Asymmetrical Bets

30 posts

Asymmetrical Bets

@AsymmetricBets_

Join @MichaelSikand and @KawzInvests as they use thematic analysis and narrative driven alpha to find stocks with multibagger potential.

Katılım Kasım 2025

4 Takip Edilen304 Takipçiler

Asymmetrical Bets retweetledi

While the neocloud trade gets torched, $DOCN went the other way and ripped 10% today on record preliminary Q2 numbers.

$DOCN DigitalOcean doesn't just rent you the raw GPUs, it runs a full five-layer stack on top of them, infrastructure, core cloud, inference, data, and managed agents inside one platform, then steers customers up into the higher layers.

CEO Paddy Srinivasan said they "continue to extend our software advantage and further separate ourselves from bare-metal GPU rental companies."

A neocloud like $CRWV or $NBIS rents you the chip and leaves the wiring to you, so a customer who needs more than compute has nowhere to go but out.

$DOCN keeps them. RPO crossed $800M, up more than 10x year over year, and average contract life stretched from 1.6 years to over 3. AI ARR now comes primarily from managed services, not bare-metal rental, the layers a renter can't easily walk away from.

Bit salty they dropped this today, not gonna lie. Had the full breakdown queued up.

$DOCN has committed to over $1.9B in data center obligations, and gross margin already slipped from 61% to 56% as capex ran ahead of revenue. That only reverses when the new capacity fills.

If it fills, a platform where every agent consumes the whole stack instead of one rented layer collects a far bigger toll on each token.

Full deep dive breaking down the whole thesis is in the comments and pinned on my Substack in bio.

$DOCN $CRWV $NBIS

English

Asymmetrical Bets retweetledi

Good time to look at defense again after we lost to Belgium.

English

Asymmetrical Bets retweetledi

I'm already up 50% on my $SONY trade.

Stock is up 7% in 5 days, but recent IV expansion is boosting my calls as more sharps position around the GTA 6 thesis.

No matter how investors feel about AI, Sony keeps creeping up steadily every session.

Michael Sikand@michaelsikand

GTA VI will hit $1B in pre-orders in its first hour on sale today. But no one is looking at $SONY, the mispriced money printer on the biggest entertainment product in history. The trade on game publisher $TTWO has been priced in for a while. The highest street PT is 15% upside. The $GME upside is also light given the game is confirmed to have no discs. You see the world still looks at $SONY as a low margin console seller with a mature, memory shortage exposed product in PS5. But really, Sony is becoming a digital products business from PSN memberships and in-game purchases, a perfect set up around GTA 6. Despite being a diverse $115B conglomerate, it derives most of its revenue and profits from its video games business. $SONY is going to print high margin revenue alongside $TTWO, getting a cut of ~70% (console market share) of every game pre-order today, game purchase, and the in game economy purchases that still make $TTWO bags 13 years later. Sony’s own CFO said this point best: “The increase in operating income was mainly due to an increase in sales of add-on content and network services, as well as the impact of foreign exchange rates.” Plus there will be a massive flood in high margin new and re-activated PSN online memberships. Think about how many churned, non active PS5 owners will re-activate here for this game. You might think is this trade priced in because Sony recently guided for 30% earnings growth for their gaming business this fiscal year. However, almost of that earnings growth guided is from a large impairment $SONY took on its Bungie deal (Destiny publisher). So the organic growth from this once in a generation gaming catalyst is not baked in. To further support this "not priced in thesis", GTA's history of delays would make building guidance around it a risky play for management. Now you should know this thesis is not about console sales by the way. Memory shortages have forced Sony to hike PS5 prices, hurting demand. However, I believe the demand for GTA 6 is so asymmetrical, there will be major price inelasticity this holiday season, and PS5 will exceed sales targets anyway. It doesn't really matter though because the margins are very low on the hardware, the key is the console as a wedge into the high margin digital subscription and purchases revenue. Overall I love the R/R as the business is cheap here at 16x forward, down 20% year to date and down 50% from ATHs. I computed the base case at around $30 (50% upside) which aligns with other analysts like TD and BofA, so the company does look to be genuinley cheap. IV and expected move on options are super low, so I'm taking an options trade and you won't see Sony show up in any of my @joinautopilot strategies for this reason. Hope is that the market might begin to see what I do around this massive launch as more catalysts build and pre-order data drops. I've linked my free write up on Sony below or at link in bio.

