dreamon.eth

651 posts

. @blackhaven shipped the marketing before they shipped the product.

Classic Web3 move … sell the safety net, build it later.

Eli5DeFi@Eli5defi

Just saw that many people seems doesn't really understand on how @blackhaven works and operate. → BAM (Backing Arbitrage Module) is planned and may not be live at launch. → Until BAM is on, RBT can trade away from NAV with no automatic correction. Genesis trading = higher peg risk. Size positions accordingly. → Once BAM is live, NAV becomes an active anchor (mechanical floor/ceiling). Until then, it’s just a reference. Two prices exist at once - NAV: reserves ÷ circulating RBT (on-chain). “Collateral value.” - Market price: what the RBT-USDm pool trades at. They won’t usually match. BAM’s job is to shrink the gap. NAV moves only when reserves or supply change; market price moves with trades. - ➠ When Market Price > NAV (premium): - BAM sells RBT into the market. - USDm from sales goes to reserves → NAV rises. - Selling pressure pushes price down toward NAV. - Bigger premium → bigger action (with cooldowns). Net effect: the protocol issues into a premium, strengthens backing, and compresses the spread (expansion). - ➠ When Market Price < NAV (discount) - BAM buys RBT with reserves and burns it. - Reserves drop, but supply drops faster → NAV per token rises. - Buy pressure pushes price up toward NAV. Net effect: buying below NAV is accretive to remaining holders (contraction). ➠ How NAV can grow without BAM Reserves also grow from: - Bond issuance (90% of each USDm bond to backing) - Returns from whitelisted MegaETH DeFi strategies - MegaETH points + retained MEGA - Forfeitures (early-exit fees, forfeited distributions/unvested RBT) - BAM proceeds during premium sells Most of these add reserves without increasing circulating supply. - There are many @megaeth users dissatisfied with Blackhaven’s approach, especially since it’s live on Mega Terminal. The core issue, though, was transparency and communication. Many felt the marketing framed it as stable/reserve-backed while key safeguards weren’t in place (BAM isn’t live yet). The bonding UX and disclosures also seemed too implicit. Users saw bond discounts and the market price, but the “backed price”/NAV wasn’t obvious or clearly surfaced. Some didn’t realize they were buying into an already-live DEX token that had been front-run, or that after the lock period they’d receive RBT (not the stable USDm). The 10% fee was also widely criticized as greedy. This resulted in massive instant losses for early bonders and buyers who expected a “reserve-backed” product to hold its value.

English

dreamon.eth retweetledi

The thing AI will never fake is a human who stood in the desert and felt time slow down.

Gift of Time by @ManuelLarino isn't generated. It's remembered. 🤍

English

dreamon.eth retweetledi

dreamon.eth retweetledi

@Simon_Ingari “We chose someone better suited to our needs.”

Translation: “Someone who can be underpaid quietly.” 😭

English

dreamon.eth retweetledi

@fatiieenotfatty She said ‘let me help’… he said ‘help by stopping’ 😂

English

If you've never experienced second hand embarrassment, read this🤣. So this girl went to her bf house for the first time. She slept over, fast-forward to the morning she wanted to wash the plates they used the previous night. She noticed the morning fresh liquid soap was half way

English

dreamon.eth retweetledi

dreamon.eth retweetledi

One man can impregnate 9 women everyday for nine months. Those will be 2,430 pregnancies. A woman can only get pregnant once within nine months, even if she sleeps w 9 men everyday within 9 months. so, birth control should be for MEN, Science is busy making pills, and birth control for the WRONG PERSON.

English

🚨Caroline Ellison was released from jail today after serving 440 days, or 60%, of her 2 year sentence.

She pled guilty to fraud & conspiracy charges in 2022 following the FTX collapse.

Now that she's out, she has a 10-year ban on leading any public company or crypto exchange.

English

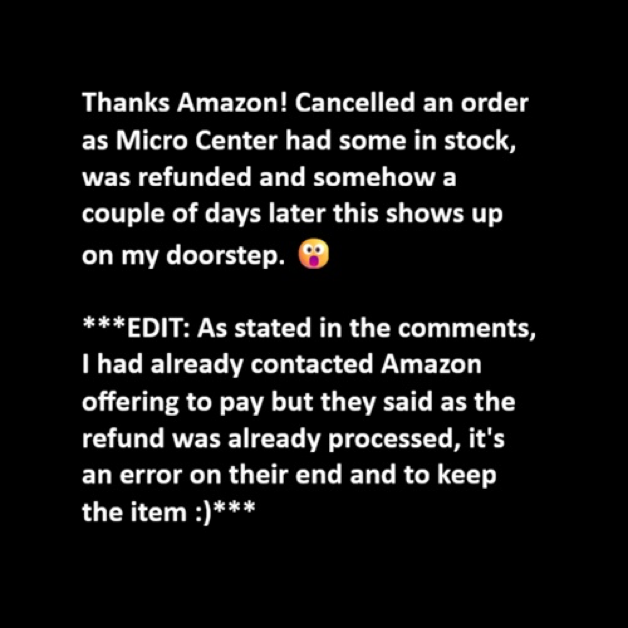

A Redditor canceled their order for an ASUS ROG Astral RTX 5080 (White edition) on Amazon, got fully refunded, and then the $1,850 GPU still showed up at their door anyway.

When they reached out to Amazon offering to pay for it or return it, the company told them to just keep it, blaming the mix-up on their own system error.

English

@0xSunSeeker @Pirat_Nation i thought I was VIP when i tried to return a 7 dollar cable and they told me to keep it. damn

English

dreamon.eth retweetledi

dreamon.eth retweetledi

Can you suggest a baby boy name that sounds like he comes from an ultra-wealthy family ??

English

dreamon.eth retweetledi

dreamon.eth retweetledi