Sabitlenmiş Tweet

Agent 17

2.6K posts

Agent 17

@0xAgent17

CM✍️ Believer: @playcambria @re @SuccinctLabs

Saint-Petersburg Katılım Ağustos 2015

556 Takip Edilen880 Takipçiler

Yo bro! Your offer caught my eye! I'm Agent 17. I'm deep into crypto, heavily tatted, and my thing is tattooing crypto logos. Check these out:x.com/0xAgent17/stat…

x.com/0xAgent17/stat…

x.com/0xAgent17/stat…

My wallet 0x471831d7fd442c4d6882f5e5c0839064d0eab0ce

I'm prepared to complete the tattoo within 24 hours, in exchange for your compensation, of course.

Agent 17@0xAgent17

Hello to all the Goons out there!🐦 I want to share with you my new tattoo. I think this feather fits my body perfectly @plumenetwork @PlumeGoon 🩶

English

The global financial system is in crisis.

Rising transaction volumes, increasingly automated strategies, and geopolitically fragmented institutions are exposing the limits of trust-based infrastructure.

Verifiable finance matters now.

blog.nexus.xyz/intro-to-verif…

English

English

OptimAI Core Node - More Than Mining. It’s Thinking.

What does the OptimAI Core Node really do?

+ Crawls and indexes real-time web data

+ Runs lightweight AI inference tasks

+ Stores and retrieves data collaboratively

+ Powers decentralized search and compute

Each node you run becomes part of a living AI infrastructure - one that learns, evolves, and grows smarter with every participant.

The future of intelligence isn’t centralized.

It’s distributed, and it starts with us.

👉 Join the network: optimai.network/optimai-nodes

🎥 Watch the installation guide from our CCO, Ricardo, now for Windows users.

OptimAI Network@OptimaiNetwork

English

@miketwinks @re Я в ахуе , Брат , спасибо тебе за твои старания . Я как твой преданный товарищ буду всегда где то рядом!

Русский

honestly, i don’t even know where to start.

at first i thought this post should begin with an apology. but when my emotions settled, i realized i have nothing to apologize for. so i’ll just tell it like it is

what happened?

@re team just announced, without any warning or prior context, that they’re shutting down the roles system and dc in the form it existed up until today. the new idea is to turn it into an investor-focused space :)

i’m not here to judge them. maybe they know better. maybe it’s not my place anymore, and honestly that part doesn’t matter.

what i want to talk about is something else

i joined re six months ago. back then, if i’m being honest, there were maybe 30 active people on the server. i was invited by my close friend and basically my only one at the time, @stepaks576. that’s where the story began.

for six straight months, i did everything i possibly could to build a truly real community. spoiler: it was insanely hard. but we did it.

you don’t have to believe me, but i gave re my soul. my heart. my time. my ideas. my love. i was building for 10 hours a day. every day. every month.

and it was incredible.

yes, there were mistakes. yes, there were experiments. lots of trying new things. a lot of learning. but the result was insane. what we built together in half a year is massive progress. i received hundreds of messages saying people found a second home in re. that re had a soul. not to mention the visibility and growth this gave the project.

i’m proud of that. i truly believe we did it right

most of the ideas were either mine or built and shipped with my direct involvement. i did it genuinely, from the heart. i spent literally all my time on this community. you only do that when you truly love what you’re building.

we tried to make @re the best. something unique. we valued real people. we fought ai slop with everything we had. we did collabs. we supported our members in a way you rarely see anywhere else. but sometimes things happen that are out of your control.

this was my first experience in a role like this. and it was the best experience of my life. full of hope and creative freedom.

and honestly, i believe i did everything i could. probably even more.

but.

in the eyes of the team, i’m just "another community member" like everyone else. part of the crew. part of a ship they decided to sink.

maybe that’s why my pirate persona fits so well. i won’t run away from the ship. i’ll do everything i can so that my crew - and for me, my crew is you, the community - knows the truth and makes it out. if i go down alone, so be it. at least i’ll know i did everything i could.

this decision wasn’t mine. it was the team’s. and trust me, there was no ceremony around it. i wasn’t even told personally. today was a regular friday. tasks, plans, future ideas. work was in full motion :)

now none of it matters.

i know most people won’t read this far. but if you’re still here, i want to say this.

