Andrés González

9.8K posts

@Broasted_King @KobeKapital Lmfao that guy is regarded thinking it’s a “pump and dump” or there’s a leak.

They can point fingers all they want, somehow people in Europe are extremely salty for no reason.

Especially when they don’t understand how hyperscaler supply chains work.

English

Holy crap $SOI.

$AXTI went up 30% yesterday too.

Substrates to brrr?

Serenity@aleabitoreddit

Wow $SOI is now the 16th name... I've done a mininthesis post on that returned over 100% Year to Date. The most recent two were $ALRIB and $RPI. Why does everything around me keep doubling?

English

It’s just that the world wanted me to reach 1000% unrealized gains on $AXTI.

My most legendary thesis to date.

Jos@Jos1984482

@aleabitoreddit Anything explaining axti's 20% jump?

English

@aleabitoreddit @RayBraha The vote didn't happen on the 14th? I closed everything before then fearing the result

English

@aleabitoreddit @Investmnt_Eagle Wasn't the vote on the 14th?

English

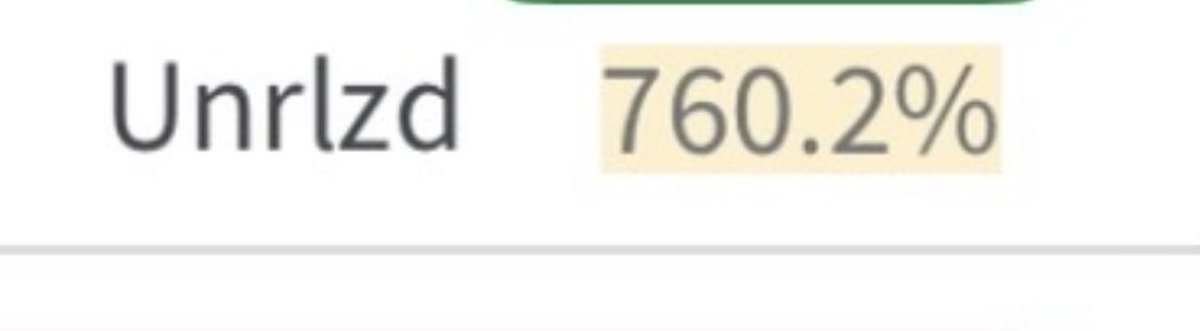

@Investmnt_Eagle I’m just sitting on a small 720% unrealized gain on $AXTI.

Wanted 1000% so just holding personally. We’ll see how the shareholder vote turns out

English

My $IQE call… might actually outperform my legendary $AXTI thesis soon?

It’s only been 2 months:

Now it's up over +316% after institutions started publicly buying… and keeps going up.

Fun time for critical chokepoints like $ALRIB, $SIVE, and $SOI recently in Europe.

Probably expect them all to compound another triple digits from here, even after all their rallies.

Retail is just extremely early for the first time.

So, expect a lot of institutional capital to pour into these critical supply chains companies soon, especially $SIVE after Nasdaq listing.

Serenity@aleabitoreddit

Not exactly! I'm just a tad more familiar with photonic supply chains than I am with energy so I like picking potential winners. Just wanted to introduce $IQE into the equation like i did with $AXTI, so I could do a "Did you Listen Anon?" post 3 months later if it turns out well.

English

@aleabitoreddit Wasn't this the case with AXTI too up until recently? Wouldn't call it sleeping too well haha

English

The nice thing about multi-year bottlenecks from:

$HPS.A to $SNDK to $LITE

Is that you can sleep a easier despite market volatility like today.

Knowing demand will be extreme even 1 year...

Even if Trump wants to nuke Bikini Bottom and other companies might be more impacted:

-> One has a huge market share over Transformers

-> One has huge market share over NAND

-> One has huge market share over EML/OCS.

And the one thing in common is that they're all likely backlogged on orders into 2028.

Signaling near-guaranteed fundamental revenue and likely margin expansion into the next year.

It's H1 2026 now.

English

@aleabitoreddit Why is AXTI on a free fall? Did something fundamentally change?

English

Not really late too the party, it’s extremely early and at the beginning of the next inflection point.

I personally like $SIVE, $AEHR if I had to pick two more smaller purer play companies around now, maybe throw in $AAOI on the next drop.

For safer, Win, $SOI, $MRVL seem solid?

