little fish

1.4K posts

little fish

@AdamMetaverse

Cypherpunk. Investor, not a trader. Digital art collector. Web3. free speech. free economy. building value.

Metaverse Katılım Mart 2022

1.3K Takip Edilen7.3K Takipçiler

$ENLV JUST REPORTED. NET INCOME PROFIT $1.23B, EPS $25. CLINICAL QUALITY LONGEVITY DEVELOPMENT ON ONE SIDE, PREDICTION MARKETS INFRASTRUCTURE ON THE OTHER.

English

Did @Tyga just tweeted about @Rain__Protocol? 👀

T-Raww@Tyga

What’s this rain site about ? You make Predictions and make money ?

English

That's beautiful

Rain@Rain__Protocol

Prediction Market Builders want more - and now, they’re finally getting it. The Rain Builder Program is live, with the first prediction market SDK built for AI agents. We’re moving past the era where "building" just meant skinning someone else's data. Rain is giving you the infrastructure to launch and own your own end-to-end platforms from day one. Our SDK provides the tools and resources to handle the entire lifecycle: public or private market creation, manual or AI Oracle resolution, dispute processes, and more. You aren't just promoting trades anymore - you're running the engine. Specifically for the agent-led future, our SDK is ready for @AnthropicAI Claude Code, @NousResearch Hermes, @OpenClaw, @OpenAI Codex, @ManusAI, and more. It's time to build: rain.one/builders

English

Why machine-to-machine payments are the new electricity for the digital age theravens.ai/article/20

English

@HernanArber @Rain__Protocol @CoinMarketCap What you're missing is that the top 200 on @CoinMarketCap is a closed list and to get in there they will need to list them there.

In terms of market cap rain is probably top 50 but because it's a closed list the odds are low.

English

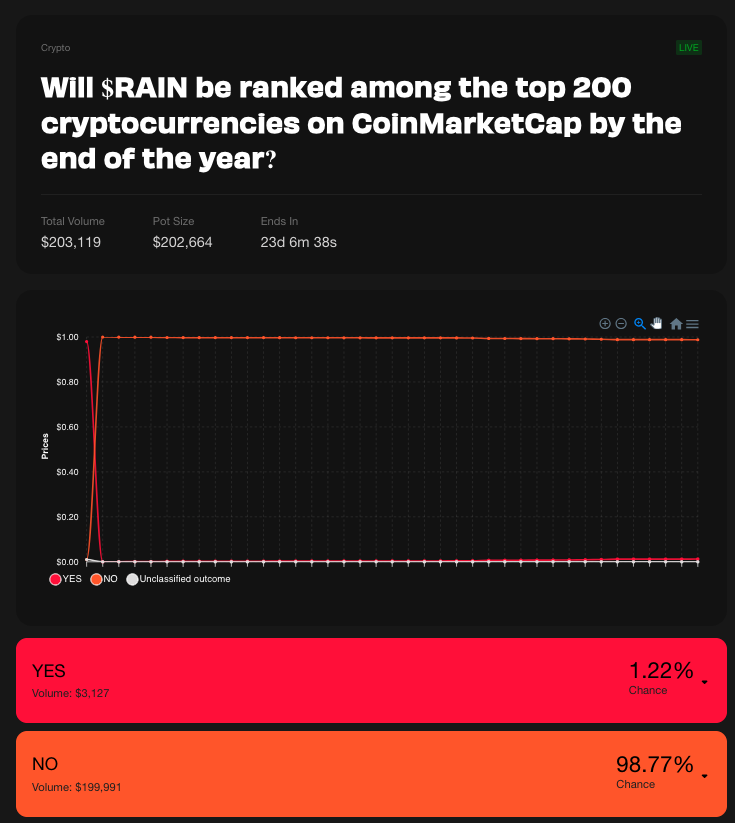

Something is not right...