thank you. sincerely. to every real person who stood with me this whole time. you’re one of the strongest communities i’ve ever seen - and we barely had time.

thank you to the helpers. the best people i’ve ever worked with.

thank you to those who hosted events.

thank you to those who created insane content and brought creativity.

thank you to those who carried the vibe.

thank you to those who were real.

thank you, @ChazEevee you’re the best thing that happened to me in web3. i’m sure our friendship will last for years. you’re the best partner and leader i’ve ever worked with, period. kindness, freedom, professionalism, wisdom, creativity - that’s you. you’re the best thing i got from re.

thank you, @st3phdoteth you were always involved, always open to ideas, never afraid to try, and most importantly - you listened. truly listened.

thank you for giving me the chance to be who i dreamed of being. to create. to lead. to see my ideas resonate. thank you for the trust.

once again - i genuinely fell in love with our warm, cozy community. there was zero personal gain for me in this. only a big idea and a dream to build something bigger. what’s happening now is just as unexpected for me as it is for you, and it had absolutely nothing to do with me.

you probably can’t fully understand how i feel right now. it feels like a piece of me was torn away, and there will always be a scar there.

what’s next? i don’t know.

but as one wise man once said:

here it is. it turned out to be a pretty good story: interesting, fun, sometimes a little sad, and most importantly - instructive. it taught us to be brave and not to fear the challenges that life prepares for us. but most importantly, this story could have had a happy ending. Vika agreed to stay in Moscow, and i became a head chef; we would have worked together again

< 3

English

@Lxdy_rxd @re @ChazEevee @stepaks576 @miketwinks @st3phdoteth @natalieevagray @bleeshy @Unendingfates @Oluseyix @wtf4uk cuty girl

English

P(RE)ACHING THE RE GOSPEL DAY 55/56🐙

HOW TO BECOME A (RE)AL ONE 💜

I would like to sincerely thank the team and the entire @Re community for their continued support. I’m grateful that my contributions have been recognized, and I’m honored to be promoted to (Re)al OG. Proud to be part of such an amazing project and community.

LETS DIVE INTO THE DETAILS

(RE)AL CONTRIBUTOR

(re)al contributor is the first level of contributor in the Re community. To become a real contributor you must be very active and genuinely involved. Be genuine about how you contribute and involve yourself with the community how:

~ By Joining the community events

~ Chat, react, and keep conversations alive

~ Share ideas, memes, art, and helpful thoughts

~ Help organize events and start creative activities on X

~ Support others, especially during Twitter raids

A (re)al contributor shows real passion, you can feel their energy and clearly see their connection to Re. Whether on X, Discord, or anywhere else, they stay authentic, supportive, and positive, helping the community grow naturally.

(RE)AL OG

(Re)al OGs are long time community members who have been around for several months and consistently make a real impact.

They stand out because they:

~ Show up regularly and stay involved

~ Bring original ideas and real value

~ Actively join and talk about community activities

~ Are deeply engaged, not just passive members

They have strong energy, keep improving, and truly represent the spirit of Re.

(Re)al OGs are the core of the community, they help move everything forward through their ideas, attitude, and presence.

Becoming an OG is a big responsibility because OGs represent Re and help set the example and culture for everyone else.

(RE)AL GIGACHAD

(Re)al Gigachad is always active and constantly brings new ideas or value to the community. They combine (re)al skill with authenticity and stand out as someone truly exceptional.

At this level, they’re basically part of the team, a leader who sets the example and inspires others to get involved and do better.

To become part of the Re Community is one of the best decisions I’ve ever made..!