Quite a lot of names…

English

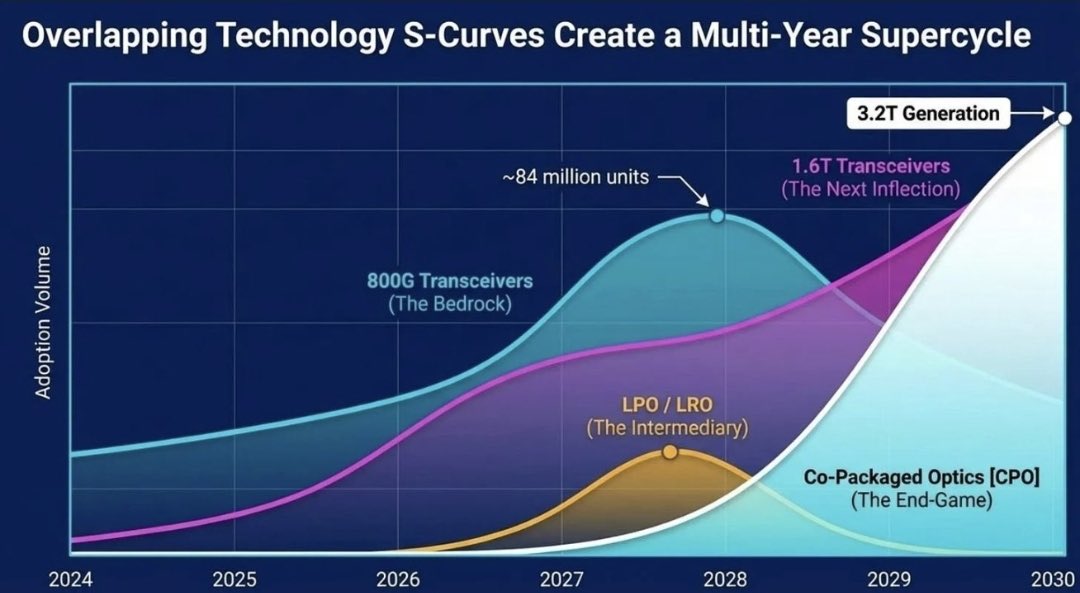

Please stop trying to model 2025-2026 revenue for future CPO/SiPH ramp…

When I looked at $TSEM back at ~$115 last month (round to $200 now).

The forward p/e compressed to rates like ~16-18 (down to 10-12 in growth scenarios)

Same applies to $AEHR / $SIVE / $SOI /Win Semi and other names.

This is H1 2026. Volume ramp hits H2 2026.

We’re at the very beginning of a massive supercycle and these are my more pure play exposure picks for the next architectural changes in photonics:

For testing, cw lasers, substrates, and foundries in next paradigm shift in the photonics supercycle.

Companies like $LITE or $AAOI that I’ve longed last year cover multiple cycles.

However, the most returns comes from anticipating what benefits the most Mc wise relative to future revenue/TAM growth (not priced into current earnings).

Not looking back at 2 year historical returns to calculate fair value.

And when we’re looking at massive new photonics TAM ($110B+ bull case from lightcounting), largely driven from architecture that use CW lasers as an example or struggle with yields.

A lot of these companies are likely going to re-rate hard.

Especially when you look at the start of the next architectural changes, happening around H2 2026.

English

@aleabitoreddit @ram_blings Are you still long on $U and $RPI?

English

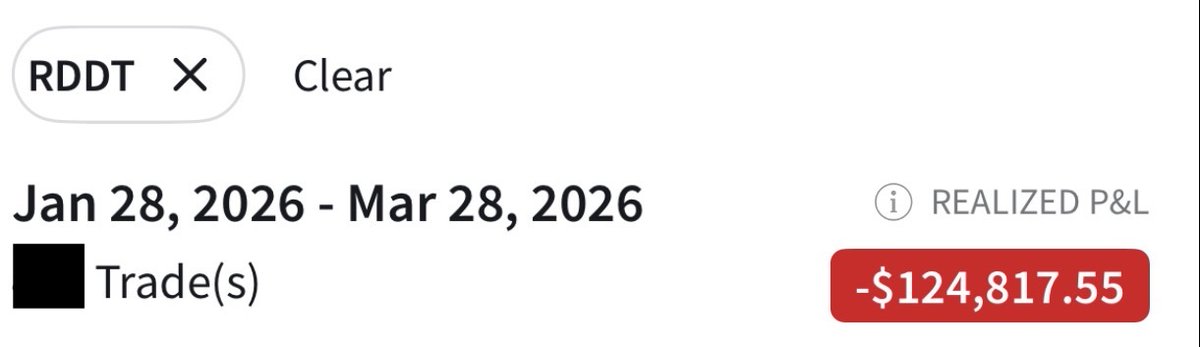

@ram_blings I've trimmed concentrations here and there, but remain long overall. This is $RDDT for example, but I did buy more at $125.

English

I don’t post USD values of positions from $RDDT to $CRCL since they’re irrelevant.

