Sean

11 posts

I have sold my entire wti futures position overnight. I don’t have the balls to short it but happy with this run. Will leave it alone till it gives me the opportunity of a decent re-entry after the mkt retraces and retrace it will

English

@clkleinmonaco How should someone position themselves right now for the best risk-to-reward, assuming they’re staying in equities and maybe using options as an overlay?

English

@clkleinmonaco Thank you — I really appreciate you sharing these thoughtful ideas during such a turbulent time.

English

@BuBarrelBull Really appreciate the thorough breakdown. I completely agree with your assessment—gold’s unique supply/demand dynamics mean the standard cyclical rules don’t apply. PNAV at spot is a much cleaner lens for valuation here.

English

Like a lot of things, it depends. Valuation multiples in cyclical equities *should* compress near cycle highs and should expand near cycles lows. So, if you’re only looking at multiples simplistically, they might look cheap at cycles highs.

Despite that logic sometimes the opposite happens, as was the case, for example, with lithium equities over the past few years. It often depends on whether the market judges the cycle as durable or not.

Either way that’s not how I’m thinking about it.

I’m looking at PNAV at spot gold. It removes the cyclicality. At any point in the cycle, you’re asking, how are the equities trading versus the commodity. I’m not assuming the gold price stays at $5000. I’m just saying, if it does, I think the equities are attractively valued against that assumption.

Gold equities are a bit different from other cyclical equities because gold is a bit different from other commodities. Gold isn’t really consumed like other commodities, with the vast majority of gold that was ever mined still being in circulation. So the elasticity of supply is sort of … irrelevant.

In commodities, traders often say “high prices solve high prices”. The reason is that if prices rise you get a supply response. Also, you likely destroy demand, depending on the demand elasticity.

Whereas with gold, sometimes the rising price actually drives *more* demand as investors chase returns. It may incentivize investors to sell to other investors, but the increase in mined supply is virtually irrelevant relative to the potential swings in investor demand.

In literally any other commodity I would say that through-cycle prices are relatively bounded by the cost of production. Meaning, over long periods they won’t trade at a significant premium to cost of production, and the time in which thy do will depend on the elasticity of supply.

Gold can trade above cost of production indefinitely.

So, for that reason, I don’t think it makes sense for gold equity multiples to compress near cycle highs (assuming this even is a cycle high). I think that should trade close to 1x price-to-nav (at spot) in aggregate. And I’d say the majors are trading at a discount to that.

English

It feels like it needs to be pointed out that gold is up 10% YTD

English

@latinmines Hi Latinmines,

Are you no longer in ELE? I think ELE is a great long term investment on both gold and copper. Could you share your view on the company?

English

To bring more attention to this great list I thought I'd give my off the cuff thoughts on each.

$WPM - the more silver leaning of the big 4.

$FNV - the 🐐, not cheap but upside if Cobre Panama reopens. I have a position.

$RGLD - most development upside of the big 4. I have a position

$OR - Not a long enough track record of being run by adults but arguably should be part of the big 5 now that it is.

$TFPM.TO - I put them in the big 4.

$SII - really an asset management company

$ELE - The new mid-tier.

$DRR.AX - reasonably priced on MAC iron royalty & Thacker Pass lithium upside. I have a position.

$ALS.TO - top tier management but every time I run the asset valuation I decide the stock is already fairly valued.

$LIF.TO - I think the premium for high grade iron over low grade iron continues to widen over time. Still I think it's already fairly valued.

$GROY - Management looks ready to sell but there's a risk management won't sell and instead will do things.

$VMET.TO - Could get a boost from a US listing and/or $GDXJ inclusion. Tether and Lundin investment could lead to merger with $ELE or $LUNR.V . CEO took Maverix to an acquisition exit. Assets are just OK, this would be a bet on the team and capital markets approach.

$LUNR.V - A royalty on a special project but present value discounted really depends on development timeline. Real bet here is that the Lundins have given hints this vehicle will be active and doing more deals. On my shortlist.

$MTA - On my shortlist. Legit mid-tier with a good growth portfolio.

$UROY - Amir Adnani is chair of the board. It's buying physical. Not for me.

$QRC.TO - Convertible notes have good protection and upside potential, though different from royalties. Management had really done a great job. I have a small position and wouldn't mind adding on a pullback.

$LIRC.TO - Being acquired by Altius. I had a position that I exited after the offer.

$VOXR - Not for me.

$GLDG - Amir Adnani and David Garofalo. Not for me.

$DC-A.TO - On my shortlist. Mining private equity fund basically.

$VROY.V - If you buy a single asset royalty company it helps if you like the asset, I'm not in love.

$RHI.AX - The play here was the mine start bonus, which has been received and paid out to shareholders. Now remaining is a A$28m / yr royalty in a A$320m market cap company. I'm also not in love with Onslow operationally.

$ECOR.TO - was trading cheap so I bought; Isold after I thought it wasn't cheap anymore.

$FISH.V - Not for me.

$KLD.V - I'm a long term shareholder.

$OGN.V - On my shortlist but the recent runup on a newsletter pick seems unwarranted.

$NRC.V - Not sure how public investors fit alongside the first nations on this one, watching for now.

$EVR.CN - I have a small speculative position.

$SRL - If you own a single asset royalty company you had better like the asset. I'm not in love.