gRee familia💜

Ladyred🌹@Lxdy_rxd

P(RE)ACHING THE RE GOSPEL DAY 53/54🐙 RE IS A SAFE HABOUR Reinsurance is strictly regulated to make sure companies stay financially stable, customers are protected, and the market is fair. Even though each country has its own rules, they all aim to do the same thing. Now, onchain reinsurance @Re is building is a new area, because of this, tokenized insurance regulations are being added on top of the already strict traditional reinsurance rules. That means there are two layers of oversight. AN ANALYSIS OF RE PROTOCOL Re Protocol has to follow two sets of rules: ~ Traditional reinsurance rules and ~ New blockchain reinsurance rules. This is because it connects the traditional insurance world with blockchain technology. In July 2025, a law called the GENIUS Act was passed. This law sets clear federal rules for stablecoins digital currencies used for payments. The law doesn’t directly control Re tokens, but it does affect which stablecoins can be used inside Re Protocol. Under the GENIUS Act, only stablecoins that meet federal standards, are issued by approved financial institutions and are fully backed 1:1 by safe, liquid assets like bank deposits are allowed to be used as payment stablecoins. REGULATION CONSIDERATIONS FOR TOKENIZED REINSURANCE IN 2026 In 2026, tokenized reinsurance is being guided by three main sets of rules, all overlapping with each other. 1. UNITED STATES “SEC rules”: In the U.S., regulators treat tokenized reinsurance like investment securities. This simply means that these tokens must either be officially registered or qualify for a legal exemption, Companies must clearly explain risks and details to investors while Investor protection rules still apply, even though the product is on blockchain. 2. EUROPEAN UNION “MiCA rules”: In the EU, companies offering tokenized reinsurance must get a special crypto licence “MiCA licence”, perform identity checks “KYC/AML”,hold enough capital to stay financially stable and follow consumer-protection rules MiCA also clearly defines which crypto assets fall under its control. 3. BERMUDA “BMA rules”: Bermuda is creating rules specifically for tokenized insurance and reinsurance by updating its existing insurance licensing system, clearly defining what counts as an “innovative” or blockchain-based insurer and Providing clear licensing paths for onchain reinsurance and insurance-linked securities “ILS” All of these rules together creates a clear framework for how tokenized reinsurance should operate in 2026. Projects must follow laws in different countries, keep enough capital, properly manage risk, and be open and honest with investors. These regulations are not designed to stop growth instead, they make sure companies operate safely and responsibly. Because strong rules are now in place, more people and institutions will trust and adopt tokenized reinsurance in the near future. Re Protocol was built exactly for this kind of environment one where trust, safety, and investor protection are essential. So insurers, reinsurers, and investors using Re Protocol can feel confident knowing their funds are protected by strong, well defined regulations and high operational standards. RE IS A SAFE HABOUR 💜

English

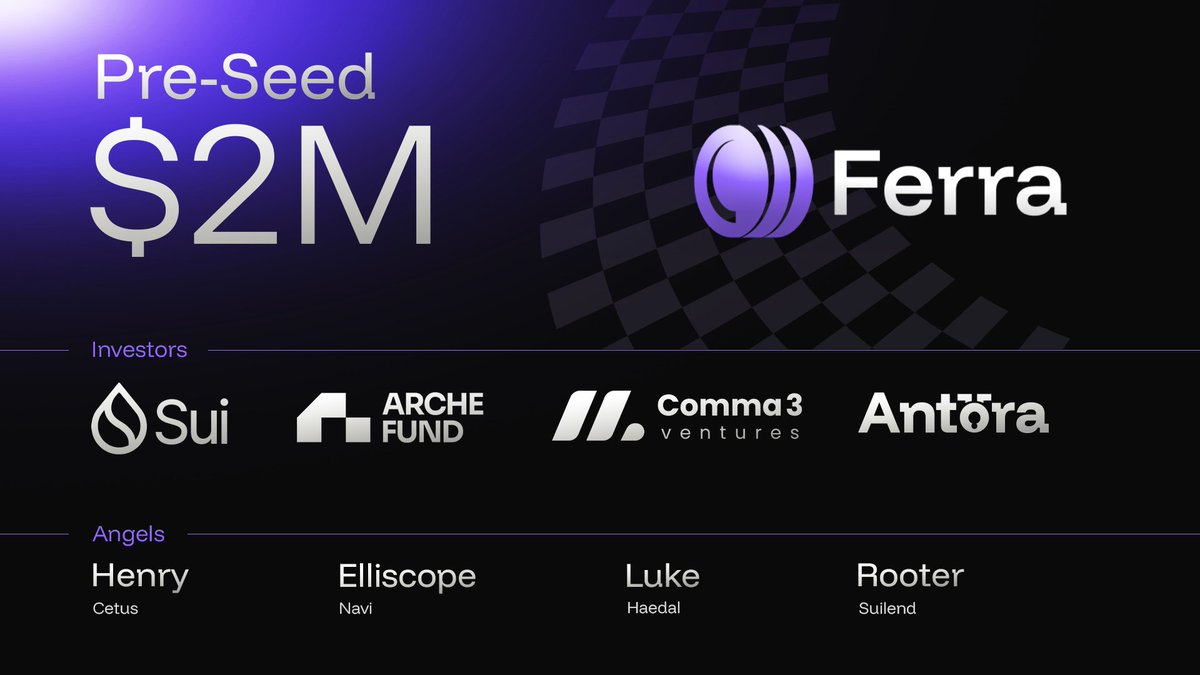

Ferra's fueled.