English

Asymmetrical Bets retweetledi

same guy who asked $PENG about margin last earnings and they let slip how they've been stockpiling memory.

that was in april. memory price increases since then have been insane.

cheap chips in -> expensive CXL systems out = high margin

Asymmetrical Bets@AsymmetricBets_

$PENG just got its highest price target raise on Wall Street Rossenblatt Raises to $75 from $65 - Buy Analyst comments: "We are expecting Penguin Solutions to report a solid beat-and-raise for 2HF26. We expect the company's momentum in both its Advanced Computing and Integrated Memory product lines to accelerate going into 2HC26. For years, we have highlighted PENG shares as the best value in the AI market. In the past three months, investors have moved PENG's valuation from 6.7x to 22.6x forward earnings. We see this increase as justified by the AI market now needing the products and services Penguin provides.” For perspective we bought into $PENG back in May. Earnings could send another massive re-rate.

English

Asymmetrical Bets retweetledi

Be careful on $AAOI.

There's a crazy amount of resentment from institutions such as B. Riley who MISSED the stock and were bearish as low as $15.

Now making a massive intellectual leap on a nonsensical optical short thesis and literally name dropping $AAOI out of bitterness? Spite? For the virality?

You really can't make up the misinformation and FUD in photonics right now it's just unbelievable. Earnings should put everyone in their place very soon. Nothing has changed in the fact that there isn't enough photonics tech in the world today and won't be for years.

Everyone in my paid Substack + Discord knows I've been buying $AAOI all the way down from $160 in my trading portfolio, most recently loading at $114. I also increased $AAOI in my "Photonics Is Next" portfolio today.

No asymmetry without FUD - NAWF.

Stock Talk@stocktalkweekly

*B. RILEY SAYS AMAZON'S RNG & OPENAI'S MRC PROTOCOLS POSE MAJOR STRUCTURAL RISK FOR OPTICAL INFRASTRUCTURE / "PHOTONICS" STOCKS, NAMELY APPLIED OPTOELECTRONICS $AAOI Full comments: "Following the OFC conference in March 2025, the AI data center boom triggered an unprecedented optical supercycle. As demonstrated by the parabolic re-rating of optical infrastructure stocks such as Lumentum ($LITE – Buy, $1,142 PT ) and Coherent ($COHR – Neutral, $309 PT ), the prevailing investment thesis assumed an aggressive, compounding multiplier: scaling AI clusters meant building deeper, multi-tiered networks (3-tier or 4-tier Clos topologies), exponentially driving up transceiver demand per unit of compute. This thesis, however, is hitting a structural wall. Just a year after the 2025 explosion, the simultaneous market introduction of Amazon’s ($AMZN, NR) Resilient Network Graphs (RNG) and OpenAI’s Multipath Reliable Connection (MRC) protocol marks a major pivot toward network flattening across both training and inference workloads. Microsoft ($MSFT, NR) and Oracle ($ORCL, NR) are actively integrating the open-source MRC protocol into their frontier AI training supercomputing clusters—such as ORCL’s massive GB200 Abilene site—to execute sender-controlled packet spraying and bypass physical network bottlenecks. Concurrently, AMZN is deploying its quasi-random RNG architecture across its general-purpose cloud fabric. While RNG is isolated from back-end training clusters, it serves as the primary backbone for scale-out generative AI inference, data ingestion, and retrieval-augmented generation (RAG). Crucially, as mature AI models transition from training to mass inference, hyperscaler capex is shifting heavily in favor of these front-end, scale-out environments. Because RNG replaces traditional, active multi-tiered aggregation switches with passive optical ShuffleBoxes, it reduces active networking equipment by over 60%. Consequently, as AI workloads migrate to inference, this architectural deflation loops directly into the broader optical market, stripping out switch-to-switch optical links and dismantling the legacy transceiver-to-compute multiplier. For the transceiver market, this dual-front flattening represents a severe structural headwind that will sharply decelerate the sector's long-term TAM expansion, since these technologies reduce structural transceiver counts by 40% to 50%. We believe Applied Optoelectronics ($AAOI – Neutral, $129 PT) will be especially vulnerable to this development. AMZN and ORCL—the primary network provider to OpenAI—are expected to be the anchor customers for the 800G/1.6T transceivers forecast to drive AAOI's quarterly revenue to ~$1B by 2H27. As ORCL deflates training-cluster transceiver ratios via MRC, and AMZN strips active transceiver requirements from inference rollouts via RNG, AAOI's core revenue growth engines face massive structural risk."

