Sabitlenmiş Tweet

The Western Oil Buffer Has Not Moved. Yet.

I. The Headline Number Nobody Is Reading Correctly

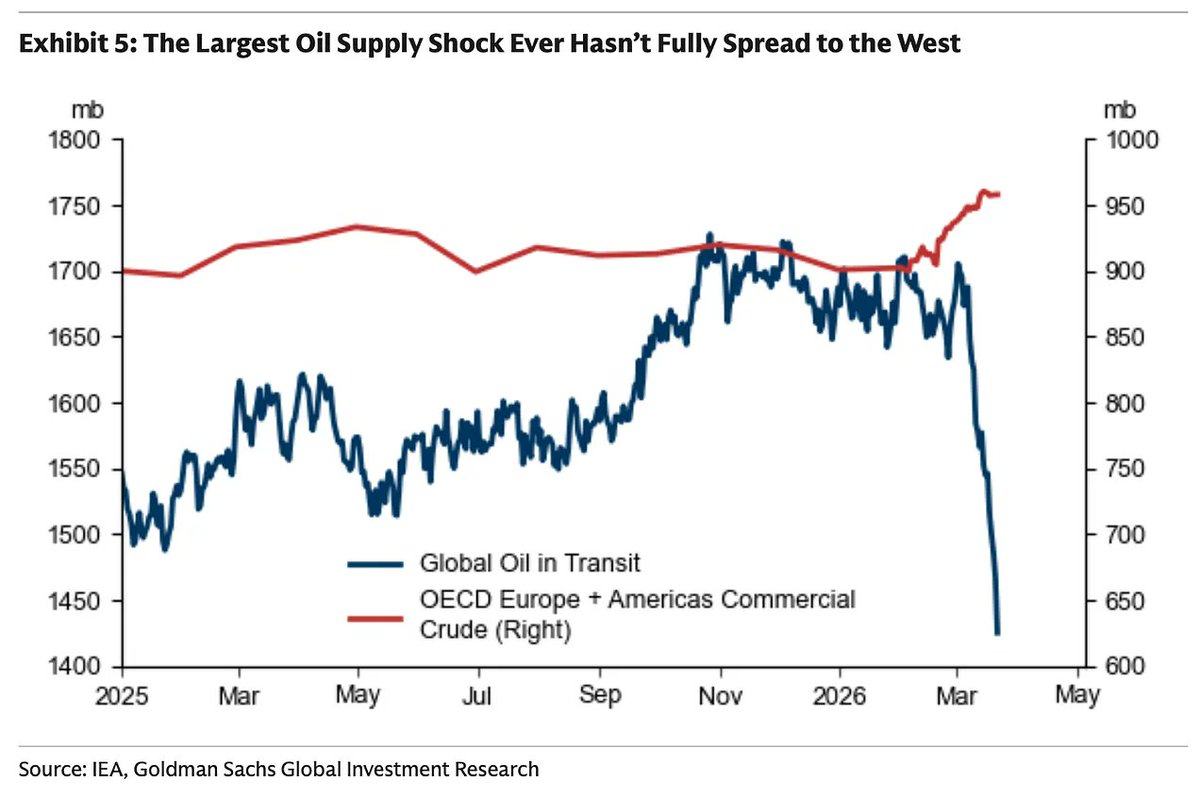

Hormuz has been effectively closed since February 28. The IEA called it the largest supply disruption in the history of the global oil market. And yet OECD commercial crude inventories have barely moved.

That is not evidence the market is fine. It is evidence of a lag that has not finished running.

II. What Actually Happened on February 28

Within 48 hours of Operation Epic Fury, the Strait of Hormuz went from 138 vessels per day to near zero. Maersk, CMA CGM, MSC and Hapag-Lloyd suspended transits the same night. P&I war risk insurance was cancelled from March 5, making the strait commercially unnavigable regardless of military conditions. The IRGC confirmed formal closure on March 2. By March 4, Iran claimed complete naval control of the passage.