Announcing our $2M pre-seed round to build the dynamic liquidity layer on Sui, unifying DLMM, CLMM, DAMM DEX models plus a holistic DeFi toolkit.

The round was led by @comma3vc, with participation from @SuiNetwork, @ArcheFund, @AntoraTech, @henrybuild from @CetusProtocol, @elliscopef from @navi_protocol, @Lukeeeeal from @HaedalProtocol, @0xrooter from @suilendprotocol.

English

this is a very common take that SOUNDS CORRECT at a glance, but is the #1 reason almost all games in this industry have failed so far. 99% of crypto games failed because they weren’t financialized enough or honest enough about where the product-market fit is.

as a new game, you need to have one big twist or innovation that makes people actually come check you out, when they could be playing one of the thousands of EXTREMELY good games out there in the market. no, ingame items / skins / products onchain is NOT ENOUGH of a twist for people to care.

the benefits of onchain do NOT matter enough to 99% of people to swing repeated behavior. they can only improve what’s already working with the core game loop especially one designed with RMT and onchain assets from the ground up.

in web2, a shitty game can be somewhat of a success. with crypto games, with the amount of money that has been put into it at the outset, it needs to absolutely COOK as a crypto business or fails by default, regardless of whether or not its fun. this is the fundamental business model disconnect that has resulted in the -$XXB loss that crypto gaming is in.

because of this massive, fundamental flaw in the investment thesis - the teams / investors / founders that were earliest to launch tokens into the gaming narrative while it was still alive are the only winners (so far), cashing in before there was enough time for evidence disproving the “crypto gaming thesis” to accumulate.

if you aren’t in the target audience for degen games, you will never understand how to build these games. why would I care about a crypto game that’s not financialized? hell, I don’t even play the best web2 games anymore, even though i grew up spending most of my early life playing games. how could these “just make a fun crypto game” titles ever compete for my attention?

what works is niche, but imo will grow extremely rapidly - degen / risk-to-earn gaming as part of financialized entertainment vertical (perps, memes, prediction markets). there’s a thrill in risking assets that is just net new entertainment especially suited to this generation of terminally online people.

the challenge for crypto games here is you need to win at two things at once, it needs to be a fun and ADDICTING enough game (very very hard) that has the intagible cool that gets people to care about the game (emotional investment) AND you need to have the ability to run MASSIVE stakes at scale while avoiding the million pitfalls that will completely sink the game. along with #2 is being able to CONSISTENTLY attract both ATTENTION and LIQUIDITY to the game - this is a bar that web2 games do not have to clear.

its not impossible or the holy grail even to do all of this. just look at web2 - I’d say the gacha games (Genshin, Honkai Starrail) have been able to not only build geniuely fun games, but also kill it with a winning business model (gacha spins for characters). done correctly, the two feed into each other and its a beautiful thing to witness.

all of this said, i think the OP is still correct in that the “game needs to be good” - there needs to be a very strong central core to the game that people care about that you can stack the financialization on top. e.g. prediction markets latch on to stuff people care about - big news events, sports, etc. - and get this core for free. perps latch on to the price action of crypto and other assets for the “””trading””” that happens on top. the key is the content core needs to consistently keep attention, and be 24/7 emergent and ever-evolving where it can never be “solved.” e.g. hyperliquid needs to launch more things to bet on (silver, web2 stocks) to grow.

