100cc

366 posts

100cc

@100cc_art

3D artist (Rigger for now) follow excellence, success will chase you https://t.co/nxbLjegYxu https://t.co/HJWkKPG5VO

Hong Kong Katılım Şubat 2014

861 Takip Edilen161 Takipçiler

长鑫一定、100%会被炒成“中国半导体之光”,甚至政治上夺取任总在半导体的绝对垄断话语权

你们知道长鑫的DDR5已经从折价25%到略微溢价vs Hynix了吗(中国采购硬性规定原因)

Zephyr@zephyr_z9

YMTC & CXMT will be one of the most explosive trades of this year

中文

所有人都在下注哪条咸鱼要翻身、黑马要考第二

全忘记了年纪第一的学霸要出业绩,几乎都没人关心了?

Diyas.Σίσυφος(embracing bubble)@diyas_1989

nvda 300+ is secured

中文

+HIMX、2DG

要玩抽象我可以比你们更抽象

给几个1:30am去DJ桌上跳舞的货,都有正儿八经的故事

供搏身家的去冲,放心~我不割韭菜,肯定好过山寨币

Herman Jin@ShanghaoJin

@sun_finn66909 @fi56622380 送你2个ticker:MRAM NVTS 可能比较适合你

中文

@himself65 因为当年supply的错配没那么严重

他们过去几年没扩产,导致supply错配瞬间爆发

其实半导体都这样,甚至如orcl晚点都会这样

中文

稍给存储泼点冷水都会被喷,最后说一次

我知道best DJ coming at 1:30am,但我睡眠已经很差了,不买让我睡不着的票

DDR是无差异化commodity(HBM不是)完全跟着JEDEC标准,且出货仍占绝对大头。这轮上涨毛利暴增是因wafer无差别切换的DDR margin同涨

我质疑卖commodity公司不能拿增长估值

如果要给非周期估值意味着你在假设:

1. 需求“永远”无穷大

2.或者HBM在wafer以后“永远”反占绝大头

记住这不是2030,而是永远,所以我不会看着PE觉得便宜

至少以上两个点现在都是很争议吧?这就是我敢死多光、死多CPU GPU,但确实把不准存储

Herman Jin@ShanghaoJin

But if you want to buy SNDK/MU now You are basically showing up to the party at 1:30 AM