$EMPR.V - They lost most of their dealflow when their partner bank went bankrupt. Now they are fighting to get out of the sub-scale royalty company size doing $3-5m deals without a lot of dealflow or financial backing. I wish them luck but not for me.

$LRA.V - pivoting from project generator to PEA stage developer of a 100% owned project. I have no opinon on the project.

$SUM.V - One to keep an eye on, but not at a point where I'd invest yet.

$GMX.TO - A former position and always on the shortlist to re-enter. Jack fixed the lack of succession problem by bringing in a new President/COO.

$NKL.V - This will tell you how much I hate Nickel. I estimate royalty revenue to enterprise value is 30% and that will increase as they pay down debt and gets a bump when they pay off the debt. Former management got fired for cause May 2024. Potential for one of their other royalties to hit if re-shorting of critical minerals funds one.

$RMCO - new to me

$HWG.CN - on my list to look at

$MD.V - very investible, I've owned in the past but no current position

$MRZ.V - there's some data supporting the Lunahuasi porphyry trending deep and West and what's 3km west? The Sobek North El Potro SE Target. It's a long shot but if you like to gamble I could see buying a lottery ticket. The rest of the company seems pretty stagnant.

$TNR.V - the royalty is worth more than the company thanks to management. Some shareholders are in revolt and may overthrow management.

$SMD.V - setting aside I got burned here when Nickel price collapsed and Broden Mining got stalled I think this is interesting. I haven't updated my spreadsheet since selling but it's common that their market cap is less than the value of stock they own in other companies. Holding costs in the Yukon are low which allows them to maintain a deep pipeline of projects and work them economically efficiently.

$JG.V - on my list to look at

$DEX.V - Had a good thing going in Mexico until that jurisdiction became hostile to mining. Have scrambled to rebuild a pipeline in the US & Canada. Wish them luck but not as an investor.

$SCRI.NE - new to me

$LMS.V - I have a position.

$MUN.V - always on my shortlist

$STRR.V - The Copperstone royalty is worth more than their market cap. But the rest is messy. Not sure what path management will take to try to unlock the value of the melting ice cube.

𝙔∪𝕏²@_Yux__

My updated Royalty/Streamer and Generator overview (with a couple of chosen Investment/holding cos included), from where I choose most of my beta plays, ~40% of my portfolio (depending on cycle period). Thanks for all input from last time I posted.

English

Next on the Tether ladder $MTA.v, $VOXR.to, $VROY.v, $EMPR.v unless they move up. Then it is $OR.

I am guessing there has been contact between Tether and $LUNR.v also.

𝙔∪𝕏²@_Yux__

$VMET.v $RGLD RGLD selling 11.8m shares in VMET to Tether and Lundin Family Trusts for C$8.75 per share for a total of C$206m. Now trading at C$12.26. RGLD to use proceedings to repay debt. resource100.com/dashboard/news…

English

$10 says Tether has already talked to the Lundins about LunR. Merge LunR with Elemental and Versamet and you get an amazing company. $ele.v $vmet.v

Versamet Royalties@vmetroyalties

NEWS RELEASE! Versamet Royalties Welcomes Tether Investments and the Lundin Family as New Cornerstone Shareholders Read more here: tinyurl.com/4zkdxvjr $VMET.V | $VMET

English

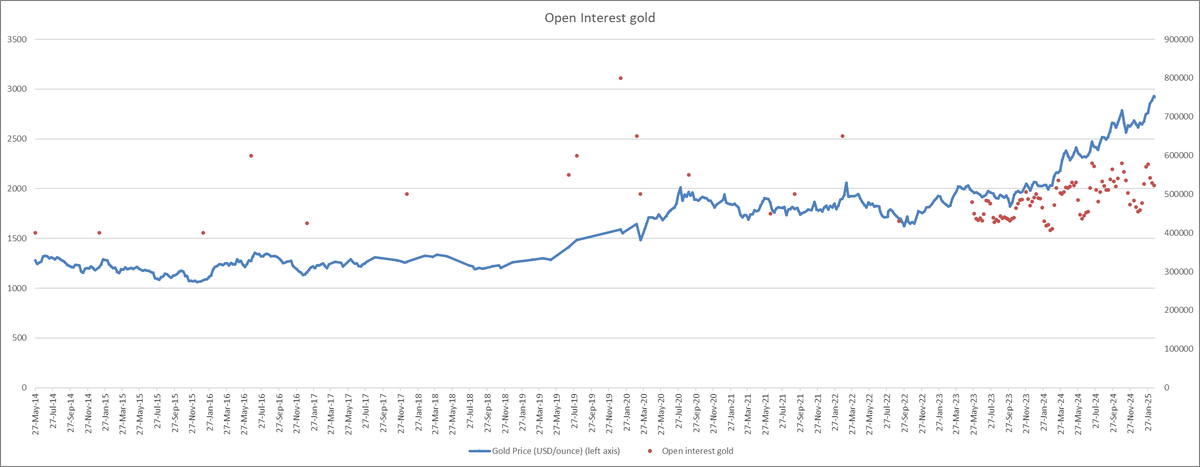

Open interest in gold continues to drop while gold is making new highs. This is extremely bullish and we are ready to rock!

English

@johnjhin7 @johnjhin7 would you say the dollar broke the resistance line and is headed much higher? Or do you still believe that dollar is going down?

It seems to have broken many resistance lines on the way until now.

English