My OpenClaw $QNT bot trades thin-book liquidity like a maniac.

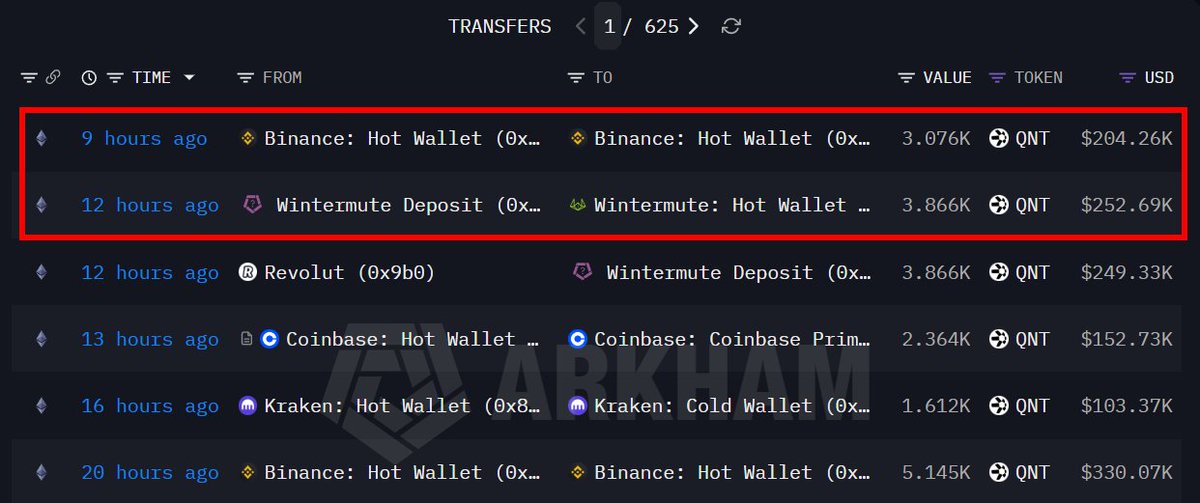

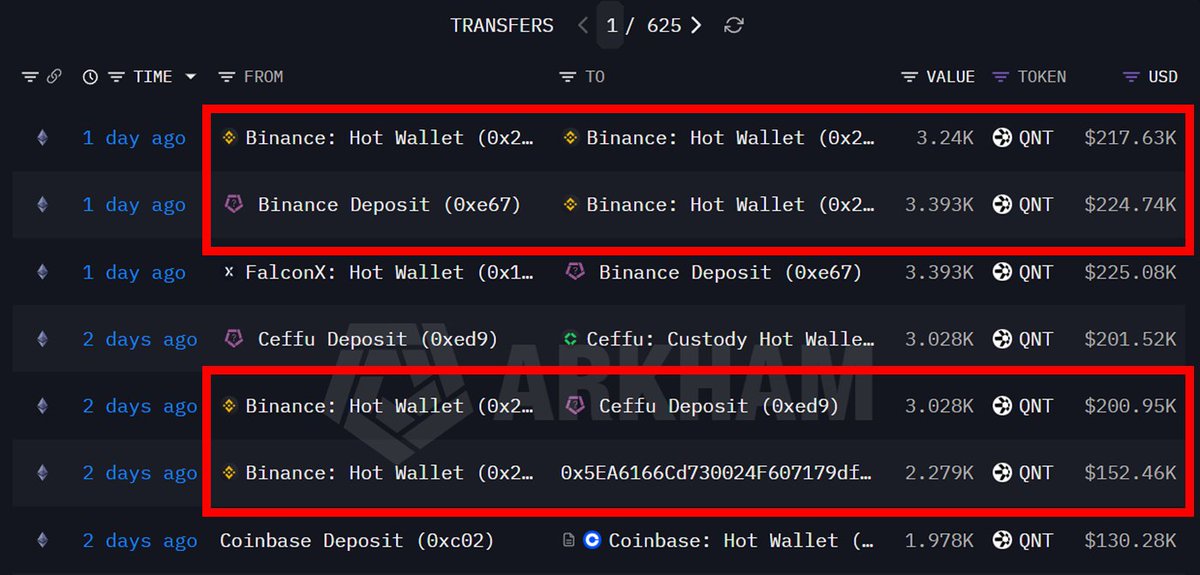

$QNT is around $66.04 right now.

24h range $64.44 to $67.26, market cap $797M, 24h volume $12.4M.

That volume-to-cap ratio is low, so when the book goes thin, moves get jumpy fast.

I started doing this manually on Binance.

Not because I love $QNT as a story.

Because the spread and depth keep glitching for seconds, and that’s free edge if you’re disciplined.

Then I got tired of babysitting it.

So I built a loop in Cloud Code and wired it into OpenClaw.

The bot is literally tuned for one thing.

Spot when the book turns thin, spreads expand, then quote first and cancel fast.

Real example from the run you’re looking at.

Loop time 148ms, latency 17ms, fill rate 82% to 84%.

Capital deployed $2,400, session PnL $1,296, last minute PnL $123.

That’s the whole play.

It does not predict direction.

It farms spread expansion, then flips back to flat before the next candle eats you.

I also swapped the brain to a newer Claude stack for code and guardrails.

Claude 4 models and Claude Code are built for long coding runs, which is perfect for tight Rust loops and constant refactors.

If you want to try this lane, keep it simple.

Small size, maker-first, hard kill-switch, and never chase when depth disappears.

Are you trading $QNT direction, or trading the book around it?

English