On the same day, the Houthis announced they would resume attacks on Red Sea shipping. For the first time in modern history both major maritime corridors connecting the Gulf to Europe closed simultaneously. There is no Suez shortcut. There is no Gulf entry. The Cape of Good Hope is the only route.

III. Why The Inventory Line Has Not Moved

The 2025 supply surplus pre-loaded the system. The IEA reported global observed inventories at 8,210 million barrels in January 2026, the highest since February 2021. OECD countries held roughly half. Refineries were not drawing down storage because storage was full. Vessels that were mid-voyage when the closure hit delivered their cargo. That is why the OECD commercial stock line on every chart looks flat. It is not stability. It is the last shipments from a pipeline that stopped refilling five weeks ago.

IV. The Bypass Arithmetic

Alternative routes exist. Saudi Arabia's East-West Pipeline runs to Yanbu at up to 5 million barrels per day. The UAE's Abu Dhabi Crude Oil Pipeline delivers to Fujairah at 0.5 to 0.7 million barrels per day. Iraq's Kirkuk-Ceyhan pipeline moves crude to the Turkish Mediterranean coast. Combined capacity: 7 to 9 million barrels per day. Pre-closure Hormuz flow: 20 million barrels per day.

The gap is not temporary. The infrastructure was built to complement Hormuz, not replace it. More than 75% of spare OPEC+ production capacity sits behind the closed strait anyway, rendering it inaccessible regardless of willingness to pump.

V. The Sequencing Problem

The IEA coordinated emergency release of 400 million barrels is real supply. At 8 million barrels per day of lost crude flow it covers roughly 50 days. It is a bridge, not a solution. And the bridge has a far end.

If Hormuz reopens tomorrow - a generous assumption given where the three-way negotiation between Washington, Jerusalem and Tehran currently sits. The arithmetic of getting replacement cargo to Western Europe is still unforgiving.

Red Sea remains commercially closed. Houthis fired on Israel on March 28. No major carrier is transiting. Every cargo from the Gulf to Europe goes via Cape of Good Hope.

Gulf to Rotterdam: 30 to 36 days. Southern Europe: 25 to 30 days. UK: 32 to 38 days.

The strait has been closed five weeks. Six weeks of commercial inventory buffer already spent. The first post-reopening tanker that loads at Ras Tanura is still a month from Rotterdam. The inventory draw accelerates before that ship arrives. It does not reverse the moment it docks.

You cannot restock a refinery the day the tanker docks.

VI. What the Market Has and Has Not Priced

Markets have priced the reopening. Brent rallied on every ceasefire signal, every Trump statement, every hint of diplomatic movement. That is rational. Reopening removes the physical constraint.

What markets have not fully priced is the replenishment lag. The sequence is: closure ends, markets rally, first tanker loads, 30 days pass, cargo docks, refinery restocks, product supply normalises. Those events are separated by weeks at each step. Commercial inventories continue drawing through all of them.

The OECD stock line is flat today because the pre-loaded buffer is holding. When it starts moving it will not drift. It will drop. And it will drop while the market is already celebrating a reopening that has not yet translated into physical supply.

VII. The Unresolved Question

The ceasefire conversation has three variables that do not currently align. Washington wants a deal before the political cost becomes unmanageable. Israel wants permanent degradation of Iranian nuclear and military capability, not a pause. Iran wants Hormuz leverage as a negotiating chip, not a concession to be surrendered before talks begin.

None of those three positions has moved materially in five weeks.

IEA emergency stocks and OECD commercial buffers together provide roughly 100 to 120 days of theoretical coverage at current disruption rates. That is runway. But runway with a specific end point. And a negotiation that stalls past that end point enters territory no strategic reserve was designed for.

The buffer is real. The pipeline is broken. The lag is the story.

---

Sources: IEA Oil Market Report March 2026, EIA STEO March 2026, Wikipedia 2026 Strait of Hormuz crisis, Lloyd's List Intelligence, S&P Global, Argus Media, LSE Business Review, Congress. gov CRS report

For informational purposes only. Not financial or investment advice.

English