What matters are the core thesis/ideas:

The % outcome in the market validates them, not the size of a portfolio and USD values going up a lot (like .01% of $10M).

I’ve said this before as well to any small X content creator who gets made fun of because of a $5K port or $25K port.

They should be listened to as well for their ideas, not how much money they have.

It’s the same reason I don’t cite my background in RISC-V to publishing papers in AI Labs when I post a thesis:

They’re based on the core idea.

Not authority.

All the endless noise ended up getting to my head so I gave in once posting $SIVE figures.

Substance is what matters and I think that’s largely why my account got such a huge following recently.

And I encourage others to focus on that as well.

Serenity@aleabitoreddit

I just bought ~.5%-1% of $SIVE as a company. I said their future CW laser chokepoint is grossly mispriced. And I put my money where my mouth is. Especially when they're the confirmed light source for Jabil, $MRVL Celestial, O-Net, and other hyperscalers.

English

@aleabitoreddit From the names you've mentioned, would you rotate out of $VLN, $DPRO, $RPI or $U?

English

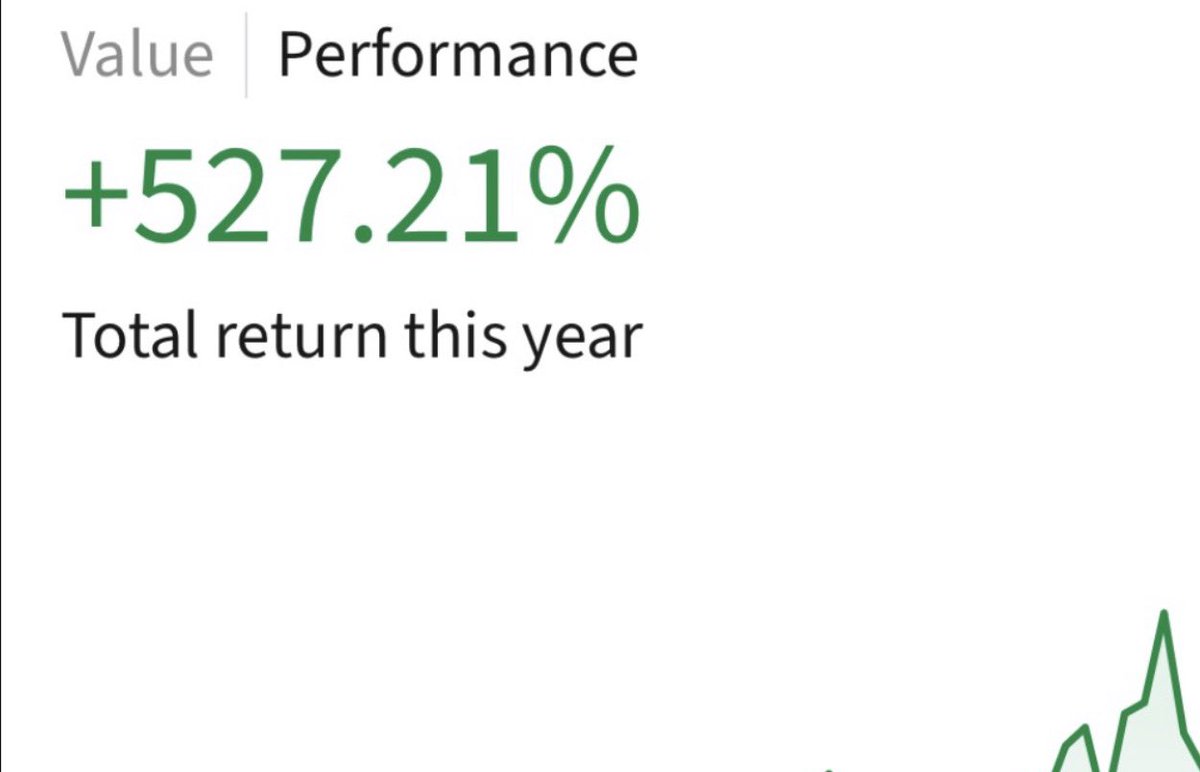

My portfolio has drawdowns from Macro as well.

YTD is now 527%.

After the index crashed -7%.

- $AAOI “crashed” from $30 -> $100 -> $96…

- $LITE “crashed” from $330-> $800 -> $702…

- $AXTI “crashed” from $15 -> $70 -> $60…

I’m not underestimating the War in Iran.

This has serious consequences to liquidity/energy, so I’ve winded down margin.

