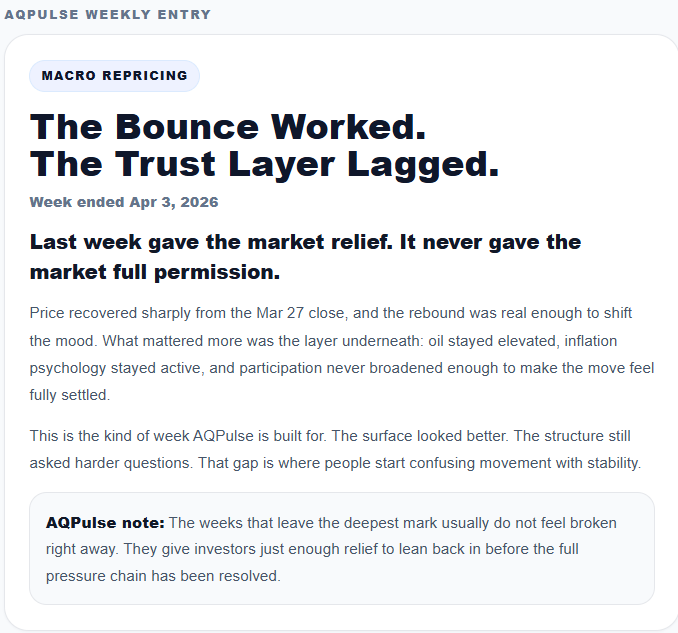

Sabitlenmiş Tweet

AQPulse

2.7K posts

@AQPulse

Stop trading the bounce. AQPulse shows what can actually hold, where risk is building, and when relief is false.

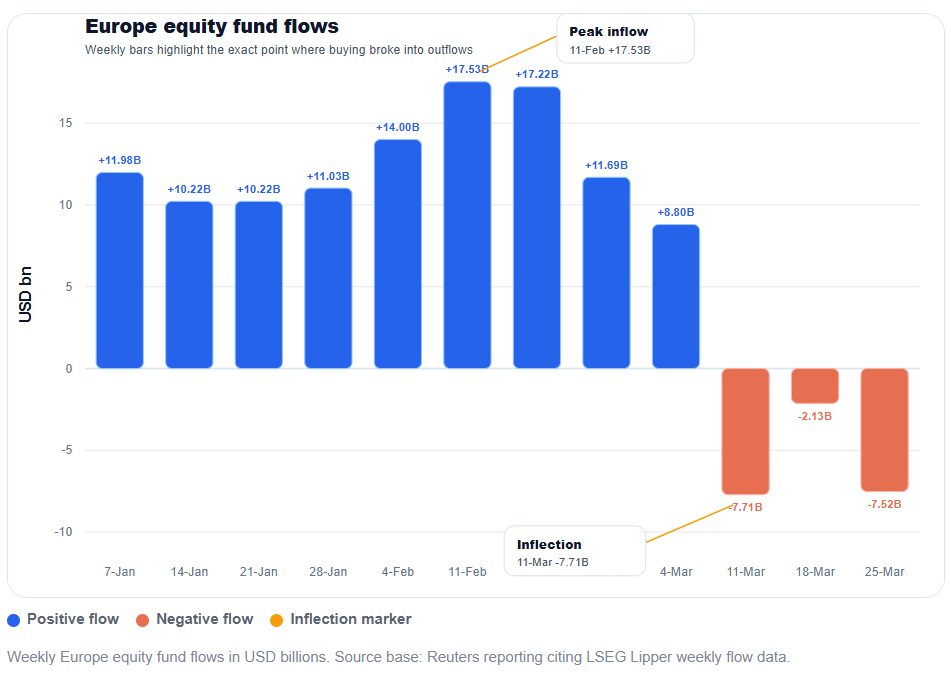

Hedge Funds dumped European Stocks last month at the 3rd fastest pace in a decade 📉📉

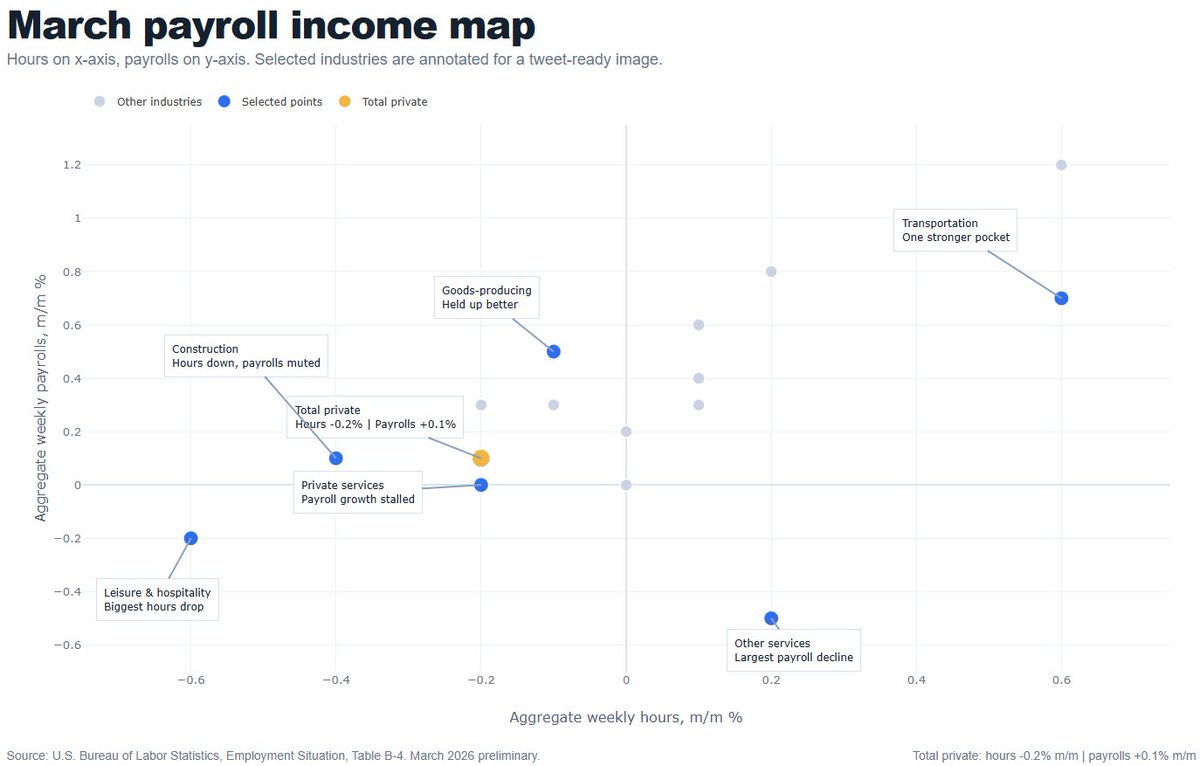

From the March payroll report: INCOMES: A drop in the average workweek in March led to very little growth in the index of aggregate weekly payrolls for private-sector workers (which combines hiring, wages, and hours). The 12-month change ticked down to 3.9%