BZ@BZ_crypto1

@Telcoin just crossed the line most crypto projects never do.

(The TLDR version:

Telcoin didn’t launch another token. They finished building a regulated financial stack and are about to turn the network on underneath it. $TEL isn’t a promise anymore. It’s a utility token about to be plugged into real money movement.)

—————

For years, crypto has had three separate worlds that barely talk to each other. You’ve got banks and regulators. You’ve got stablecoins pretending to be dollars. And you’ve got blockchains that move fast but live in regulatory limbo. Telcoin just stitched those three together in a way that’s actually legal in the U.S.

That’s the big deal.

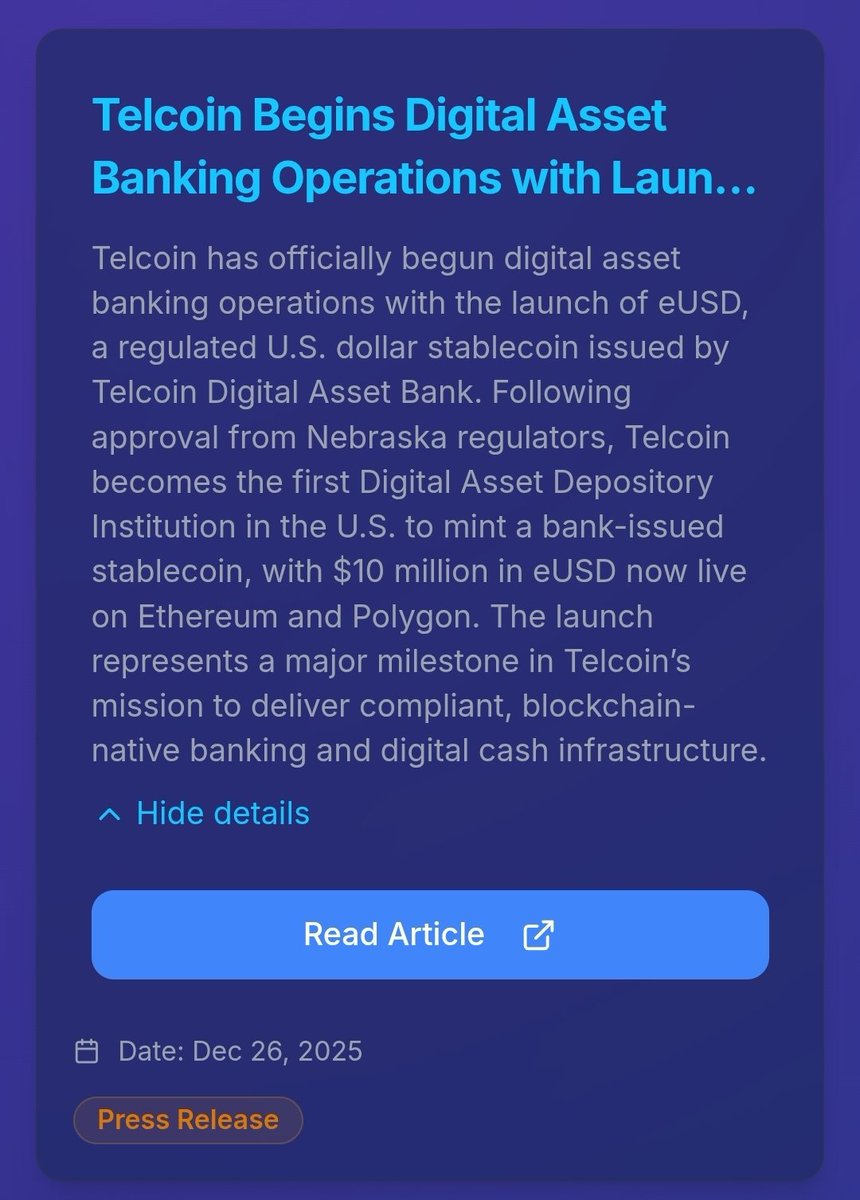

Telcoin now operates a regulated digital asset bank and has issued a real U.S. dollar stablecoin backed by bank-held reserves. Not a “trust us bro” stablecoin. Not an offshore issuer. A regulated, state-chartered bank issuing dollars on-chain.

But most will ask, “why’s that even matter? I’ll just use @USDC”

in plain English: this is how crypto stops being a toy and starts being infrastructure.

Most crypto projects try to bolt usefulness on later. Telcoin did the hard part first. They spent 7 years dealing with regulators, helping draft banking law, compliance, and boring paperwork while everyone else chased memes, KOLs and big marketing budgets.

Now they can legally hold dollars, issue stablecoins, and move value between banks and blockchains without pretending those rules don’t exist.