But if a company is going from $134m quarterly revenue to projected $1.54B a quarter from Made in America optical transceiver ramps...

or if the tiny $3.6B company owns the materials supply chain for the hyperscaler photonics buildout...

or a tiny laser supplier at $290m in $SIVE feeds to $MRVL CPO programs or Jabil transcivers...

or a optical giant like $LITE is sold out of EML capacity until 2028...

or a small European company in $SOI provides all the substrates required for silicon photonics / CPO.

or a small European company in $IQE has latent reactor capacity multiple times what their valued at…

or a memory company like SK Hynix is projected to make more than what their current market cap is in 3 years…

There’s going to be tons of volatility on the way up, as markets realize their importance to supply chains

But if you can’t bypass them to scale AI. Or they’re designed into the supply chains of $AMZN or $MSFT.

Maybe they tend to outperform the market?

English

@aleabitoreddit Terrific call. It was my first UK stock and I didn't know GBp was a thing and I just noticed I bought at 15 one hundredth of what I had actually intended to buy 💀

English

And… $IQE turned out well.

This like my 6th photonics long that returned triple digits?

Serenity@aleabitoreddit

Not exactly! I'm just a tad more familiar with photonic supply chains than I am with energy so I like picking potential winners. Just wanted to introduce $IQE into the equation like i did with $AXTI, so I could do a "Did you Listen Anon?" post 3 months later if it turns out well.

English

@aleabitoreddit Do you think the downwards pressure from the ATM has ended?

English

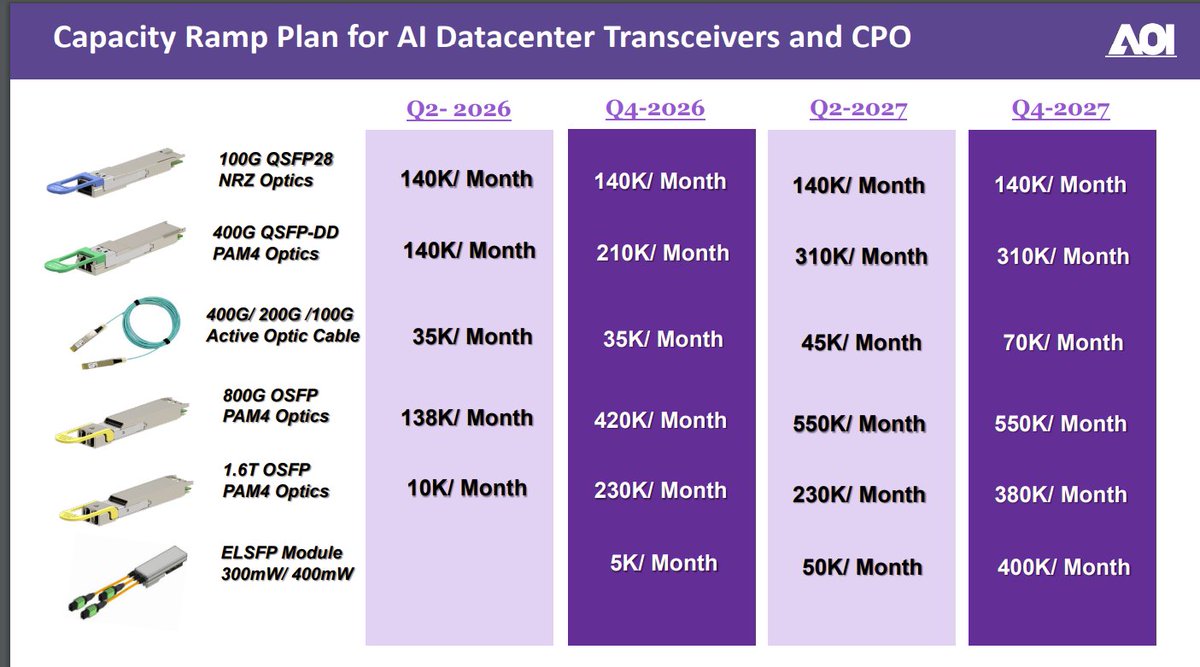

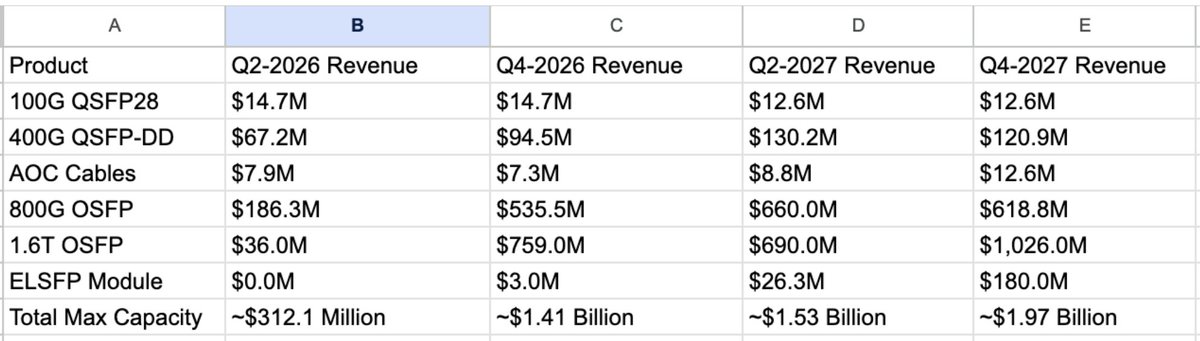

$AAOI looks very undervalued at $6.49B.