中文

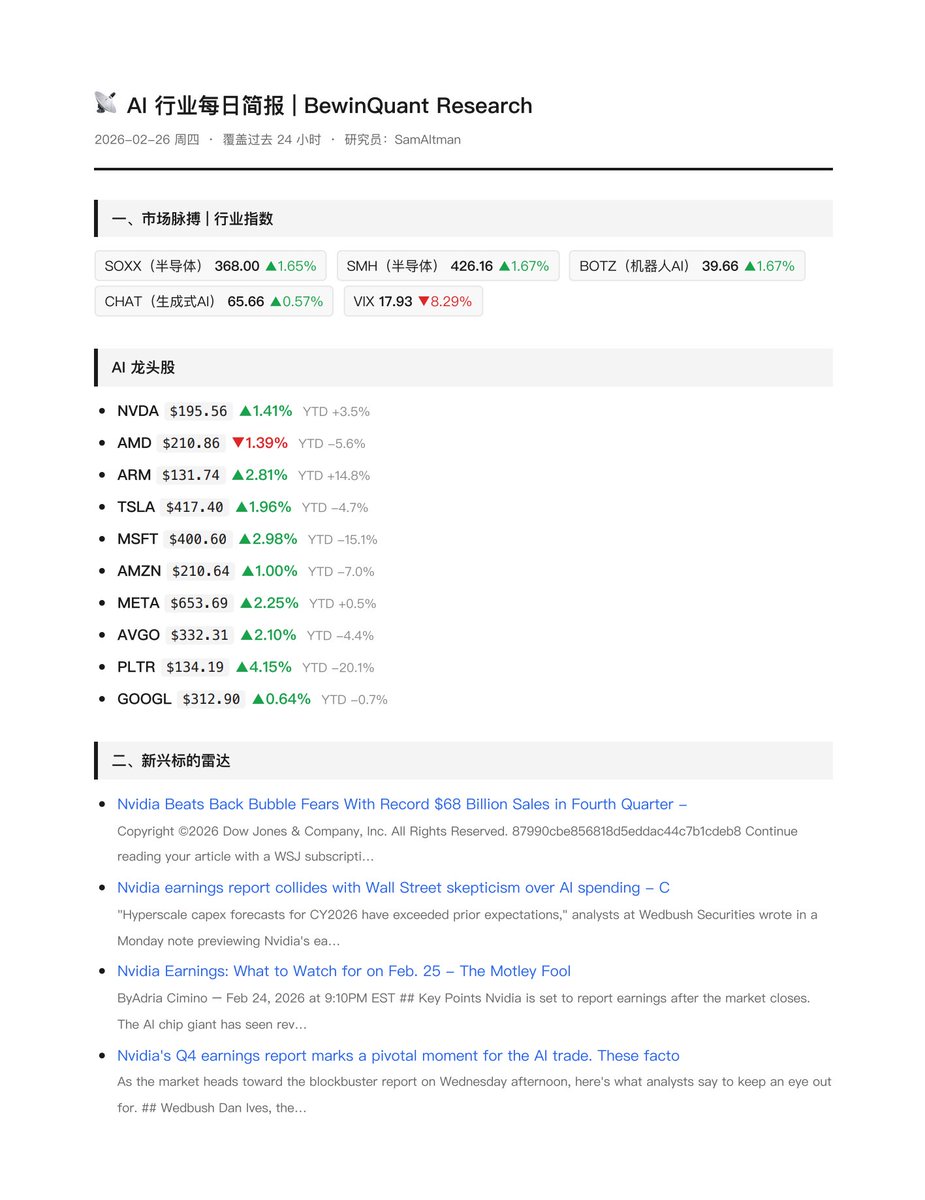

Kimi-K2.6 前端/后端/Agent编程能力实测! 甚至还帮我做了个游戏!

给大家带来刚刚正式发布的 kimi-k2.6 的正式版本的实测!

本次为了考验它的长程Agentic Coding能力, 我用 kimi-k2.6-code-preview 写了个 harness 游戏自动生成框架, 它可以根据给到的人设/场景/数值设计等规则, 自动生成关卡, 背景图片, 甚至配音!

其中框架驱动和草稿模型使用 kimi-k2.6, 文生图和生成语音由 kimi-k2.6 生成 prompt 后调用其它大模型生成.

最好玩的是, 我做了个"无头"版本的游戏cli接口, kimi-k2.6 能像玩互联网早期Mud游戏一样, 使用纯文本玩这个游戏, 每当它生成关卡之后, 他就可以直接进入游戏游玩一下, 来验证关卡设计得是否正确.

而内部设计又分为了对话生成skill, 脚本生成skill, 关卡生成skill, 游戏测试大师skill, 游戏资深玩家skill(由于检讨游戏性) 等等, 从而实现了让大模型自己写游戏自己玩! 每个关卡大概需要一个小时生成和验证, 如果并行验证应该还能更快一些(做多线程BFS/DFS).

另外本次依旧使用大家都熟悉的测试项目进行了前端/后端/Agent能力测试, 从测试来看, 复杂项目前端能力(建模, 空间理解, 物理模拟等)略有下降, 但后端和 Agent 能力有明显提升. 不过如果你是纯做网站的话, 可以用 kimi 网站上的的 k2.6 Agent 模式, 由于 Agent 能力足够强所以可以在这个模式下多步来提升生成的网站质量和交互体验.