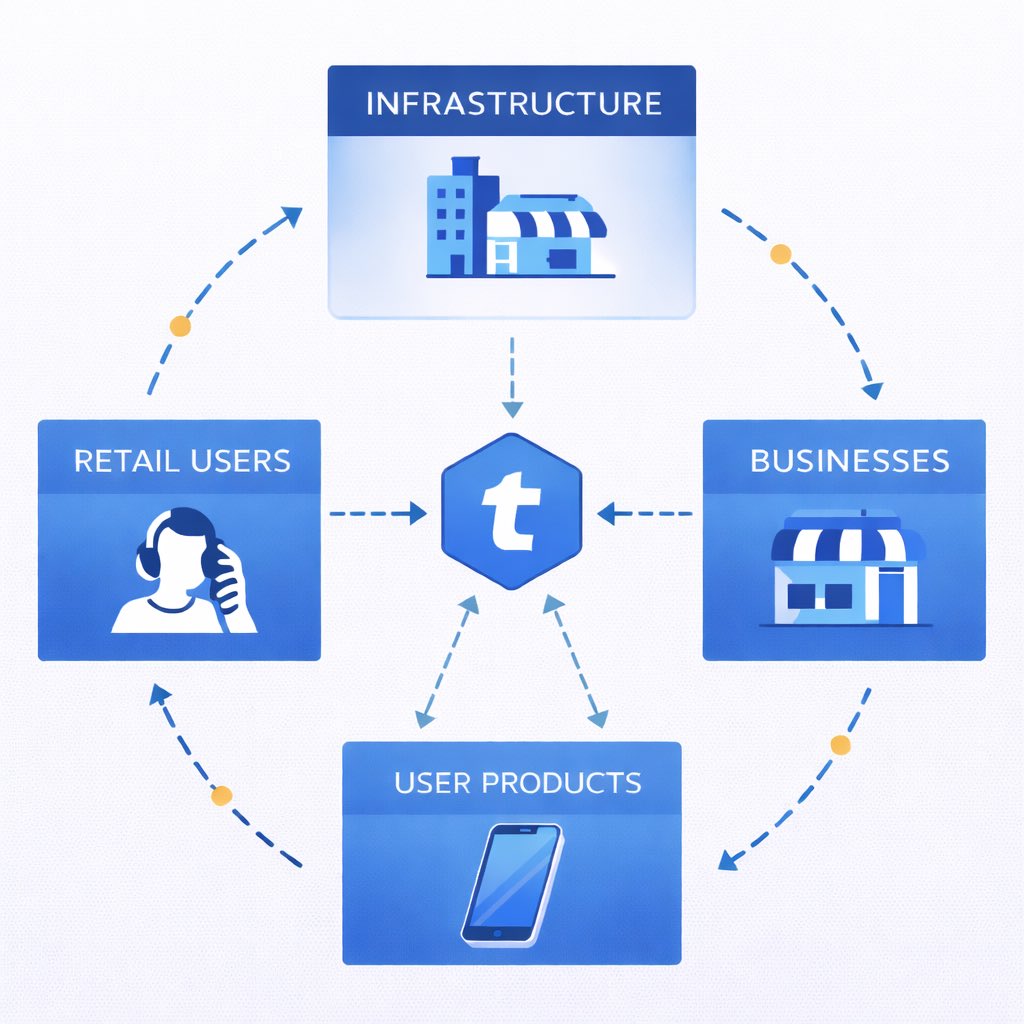

Next comes the missing piece: the L1 evm-compatable Telcoin Network being built

Right now, Telcoin has payments, remittances, and token utility, but the full loop isn’t closed. The network is what turns all of this into a self-contained system. Dollars come in through a regulated bank. Those dollars become stablecoins. Transactions run on Telcoin’s network. Fees are paid in $TEL. Usage drives demand. Demand tightens supply. That’s the flywheel.

This is where most people miss it.

$TEL isn’t competing with meme coins or random L1s. It’s positioned under the rails of real money movement. Every payment, transfer, settlement, or application that runs on the network needs $TEL to function. That’s not narrative demand. That’s mechanical demand.

Think of it like this: If stablecoins are the blood, the bank is the heart, and the network is the circulatory system, then $TEL is the oxygen. You don’t speculate on oxygen. You need it for the system to stay alive.

Right now, the market mostly prices Telcoin like “another crypto token.” That’s because the hardest milestones just finished quietly. Regulators don’t ring bells. Bank charters don’t trend on X. But once users, businesses, and developers actually start using a regulated on-chain dollar inside a purpose-built network, the valuation framework changes. It stops being “what might this be someday” and starts being “how much value flows through this system.”

That’s the inflection point investors look for after the fact.

The risk is execution, not legitimacy. The legality is done. The compliance is done. The bank exists. The stablecoin exists. The remaining question is adoption and scale. If Telcoin executes even moderately well, the upside asymmetry is obvious. If they fail, it won’t be because regulators shut them down. It’ll be because they couldn’t attract users fast enough.

That’s a very different risk profile than most crypto.

People usually notice that part late.