If we model ASP and their newest capacity projections today:

Revenue from Capacity:

Q2 2026: ~$312.1M

Q4 2026: ~$1.41B

Q2-2027: ~$1.53B

Q4-2027: ~$1.97B

This is absurd ramp (off ~34-40% est. gross margins).

ASP modeled off (LightCounting, Dell'Oro Group & Yole, pricing for ELSFP modules is the most speculative). And some sell-side models (from firms like Raymond James, B. Riley, Northland Capital, and Goldman Sachs).

Exact contract pricing for massive volume orders is not known, so this is speculative.

But the Q2 volume * ASP estimates actually align with their $378M/month target Q2-2027.

Again, you might be wondering? This is capacity, doesn't translate into revenue right?

Hyperscalers from $AMZN to $MSFT are buying any capacity any of these companies from $LITE to $COHR can make, years out.

This includes $AAOI from their former earnings call.

English

@aleabitoreddit Would you enter here either with shares or calls, or wait?

English

@theburiedcity $AAOI is diluting $250m and selling around the $100 mark.

The last ATM got absorbed extremely quickly.

Probably going to have some resistance around that level until the ATM gets filled up. Then if they stop diluting… sky is the limit depending on execution imo

English

Just looked outside my little bubble.

Majority of folks on X are:

- posting deep red portfolios.

- doomposting 1W charts

- fearing about oil

Feels like most of my individuals stock 1W returns are way in the green?

$AXTI up +46.9%

$SOI up +48.59%

$NBIS up +29.59%

$IQE up +27.92%

$TSEM up +13.99%

And so on… maybe luck?