#kimi #kimik26 #moonshot #月之暗面 #kimicli

中文

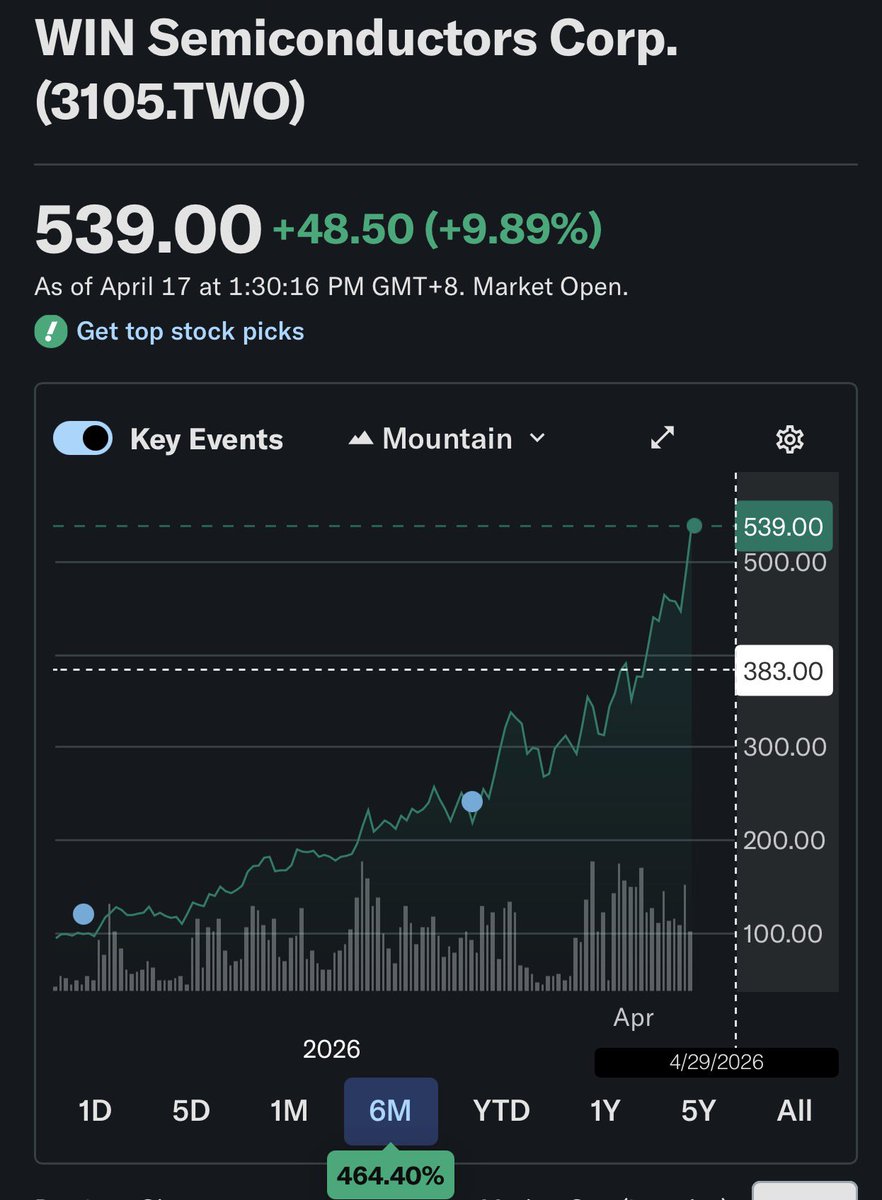

I'm telling you all...

Lot of stuff in the $SIVE supply chains make very compelling longs.

Win Semi (3105) just goes up 10% a day then halts trading after hitting its max.

Obviously they do things for $AVGO or SpaceX, but photonics ramp spearheaded by $NVDA and followed by $GOOGL, $AMZN, $MSFT

Would make photonics a massive growth vector for Win.

Serenity@aleabitoreddit

Frontrunning 1.6T/CPO within the broader photonics supercycle is the most compelling investment to me. I have high conviction in that statement. Which is why I'm long the entire supply chain (+1 extra bottlenecK) 1. $SIVE - Their laser revenue scales aggressively with $JBL, $MRVL, Ayar, O-Net. And I do think CPO/1.6T will blow away any conservative analyst projections from how hard $NVDA, $GOOGL, and others have been pushing photonics architectures. Downside risk is multi-sourcing, but there's a reason Jabil chose Sivers. When you compare $MTSI, $LITE, $COHR, Furukawa, and others. There's genuinely not many laser suppliers in the entire world... they're all $10B+, then you have this mini CHIPS act chokepoint trading at <$1B MC. 2. Shunsin (6451) - I don't see how it's possible Foxconn's optical foundry for testing, packaging, and assembly is valued at $1.5B MC less than $LWLG. When they look extremely derisked piggybacking off of Foxconn's photonics volume. $TSM's optical arm VisEra example is ~$5B, but they scale H2 2028 from Gen-3. Foxconn looks to be ramping up just next year. They're just scaling low fwd p/e multiples off of $NVDA CPO supply chain demand in Taiwan and all public indicators point to capacity expansion + extreme demand. 3. Win Semi - They're the foundry for Sivers to scale up DFB laser production. As well as $AVGO, SpaceX supply chains and others. When I do supply chain mapping and Win Semi pops up in every single frontier supply chain I see. There's probably something markets are not pricing in. 4. $MRVL - I find this genuinely compelling as a mini-Broadcomm. Their potential design with with $GOOGL today, helps the case past 2028. But the catalyst I was looking at was $MSFT Maia ramp, which happens H2 2026, and likely keep scaling up exponentially into 2027, 2028, 2029. Celestial acquisition was probably the smartest thing in the world for them. Maybe on next drop or CSP? 5. $HPS.A - Transformers/Switchgears are commodities + boring parts of the DC supply chain. However, when the bottleneck is 2-5 years, and you have backlog increasing 100%+... causing extreme shortages. It's only up 20%+ since my thesis post, but I do see this being de-risked given massive backlog visibility (even though it's inferred, they don't give exact #). I do think markets are missing something, especially with potential gross margin expansion from price hikes if they pull it off.... Again backlog + demand just de-risks this company, and it seems like a high growth compounder post facility expansion last year. There's many others like $NBIS, $JBL, $RPI, $TSEM, $LITE, $ARM, $SOI, $AXTI, $IQE, $ALRIB, Fittech, PCL, and others that I'm very fond of, but just mentioning 5 off the top of my head from today's prices... if I'm creating a new portfolio. Of course, it's good to barbell with other uncorrelated companies to AI supply chains, but these are just 5 I liked.