I just placed a small bet on this @Rain__Protocol Market:

*Will $RAIN be ranked among the top 200 cryptocurrencies on CoinMarketCap by the end of the year?*

$RAIN appears to be at spot #202 on @CoinMarketCap, and yet, NO is at 98.7%, while YES is at 1.22% odds.

That means like a 22x+ Payout if the $Rain pumps 4%-5%

DURING THE WHOLE DECEMBER!!!

So why a small bet? Dunno, it's my 1st time placing a bet on these Markets, and the Whole NO Pool is held by RAIN themselves, so they may manipulate the price (or the result)

But if they are fair and the coin does even a slight jump during the next few days, it's a total no-brainer.

AM I MISSING SOMETHING HERE? Or is noone else paying attention?

NFA, but if you want to make use of this alpha: rain.one/?code=0x10799a…

English

@Rain__Protocol @arbitrum That's not funny any more, I've put money on YES @arbitrum, in 2 days I'm gonna lose my money because you don't follow the biggest project that's on your chain, I really hope it's a joke and you're gonna follow before this market ends!

English

Many in the Rain community have asked a fair question:

“How come @Rain__Protocol is built on @arbitrum, but Arbitrum doesn’t follow Rain on X?”

So we turned the question into a $10,000 incentivized market: Will Arbitrum follow Rain’s X account by December 11, 2025?

Right now, all the money is on NO.

If you think you can move the needle, or just want to ride the upside, the YES side is wide open.

Arbitrum Everywhere? Let’s see.

Join the Market ⬇️

English

little fish retweetledi

JUST IN: $ENLV ANNOUNCES A $212M DIGITAL ASSET TREASURY ALLOCATION INTO $RAIN, THE PREDICTION MARKETS PROTOCOL. FORMER ITALIAN PM @MATTEORENZI JOINS THE BOARD.

English

If you think that in 3 years $BTC all time high would still be $126K you're stupid.

Buy the dip.

English

little fish retweetledi

Polymarket changed the game for prediction markets, but its data now rivals traditional polls for speed and accuracy.

This is what @Rain__Protocol is built for, a fully decentralized prediction platform on Arbitrum.

Unique Key Features:

✅ Create Markets on Anything – Build prediction markets on any topic, whether public or private, in any language and from anywhere.

✅ Private Market Access – You can use access codes to create exclusive markets, ideal for discreet or niche communities.

✅ Powered by Arbitrum – It has fast, low-cost, and scalable transactions.

✅ Fair Commission System – 5% of each settled market is shared among creators, liquidity providers, and a burn mechanism to support the ecosystem and control token supply.

Rain Protocol combines freedom, simplicity, and sustainability, making it a promising platform for the future of decentralized prediction markets.

We have a marketing partnership with Rain so please do your own research.

English

little fish retweetledi

@scottmelker It's actually the only protocol in the space, anyone can create a market about anything

English

New prediction market just dropped.

Rain@Rain__Protocol

Will Rain’s official X account have OVER 250,000 followers on November 30 at 2 PM UTC? We put $20,000 on “under” - not out of doubt, but to give YOU a reason to prove us wrong! If @Rain__Protocol hits 250K on X, the $20,000 will be yours. Incentives > Motivation. Think you can turn this “UNDER” into an “OVER”? Join the market ⬇️ preview.rain.one/share/market/?…

English

little fish retweetledi

Now tracking @Rain__Protocol on @arbitrum

Decentralized Prediction markets protocol on Arbitrum

English

little fish retweetledi

JUST IN: 🇺🇸 President Trump tells reporter "you don't know much about crypto…you know nothing about nothing, you're fake news."

English

Amazing entry point! Let's go shopping.

Watcher.Guru@WatcherGuru

JUST IN: $250,000,000,000 wiped out from the crypto market cap today.

English

little fish retweetledi

It’s $RAINing in MEXC.

The first drops meet the market. $RAIN is now live on @MEXC_Official, flowing into one of the world’s top exchanges.

Every trade writes the next line of the storm.

Start here: mexc.com/exchange/RAIN_…

English