English

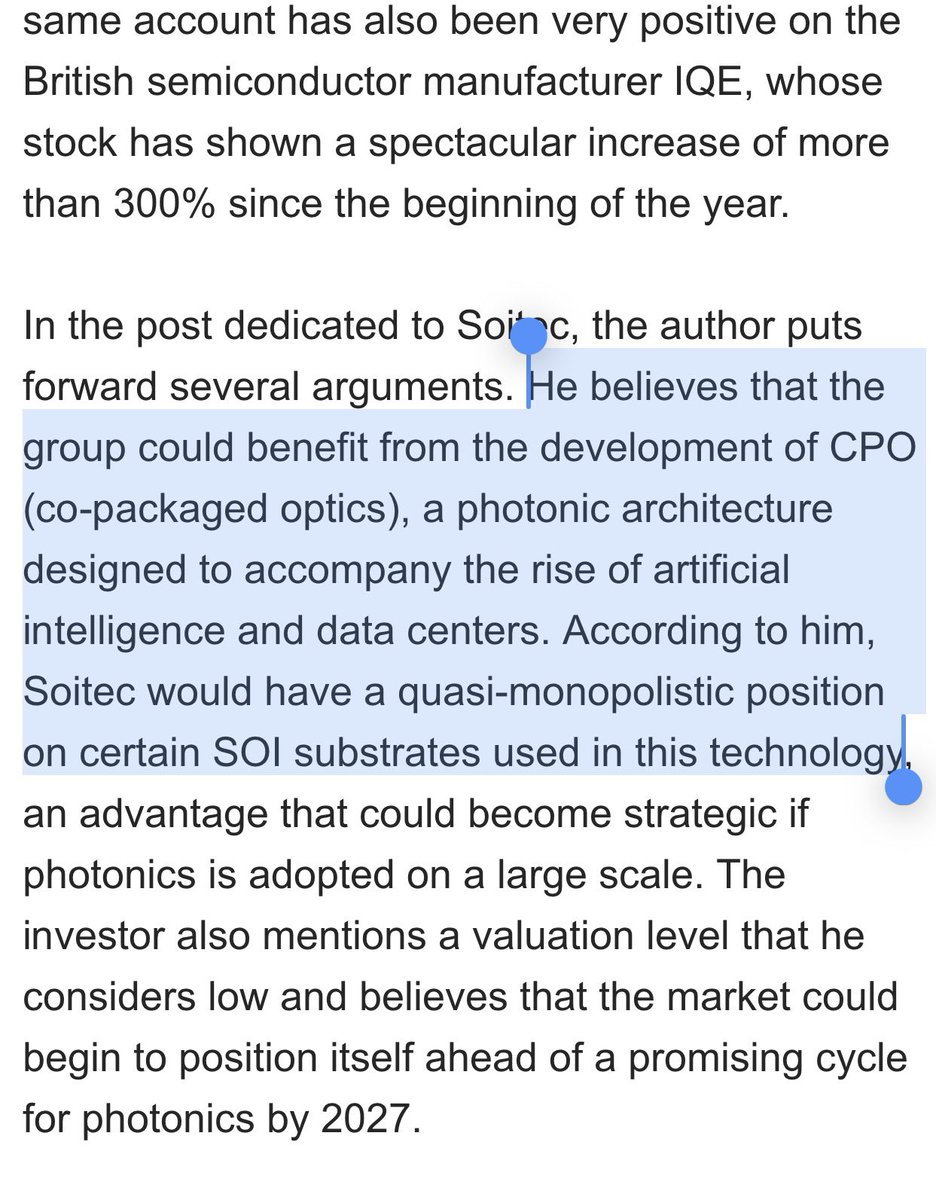

Thank you MarketScreener for actual coverage of $SOI this time.

The article writes:

“In the post dedicated to Soitec, the author puts forward several arguments.

He believes that the group could benefit from the development of CPO (co-packaged optics), a photonic architecture designed to accompany the rise of artificial intelligence and data centers.

According to him, Soitec would have a quasi-monopolistic position on certain SOI substrates used in this technology, an advantage that could become strategic if photonics is adopted on a large scale.

The investor also mentions a valuation level that he considers low and believes that the market could begin to position itself ahead of a promising cycle for photonics by 2027”

This was exactly the thesis, no extra fluff.

Last time media from FT and Bloomberg covered my thesis on $RPI, they labeled it a “meme-stock” out of nowhere. With many outlets straight up adding words never stated, which triggered negative sentiment.

That being said:

$SOI is a virtual monopoly over the substrate layer for CPO.

I plan to hold my positions over the next year or two, as I expect it to be the largest beneficiary of the upcoming architectural ramp spearheaded by $NVDA.

Serenity@aleabitoreddit

Changed my mind about Soitec ( $SLOIF ) and took a sizable position ~43 for CPO exposure. $NVDA GTC next week biggest catalyst pushing photonics and this architecture. ~1.5B euros MC. Trading at 1x book value and ~2x P/S (very depressed valuations) Genuine monopoly over substrates side for CPO (typically very premium valuations for photonics + even extra premium for monopoly status) Algos and analysts might get confused over market share but it’s an actual monopoly over SOI substrates since they give licenses to other players like Shin Etsu for diversification sake eg. $TSM doesn’t like just 1. I don’t think institutions will wait until next year to frontrun these names like Soitec or $TSEM (and most probably haven’t even heard of these names like $AXTI yet) This timing would be buying the likely bottom of the depressed smartphone cycle, while getting full upside of CPO mid-late 2027 + $NVDA GTC catalyst next week. I personally think it’s a 3x from here so I went long.