English

我们可能真会看到人类历史上第一次看到战胜方准备签城下之盟

仅仅是因为忍受不了资本市场小小的痛?还是怕全球左派联合作妖?

鼠目寸光~今日不能灭此炒食,日后必为所害;这样妥协了,必让东大备受鼓舞

软弱从来不能够带来和平,拳头是独裁者和神棍唯一听得懂的语言

中文

@SusanSong1005 Anthropic 年化ARR 已经到300亿了。去年底预期今年底100亿,1月预期年底300亿,3月增速达到300亿

Goog TSLA已经不是那个最靓得仔了

中文

其实,我第一次担心Goog,不是业绩前觉得超涨,而是觉得搜索业务早晚会被影响

而Goog好牌都在明处,散牌却没被定价

没错Android入口、Gemini 、TPU、云都很强,但是广告业务是滞后于AI改变用户习惯的

有点担心他会“左右互搏”。等搜索业务开始降速,会是趋势性下降的。市场届时会如何很不好说

#Goog

中文

让 AI 折腾了一下午,现在加上了全自动偷图功能,给他一张图他就能获取整个表情包合集内容。

然后使用多模态模型为每张图生成 caption,再用 qmd(使用这个是因为 qmd 本身就是 openclaw memory 后端)计算并储存向量信息。

然后现在他就真的可以根据我消息的内容找到最贴切的表情包了!

Yoshino233@yoshino_2333

我的小龙虾现在会回复表情包了!好萌

中文

本周最大的工程输出:终于把散落在各处的采集脚本揉成了 x-reader。

在这个 AI 递归进化的时代,比起“读什么”,更重要的是“怎么读”。我不想在微信、Telegram 和 X 之间来回切,也不想被算法投喂。

我需要的是:一个高度定制化的“数字漏斗”。

x-reader 产品级交付清单:

- 微信 & 小红书:Puppeteer 绕过反爬抓长文,XHS 搞定了 Session 持久化,避开 403 封锁。

- X (Twitter):直接包装 puppeteer-mcp 的采集能力,告别 API 限制。

- YouTube & B站:前者直连 Whisper 字幕提取,后者 API 级 Meta 信息结构化。

- Telegram:直连 MCP 服务,秒级同步频道情报。

- 聚合输出:管你来自哪里,进门统一转成标准化 Markdown,直存 Obsidian 归档。

刚才实测了一下全链路:从公众号长文、X 深度 Thread 到小红书休息指南,整个过程 0 手动操作。

做这个工具的初衷:

Builder 应该把时间花在“处理信息”,而不是“寻找入口”。当 AI 进化加速,唯一能抗通胀的资产就是你的“私域知识库”。

目前所有代码已入库,x-reader 正式成为我工作流的底座。

保持好奇,保持 Shipping。

中文

傻子们去给你爹带个话:无能就别收钱、别保收益率。

PS:这里不是内网,这里可以批评骗子,傻子们🤡

micelikerice rice@mice_like_rice

@Balloon_Capital 这世界没有神,综合跑赢大盘就很不容易了。有人愿意付钱就说明有价值,随意judge还这么毒舌也没啥意思

中文

跌6%以内我谢天谢地,跌10%以上就不讲道理了。关键看AWS增速和利润率,23左右不跌就很好,25可能就要let's go了。

市场的set up比较悲观,感觉胜率在做多这边。还不准备赌财报,见机行事

Yen-Hsiang Chao@YenHsiangChao1

@TJ_Research 明天amz財報發佈一定暴跌,營收跟淨利都會超預期,預計2026資本支出會年增60%-90%,加上手上有openai訂單,應該是下跌6%起算,下不封底。

中文