I also don’t think you need to make a game good enough to be GOTY standalone to have a financialized game that works and makes money. think about EVONY back in the day, those shitty games that get advertised constantly, most of them just latch onto a winning business model for a game (gacha) and spend a shit ton to get as many people to churn through the money making machine as possible. you can do that in crypto too. its the same arbitrage where someone might get bored of playing a triple-A, massive budget game and instead spend the same money and time playing fking vampire survivors because it makes their brain feel good.

but a game with massive amounts of crypto volume flowing through it, or better yet a complex / high-depth economy with crypto assets (economy worth billions) would absolutely become the biggest gaming company ever, by an order of magnitude. a game taking volume-based fees aligns incentives with players in ways that potentially could solve the fundamental misalignment of games monetization that even gacha / microtx / mobile could never achieve. crypto games have massive LTV / ARPU potential as well because of the pyschological effect that people have when buying something they can sell later - they are willing to pay 10x+ more.

two indicators i think to watch when tracking the next breakout crypto game:

1) how much do people care about the core thing (IP / wahtever u wanna call it)? you can look at how much the cosmetics are going for, a lot of other intangibles. this is the only edge that games specifically have against perps / memecoins / casinos, where people will never care deeply about anything except the buzz of winning money.

2) how controversial the game is getting? I 100% believe that thsi is the only way for crypto gaming specifically to scale a consistent pipeline of attention and liquidity. the more people are absolutely railing against the game (especially web2 gamers), the stronger the signal.

if you're building a crypto game - my advice is don’t start with trying to put everything on chain or launching a token. get people to care first (up to you on how), and find a way to create an experience that creates enough $ flow through the game, it doesn’t even have to be sustainable at the start.

last thought - consumer apps is ultimately just about finding new ways to elicit the most powerful emotions possible from people. if you can consistently put people in the “zone” (think grandma fucking locked in on a slot machien for 12 hours) or elicit new emotions from your consumer experience that are not common in modern life, people will remember you forever, and you gain LONG TERM equity - people will come back to try every new release. its the same reason people remember their first kiss or sexual experience forever. not enough teams are systemically optimizing their experiences to maximize this.

Zeneca🔮@Zeneca

99% of crypto gaming projects have been about making money, tokens, and the financialization of everything.. and that's probably why they've almost all failed I dunno what the answer is, but it's pretty clear at this point that ponzinomics and tokenomics based on a house of cards are not the way Most gamers are not gamblers Most gamers want to play games for fun, not to think about $$$$$$

English

usd stables were just a beta test

real mass adoption is non usd currencies and onchain fx

global commerce doesn’t run on one dollar, it needs liquid eur gbp mxn and more with clear routing

the problem was never demand it was missing rails

@codexfx is building exactly that an infra layer for global money. native swaps, atomic off-ramps, bank spreads slowly dying

the line between fiat and crypto is fading

@Vonnie610

GIF

Ash@ashxyz

English

Mando's Gilded Christmas 🎄

Live tomorrow at 11am ET

NEW: Gizmo's Folly, Ice Fishing, new Rewards, & more!

English

@LOL_proof @playcambria What's your big play for Season 4? @lorax1337

@floppitoki

I'll buy a crate of energy drinks and grind mobs.

English

Yo, Cambria fam! 😍

New Year is literally right around the corner, and what better way to kick off 2026 than snagging some fire T1 assets for @playcambria ? Scoring these as a holiday gift would be straight-up legendary – perfect timing to stack your bag before Season 4 drops!

📩I'm giving away:

3 T1 Islands (one each to 3 lucky winners)

6 T1 Cores (two each to another 3 winners)

That's 6 winners total getting hooked up with premium land and cores to dominate the risk-to-earn meta!

To enter!

1) - Follow me (@LOL_proof )

2) - Follow (@playcambria )

3) - Like + Repost this post🩷

4) - Tag 2 frens in the comments and drop: "What's your big play for Season 4?"

Giveaway runs for 7 days – winners announced on December 28th! Random draw, fully transparent, prizes airdropped straight to your wallet.

No purchase needed, open worldwide. Let's get that holiday hype going!

#CambriaGame #NFTGiveaway #Web3Gaming #RiskToEarn #ronin #HappyHolidays #Web3

English

Русский

gmbria @playcambria @cyberpunk

Season 3 finally live.

10 days of full lock in.