English

Asymmetrical Bets retweetledi

$FLY is running $NVDA compute from the moon and down 53% since May?

Firefly has long been my favorite space stock and looks very attractive at $27/share ($4.5B MC).

One of its slept on superpowers is monetizing the vast data it collects, and this capability is being highlighted on the $NVDA blog.

Blue Ghost 1 sent home 120GB of raw lunar data that scientists are STILL processing a year later. NASA even issued a $10M follow on order to buy more data than they originally negotiated.

On Blue Ghost 2 this year, Firefly's Ocula imaging service runs $NVDA Jetson directly in lunar orbit. First time edge AI has ever operated around the moon.

Instead of dumping raw data down to Earth, Ocula runs the inference ON ORBIT and beams back only what the customer wants, in near real time.

Firefly's own SciTec AI software sits on top of the Jetson chain. Its Elytra spacecraft stays parked at the moon for a FIVE YEAR mission running it.

This is the high margin AI/software engine hiding inside a "space stock".

- Map landing sites for the next wave of lunar missions

- Detect minerals like ilmenite for future lunar energy

- Track objects and operations across cislunar space

Data processing in space feels like the near term opportunity for orbital AI until full on data centers get built there.

English

Asymmetrical Bets retweetledi

The whole thesis this year was AI kills every software stock. $RDDT did the opposite.

One of the few names that's actually profitable AND still growing fast

And the funny part is AI was supposed to be the threat. reddit pulled $311M in free cash flow on $1M of capex last quarter while google and openai burn hundreds of billions building the models that lean on reddit's data.

Now reddit's pushing to reprice those deals so it earns more as its content becomes more vital to AI answers, moving off the old flat fees. the disruptor became the customer. $RDDT $GOOGL $META

KawzInvests@KawzInvests

$RDDT trading at $140, down 50.6% from ATH of $283 despite strong fundamentals. Q4 2025 Metrics: Full-year revenue $2.2B, +69% YoY (57% 5-year CAGR) Q4 revenue $726M, +70% YoY Q4 adj. EBITDA margin: 45% (Rule of 115 company) Full-year gross margin: 91.2% Forward P/E: 31.2 (trailing: 53.3) Full-year FCF $684M, +3x YoY ARPU +42% to $5.98 Company initiated $1B buyback on $2.48B cash. Q1 2026 guidance: $595M-$605M revenue, 53% YoY growth at midpoint. CEO Steve Huffman: "Reddit is at the center of a once-in-a-generation shift...more people are turning to Reddit because Reddit is the most human place on the internet." While $META $GOOGL trade near highs, SaaS/growth tech selloff created opportunity in profitable, high-margin social platform. Six consecutive quarters of 60%+ revenue growth. Business expanding while valuation compressed 51% from peak.

