路都变得格外清晰。

- 从大规模换人肃清利益集团,到慧眼识珠相信技术谏言把主站流动性和Alpha流动性打通,到放开手脚敢为天下后抄袭、模仿、内部赛马、再到超越那些已经被验证过的刚需赛道,包括但不限于Perp Dex(Aster)、Meme Launchpad(Four.meme)、Prediction Market(?)、Meme DEX(Meme Rush, wallet, (0xScope))

- 在每一个赛道,依托Binance的用户基数和财富效应,都能完成对原有竞争对手巨大的吸血鬼攻击,实现快速的超越

- 最大的市场,就是唯一的市场,一旦最大的市场对长尾的流动性也开始动手,那么其他中小cex/dex在长尾流量节节败退的也是情理之中的事儿。

- OKX,Bybit,MEXC,Bitget都还没有反应过来呢,Binance已经用了从项目方那弄来的真实的补贴和用户习惯的培养,就是彻底的让利用户,不赞助红牛,不赞助迈凯轮,就是把钱都撒给散户,让Binance彻底成为各个板块的绝对头椅。

- 确实有一种,世界就是我的图书馆,“各位诸君,无一例外,我全都要”的魄力。

- Binance确实有这个行业最多的优质人才,最优质的培养体系,最有执行力的团队,和最接地气、最具Incentive的高管团队。两位把自己称为吉祥物的创始人每天活跃在CT上令人佩服,也能自上而下看出公司的战斗力和做成事儿的能力。

- Binance显然并不完美,我们都能看到这样那样的问题,人性也被暴露的非常完全,但是我相信如果不是Binance,其他人在那个位置,做的不一定会比Binance要好,所以想想也就接受就好。当然如果你收到了不公的待遇,应当大力维权。

关于BNB

- BNB的机构持仓占比相比BTC,ETH都要低非常多,具体数据根据口径不同有些许出入,但是一个小于1%和另两家大于5%的这样的一个比例感。

- BNB是一个世界最强事实垄断Crypto公司的类股权,一个不断通缩,不断销毁,不断创造利息,创始人团队持股90+%的优质资产。不同于ETH的去中心化,BNB团队继续做事儿的incentive和主管意愿都是极强的。

- BNB的DAT和ETF显然是已经紧锣密鼓的推出和融资中。两家钦点的亲儿子可以在yzi labs的投资公告中找到。如果华尔街的部分力量也来到BNB,相信BNB也会有较好的买盘支撑。

- 当然,如果说下大棋还是需要让权贵和金融标准制定者们也能上车BNB,让BNB也进入严肃资产的讨论范围内,长期抬高Binance的地位。

- 不要低估一个踏出监狱大门之后立刻能够谈笑风生的人走上权力之巅的野心,cz为了抬高binance的地位从逻辑上会在超长期会不断的做高BNB的价格,尝试让其能够进入类似MAG7类似的讨论范围之中,虽然这是星辰大海,但是crypto的渗透率显然还会继续提高,现在是3亿用户的Binance,如果真的变成5-10亿用户,Crypto总渗透量达到10-20%,这个事情可能也并不是天方夜谭。

- 最大的问题可能来自于监管。

- 以上thesis的Predefined invalidation就是监管铁拳落下,创始人决心的改变,以及bnb通缩/分润逻辑的改变,以及bnb生态发展的停滞等。

关于Hyperliquid

- Hyperliquid是Binance第一次遇到的严肃的且以前没见过物种的挑战对手,会尽可能对抗。

- Hyperliquid通过培养早期用户粘性,造富早期用户,创造极强的社区粘性和邪教般的信仰,获得了加密原生用户的最大拥护。大家对Hyperliquid的喜欢是溢出屏幕的,不管是线上,还是线下活动,没有人不觉得Hyperliquid酷,没有人不觉得Hyperliquid有品位,可能Hyperliquid就是dydx,backpack,lighter,ourbit理想中的自己的部分样子吧。

- 本质的本质,还是你无法对一个币价从开盘后一直到ATH涨了30倍的平台币说出任何怨言,尤其是在其他山寨币发币后一个月就要-90%的市场。按NBA解说的话来说,里外里,这就是差了300倍的差距!

- 另外就是,Hyperliquid找到了一个前所未有的市场,non-kyc friendly,无监管的,透明的交易和盈利榜单,清晰的清算机制,和Binance接近的订单簿深度的一个,方便隐藏自己身份、洗钱和Flex的交易所。

- 社区上:一切以赋能代币为核心,听从社区意见上币,奖励真实用户,奖励钻石手,真正有效的有意义的投票

- 产品上:克制简洁的产品界面,流动性云一般的api接口,似乎天生就是为了来做流动性的流动性而生(虽然我们都知道这是不太现实的,因为最大的市场就是binance,最大的市场本质上就是唯一的市场,足够大的size的仓位做市商一定也是去binance对冲,但事儿就是这么个事儿,叙事反正讲出来了)

- Hyperliquid获得的大型做市商支持力度还有团队的格局、操盘能力、和社区建立令人感到无比的专业和佩服。对竟对的研究透彻,代币经济设计合理,找到的KOL也都是真实有效的KOL,而不是刷粉无效的喊单KOL,等等

- 有什么缺点吗?不是早期用户咋办?没币的人咋办?

- 未来怎么办?因为Onchain的特性,我比较看好Hyperliquid和Onchain借贷和Onchain其他玩法的一些叠加产生的可组合性。本来觉得链上的可组合性更好,但其实现在可组合性最好的其实还是Binance和OKX,借贷、抵押品、循环贷,甚至不方便链上完成的网格等,实际上中心化平台的可组合性仍更强,毕竟有这么多用户在这。

- 至于在Hyperliquid上做的其他项目,还有待观察,我也想多支持几个看看,但如果继续还是Hype内部的Circle Jerk,那不一定是特别好的事儿,好的生态应该是更加包容的,但可能这也没什么办法吧。

- 最后,Hyperliquid到底能不能继续保持这样的市占率和币价,让我们用熊市、解锁和Aster来检验他吧。

其他以前写过的板块和去年没什么区别,就不加以补充。

致读者:

- btc已经涨了整整三年,减半后也过去了18个月,过往周期已经开始进入牛末熊出了,如果你尊重四年周期,且过去三年已经努力了很久,没有休息,那么出金,出金,出金!

- 改善生活,买车,给家人买好东西,提高生活幸福感的东西,学习怎么花钱,花钱是一门学问,玩耍也是一门学问,要像研究怎么炒币一样研究怎么花钱,研究怎么玩耍。

- 如果你认为未来的降息将会主导币圈的流动性,那或许还能再玩一会儿,但整体上26年的k线最大回撤会比较大的确定性还是有的,毕竟世界没有永动机,没有东西只涨不跌,整体上还是得出金。场内钱少了,大不了你就少赚点呗?

- 其实说白了就一句话,出金。

- 对赚钱这件事情,不要入戏太深,如果未来十年MAG7都会是十万亿的公司,那么其实10年5-10倍的机会就在美股,10年5-10倍,夫复何求?

- 在熊市打造自己的系统,学习AI,学习前沿知识,改善自己的知识管理系统和复盘系统,加入志同道合的社群,认识有趣的朋友,为下一次绽放做好准备。

- 不能验证的东西,一律认为都是假的。

- 减少和他人的比较,多和过去的自己比较就好了:)

希望下个周期还能看到大家:)明年见。

拓展阅读:x.com/RR_hodl/status…

中文