Good luck to all of u guys.😈

English

Русский

gliquid everyone!

we're hosting a big crosscommunity poker night this friday with @0xfairblock, @PrismaXai, @magicblock and @Euphoria_fi, gonna be a fun one.

full announcement dropping in the discord soon. stay tuned 👀

English

English

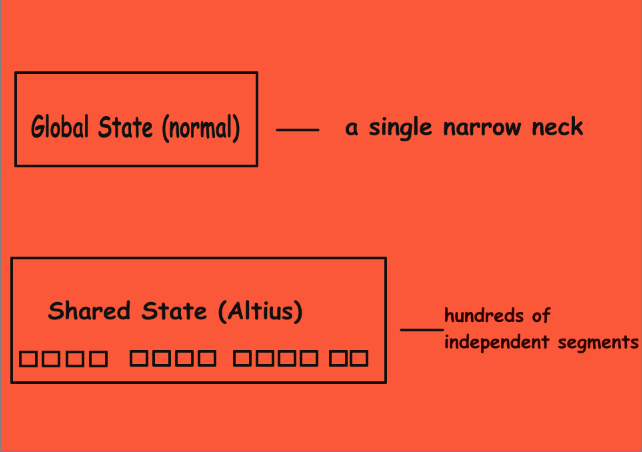

ALTIUS - a new execution architecture that changes the rules of the game

Today we will talk about Altius, a new high-performance execution system that solves the fundamental limitations of modern blockchains

To understand why Altius is needed in the industry, it is important to first understand the problem

Why standard execution layers are no longer sufficient

Most modern chains (EVM, Cosmos, Move networks) face the same limitations:

1. Sequential transaction execution

Each transaction waits for the previous one → delays increase → TPS reaches its ceiling

2. Limited storage capacity

One global state → one input stream → bottleneck

3. Poor scalability under load

As the network grows, the load grows faster than its capabilities

4. Low efficiency of parallel execution

EVM cannot be parallelized properly. Cosmos can be parallelized partially. Move is better, but still within the general architecture

And this is where Altius comes in, essentially rewriting the execution layer

What makes Altius unique?

In short:

Altius is a new type of execution layer built around parallel execution, sharded state, and instruction-level parallelism

And now in detail and in plain language

1. Parallel Scalable Storage

In most blockchains, the state is one "big file." Altius turns it into a bunch of independent cells that can be read and changed at the same time

This means:

- no queues for data access

- no global lock

- transactions no longer conflict

- TPS grows linearly with the number of shards

2. Instruction-Level Parallelism (ILP)

A unique feature of Altius:

the network understands the dependencies between instructions within a transaction and executes independent operations in parallel

This is what CPUs do, but no blockchain does yet

Fields that can be executed in parallel are executed in parallel

Dependent fields are executed sequentially

This increases speed not by 2–3 times, but by tens of times

3. Multi-chain & cross-chain ready out of the box

Altius is not tied to a single virtual machine

He works with:

- EVM

- CosmWasm

- MoveVM

And it can be integrated into multi-chain ecosystems as a single execution engine

In other words, Altius is not "its own chain"

It is a universal engine that can be installed under the hood of any network

4. Modular architecture

Altius divides the system into three layers:

1. Execution Engine — executes code

2. Scalable State — stores data in parallel sharded structures

3. Consensus Layer — a common layer compatible with different VMs

What does this give developers?

Predictability of performance - transactions do not wait for each other

Scaling without forks and L2 - more shards → more power

Interoperability between ecosystems - one engine → three VMs → dozens of networks

New types of applications:

- high-frequency trading

- game worlds with a large number of objects

- aI agents operating on-chain

- real-time dApps

Result

Altius is not just "another L1"

This is a new class of execution engines that give blockchains what they have chronically lacked:

- parallelism

- scalability

- VM flexibility

- real performance on par with modern processors

Altius solves the problem of deterministic performance

@AltiusLabs @paskal_navi @ihorbielov

#AltiusDropzone #altiuslabs

English

gRE my fam 🫶

We decided to play a little game with @miketwinks and defeat the villain Vecna👻

@re - It's something more...

English

If you run a Web3 or traditional gaming guild, we want to help YOU and your guild jump into the game!

📜 : blog.roninchain.com/p/introducing-…

English

Great article to get you up to speed on @playcambria Gold Rush S3!

Final chance to apply for the Ronin $25,000 Guild Rush Program 👇

Eleni@elenionchain

English

we had 5 IRL @playcambria energy orbs during YGG Play Summit and no one won the last one 👀

🚨 GOLD RUSH SEASON 3 CONTEST 🚨

- whoever is the #1 leaderboards player at the end of S3, i will personally ship this IRL energy orb to you with a hand written letter of congratulations

by land, by sea, and by air, God shall bless you with unending glory

may the best player win.

English