English

Asymmetrical Bets retweetledi

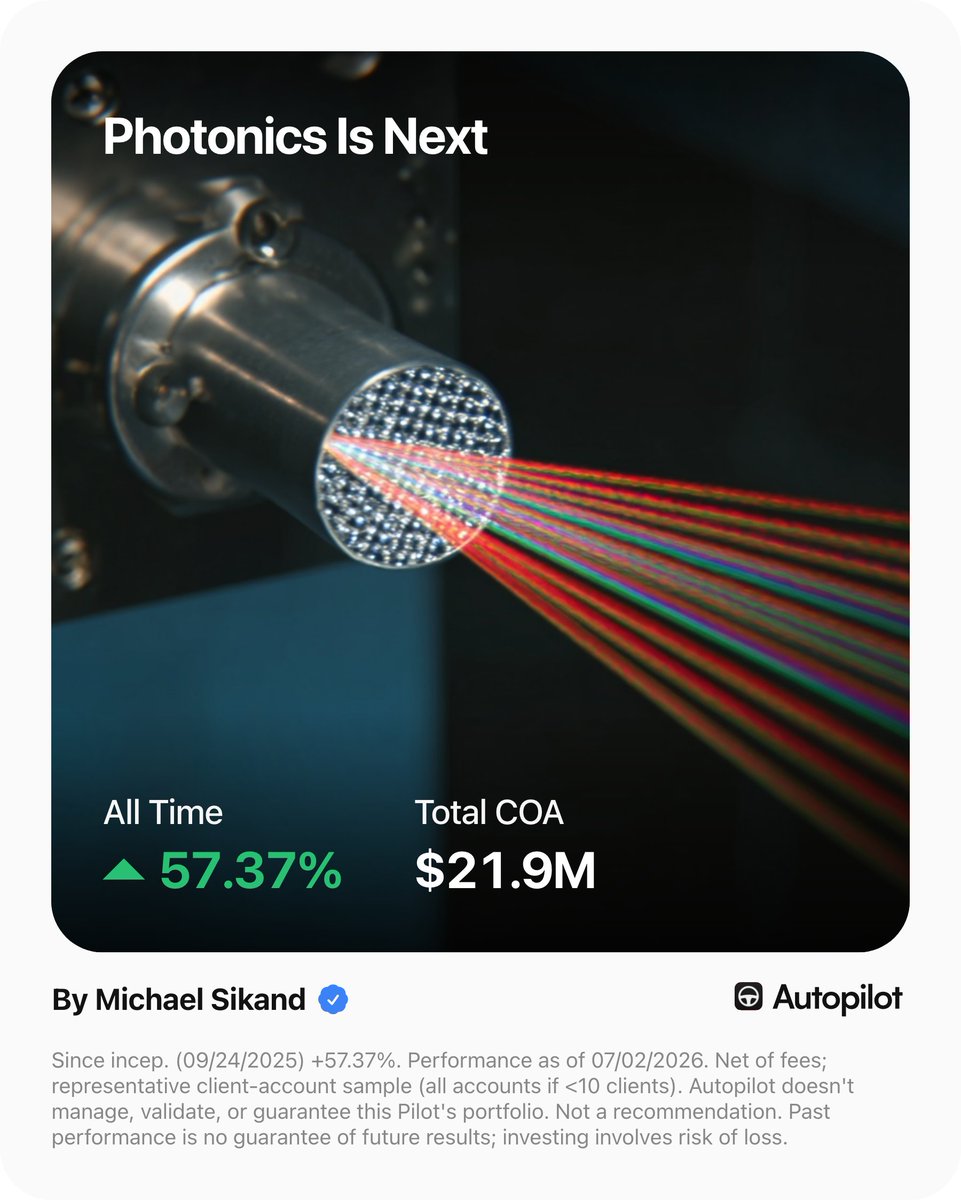

$20M trade update.

I just updated my "Photonics Is Next" AI infra portfolio on @joinautopilot followed by 3300+ U.S. retail investors and $21.9M in connected assets as of 7/6.

This portfolio, which is also overseen by my partner @KawzInvests, has been a major part of the rise in my profile as an investor.

On 6/2, my optical basket peaked at 123.5% all-time returns, achieving those gains in under 6 months, as computed by Autopilot's software. For context, the fund achieved this return holding a diverse basket of stocks, an incredible outcome for retail investors passively following.