English

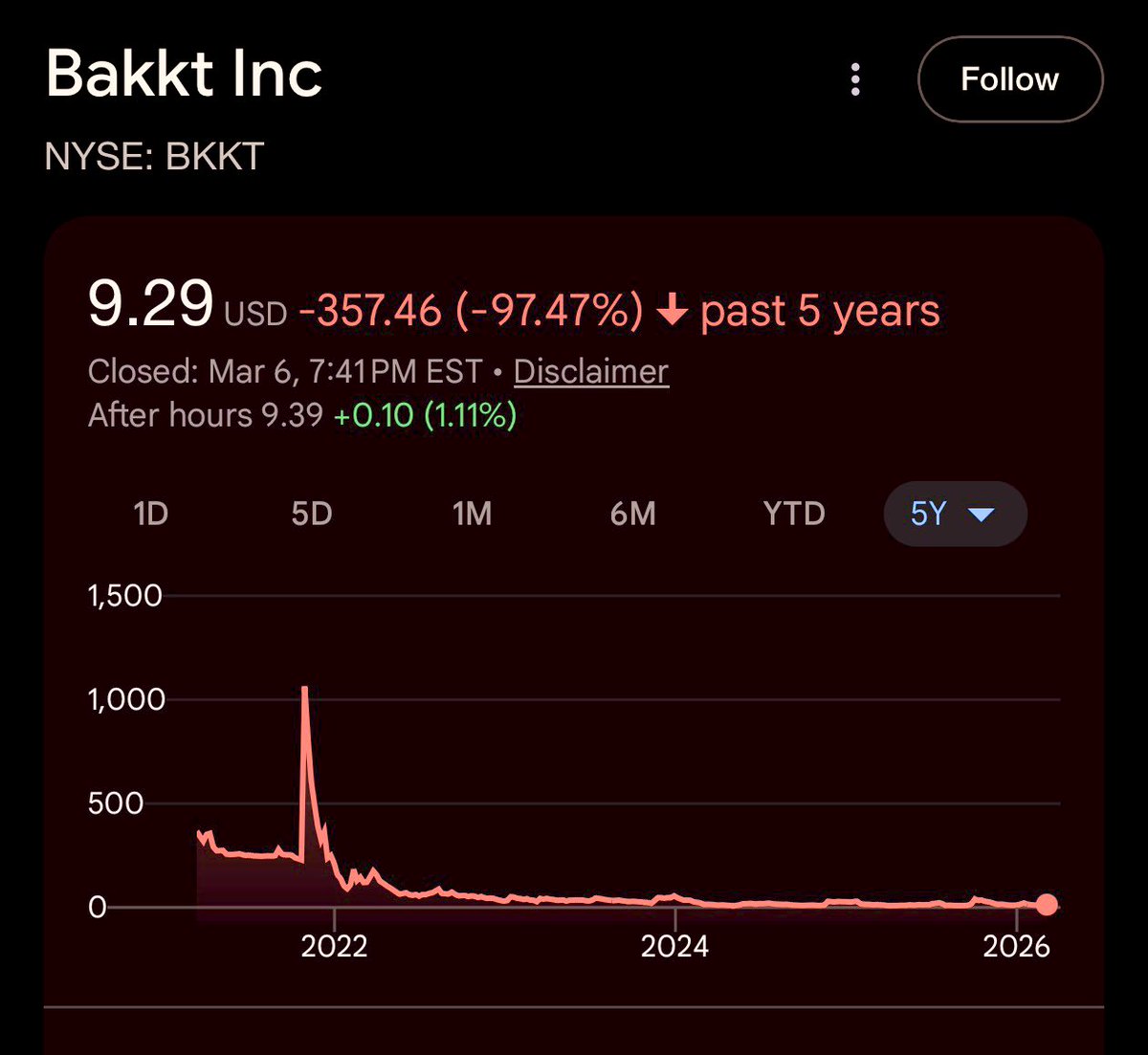

The primary argument for Iren’s $6B dilution was:

“Trust in $IREN management with managing dilution.”

If you look at the actual history of IREN management with:

$BKKT and $ASST.

Both companies have completely obliterated shareholder value from

ATM dilution.

Dropping all original retail share value down by 98-99%.

Companies like Bakkt have been doing okay.

But both stock based compensation to executives + dilution wiped out all equity value from retail.

If a company files for $6 Billion in ATM dilution, you should expect them to use it and position accordingly.

Maybe $IREN turns out differently.

But saying “Trust in Management” then looking at the track record of management of hype retail stocks -> ATM dilution wiping out all value has happened multiple times.

The company will likely end up fine don’t conflate that with the performance of your shares.

I care the most about retail shareholders over corporate executives, which is why I’m sharing the red flag about $IREN $6B ATM.

Serenity@aleabitoreddit

$IREN $6 Billion ATM is massive. For the people who hold $IREN, the truth you might not want to hear is: -> Wait until existing holders get diluted to oblivion -> Use them to "buy the dip" of $6 Billion in new shares for you. -> Go long after. If you're long now: That inevitable $6B in new shares + selling pressure structurally caps upside in your equity and serves as a overhang in any rally. Companies don’t file a $6B ATM not to use it. They will, and as much as they can on any rally. The reality is that there are other financing methods, but ATMs are the most destructive ones to retail shareholders. $IREN itself is a solid company unlike movie theater stocks, but like excessive dilution referenced: You will likely see the marketcap of $IREN go up back toward $20B, but the your share prices tanking in value. TLDR: The harsh reality is $IREN might fundamentally succeed and build a massive DC footprint. But it's at the cost of heavily diluting retail shareholders. Retail investors should care more about the value of their own stock increasing over the company's value. Disclosure: I have zero economic interest or positions in the company, but I do care about prioritizing retail interest.

English

@BrokeDadCapital Sure, I do see Space as probably the next big catalyst play, and now is probably best time to frontrun since it's only 3M from now.

I know there were some people a fan of stuff like $VELO for printers, but financials gets really complex for a lot of these companies.

English

SpaceX to be valued at $1.75T ahead of June IPO (3M from now).