I'm extremely proud of our work on this product. There exists no optical ETF currently for retail investors despite a rush by issuers to cash in on the hype. My picks were launched back in February, providing retail investors a 6 month window to front run the category and get staked into the next AI bottleneck without the complexity of individual stock picking.

Despite the recent sell off, the portfolio is still up 45% year to date, roughly 4.5x the S&P 500.

$LAZR and $LYTE are two ETFs going to launch soon by major players, which should attract billions in AUM. However, I believe my allocations are superior and that my picks will outperform them with lower fees.

So where are we now? Recently, the optical sector has gotten slammed based in my view mainly on sentiment, institutional profit taking, and disputed rumors from a well-known research firm on delays to next-gen architecture. Photonics Is Next is down 29.6% in the last month and 16.8% in just the last week.

That's why I think it's the perfect time to re-balance, add more weight to higher conviction positions, and add one brand new position I missed earlier on.

This rebalance today adds Corning ($GLW) as a new 10.00% position. Down 13% in five days. Now anchored by three hyperscale relationships (a 10x-capacity NVIDIA partnership, a Meta deal worth up to $6B, and a multi billion dollar Amazon agreement).

Three names get boosted: AAOI (12.30%→15.00%), LITE (14.75%→15.00%), and AEHR (4.26%→5.00%).

Six positions are trimmed: TSEM (11.11%→10.00%), COHR (16.07%→15.00%), AXTI (8.58%→5.00%), CIEN (11.39%→10.00%), MRVL (11.11%→5.00%), and VIAV (10.43%→10.00%).

For catalysts that could create upside, I'm watching:

- Hyperscale Capex Guides In Upcoming Earnings

- Earnings From All Optical Names In The Basket Particularly $COHR $LITE $AAOI

- The launch of mainstream optical ETFs $LAZR and $LYTE

$GLW $AAOI $LITE $AEHR $TSEM $COHR $AXTI $CIEN $MRVL $VIAV

--

See link in comments to follow the portfolio using the Autopilot app. Pay attention to disclaimers on the image of this post and the Autopilot app.

English

$PENG just got its highest price target raise on Wall Street

Rossenblatt Raises to $75 from $65 - Buy

Analyst comments:

"We are expecting Penguin Solutions to report a solid beat-and-raise for 2HF26. We expect the company's momentum in both its Advanced Computing and Integrated Memory product lines to accelerate going into 2HC26. For years, we have highlighted PENG shares as the best value in the AI market. In the past three months, investors have moved PENG's valuation from 6.7x to 22.6x forward earnings. We see this increase as justified by the AI market now needing the products and services Penguin provides.”

For perspective we bought into $PENG back in May. Earnings could send another massive re-rate.

Michael Sikand@michaelsikand

I just bought $2M of a brand new stock after it crashed 7% today. $PENG is now a 20% position in my Asymmetrical Bets fund (+89% YTD) on @joinautopilot followed by $10M. Credit goes to legend @pennycheck for being the first to call this stock. With Penguin Solutions I now own the winner agnostic integrator behind the memory, CPU, and photonics supercycle at under 17x forward earnings. 1) The memory business alone is worth the market cap. Penguin's Integrated Memory biz = they take raw DRAM chips from manufacturers like SK Hynix and package them into custom memory modules built to spec for AI servers, telco gear, and enterprise systems. It's now 50% of revenue, did $172M last quarter, growing 63% YoY, ~$800M annualized. Apply a 3x price to sales on just this unit and you're already above what $PENG is worth today. 2) Play the CPU supercycle. CPU:GPU ratios going from 1:8 to 1:1 as agentic AI takes over. $PENG is the lead integration partner for AMD EPYC and Intel Xeon. Every new socket = more memory cooling and integration revenue baked in. 3) The AI Factory platform is real. OriginAI is their turnkey deployment from 256 to 16,000+ GPU clusters for sovereign and enterprise customers. 85,000 GPUs already deployed. UBS says non hyperscaler buyers (sovereigns, neoclouds, enterprises) capture 48% of AI infra spend in 2026. Hyperscalers build in house. But these other players ALL need Penguin. 4) Photonics is the unpriced asymmetric bet. $PENG called photonics early and was an early investor in Celestial AI. $MRVL acquired it $3.25B in December. Now Penguin is building the Photonic Memory Appliance, making it the only public play on this kind of wild photonics tech. The PMA is basically a box that uses light to link memory across a bunch of servers so the entire AI cluster can share one giant pool of memory like it's one big computer. Marvell guides Celestial to $1B revenue in 2029. If Penguin captures even low double digits of that stream, that could be 9 figs of unpriced networking revenue on $PENG's highest margin, most defensible IP. 5) People/partners are cracked. Chairman of $PENG is ALSO Chairman of $LITE. AMD CTO Mark Papermaster sits on the board SK Telecom dropped $200M as a strategic investor New CPO Ian Colle ran AI infra at AWS 6) Risks are real but manageable Penguin's AI cluster business is lumpy and one big customer slipping a quarter can tank earnings (already happened in Q2, down 42% YoY). The memory shortage is a headwind as high DRAM prices are slowing customer orders and hitting Penguin's gross margins. The photonics upside is a 2027+ story, so if it slips, the stock can sit dead money for a while. Because the multiple is still so cheap, I overall see limited downside compared to the upside if their photonics option can be quantified with $MRVL where I could see Penguin trading closer to a 30x+ forward PE. Surf's up. Full thesis linked on Substack below.