Having a weird feeling all your space stocks from $RKLB to $ASTS are going to be parabolic around the time of IPO day.

Especially when everyone see SpaceX's next biggest competitor in Rocketlab valued at 2.3% of SpaceX's valuation.

English

@aleabitoreddit Congrats!! You should have a copy trading option somewhere haha!

English

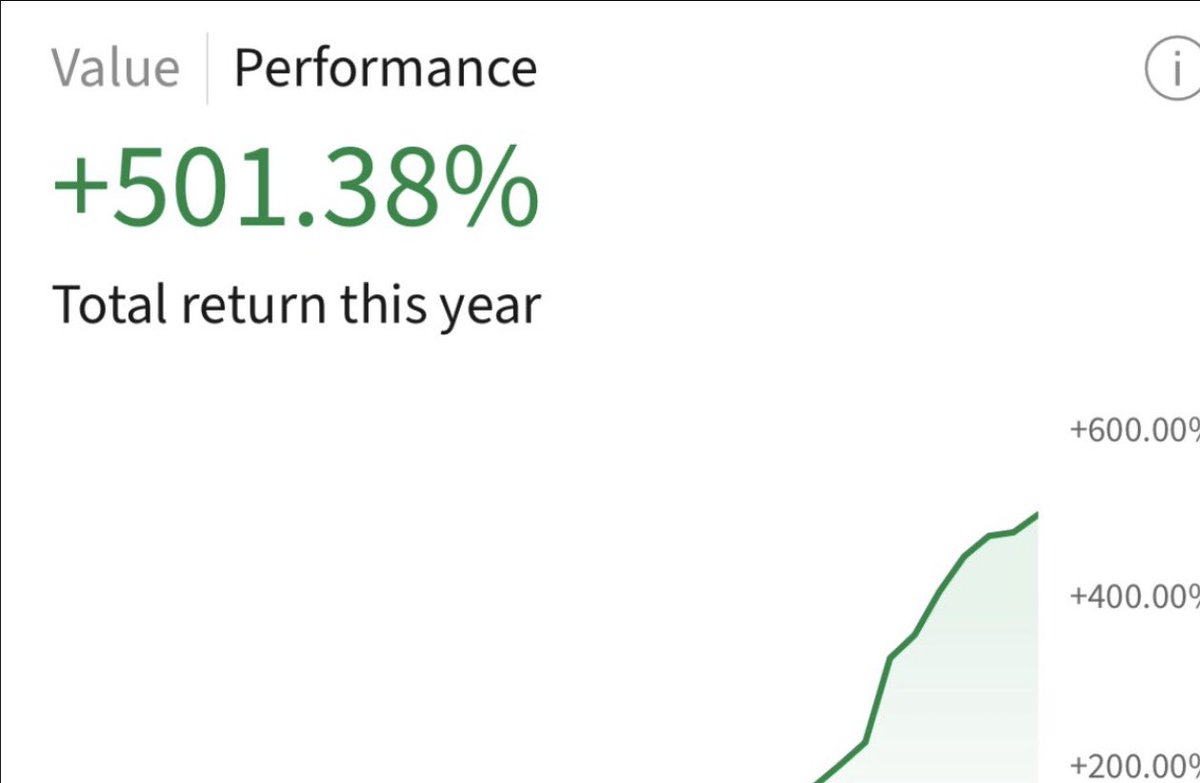

I happened to own every single top individual stock performer this year:

From $AXTI and $AAOI in photonics.

To $SNDK and SK Hynix in memory.

To Nittobo, Macronix, and Unimicron for Asia Bottlenecks.

All triple digit returns in 2 months.

Year to Date: 501.38%

Just lucky I guess?

English

@aleabitoreddit That's insane! Do you mostly do stocks or options?

English

Year to Date: 412.72%

Lot of it is just picking the right sector, profiting off of Jane Street algos weekly, and a bit of luck.

In terms of bottleneck longs, these are currently my favorite:

1. Memory - Samsung, Sk Hynix, $SNDK, $MU, $SIMO

2. Photonics - $LITE, $COHR, $AAOI, $AXTI, (maybe Yamamura too, but not to the same degree).

3. Power/Grid - $XLU.

4. Advanced Packaging Capex - $AMKR, $ONTO, $CAMT, $KLIC, and $FORM.

I’ve talked about all of these before aside from maybe $KLIC?

But most if not all are up like 50-100%+ in a short timeframe, which amplifies overall returns from trading.

Best lesson I’ve learned this year was to rotate where the money flows and current bottlenecks. Rather than attempting contrarian turnaround plays in sectors like cybersecurity.

I publish all my ideas for free too so hopefully people can take away a thing or two!

English