English

Humanoid robots are taking off with Agility’s $CCXI SPAC debut already up 80%+ and lifting the whole robotics sector.

But the same bottleneck sits inside of these robots too: Memory.

A high-autonomy vehicle already needs 300GB+ DRAM. Humanoids need 10x that.

$MU CEO says they have no line of sight on supply catching demand.

Sold out, rationing customers and all the pricing power.

Robot makers will battle for market share. Memory suppliers get paid no matter who wins.

But there’s another layer many people forget about. The software such as QNX, which is the safety critical brain powering robots. Already in surgical systems, industrial arms, and next-gen humanoids with $NVDA, and $BB owns it all. Checkout the full article linked below.

English

Asymmetrical Bets retweetledi

275 million vehicles run on software almost no one can name. The same software runs 9 of 10 medical device makers and 8 of 10 surgical robotics platforms.

It is QNX, and it is a division of $BB.

Last quarter it did $72.3M, up 25.7% YoY at 86% gross margin, now 47.3% of the entire company.

The verticals it already owns

> Automotive, 10 of 10 top automakers and 24 of 25 top EV makers

> Commercial vehicles, all five top tier 1 suppliers

> Medical devices, 9 of 10 makers and 8 of 10 surgical robotics platforms

> Robotics, 300+ programs at a 100% production deadline record

> Rail, 300M+ mission critical systems deployed

> Defense, NATO, 17 of the G20, and NASA flight software

The silicon under QNX reads like the entire AI compute stack. $NVDA, $QCOM, $NXPI, $INTC and $TXN plus Renesas all run QNX in their ecosystems.

Wrote the full deep dive on BlackBerry's Hidden Physical AI Play in the comments and pinned to my bio.

$BB $NVDA $QCOM

English

Asymmetrical Bets retweetledi

If you want to catch the next multi-bagger you best be patient and expect the idea to fall on deaf ears.

English

Asymmetrical Bets retweetledi

I've been posting about $SONY for a GTA VI re-rate.

But did you know it's also a god tier robotics long.

$SONY built a robot that defeats human ping pong pros.

It's called Ace. Sony AI trained it purely in simulation, no human footage. It reacts in 20ms vs 230ms for a pro, and this year it took down a top 25 world ranked player under official ITTF rules. This is the same lab that beat also Gran Turismo world champions in 2022.

Every robot, every car, every phone camera needs eyes. $SONY makes the eyes. The company is world #1 in image sensors for years running.

Image sensors are ~17% of conglomerate revenue

But ~25% of operating profit

Record ~$2.2B last year, up 29%.

Then last month they signed a JV with TSMC to build next gen image sensors in Japan. Sony holds the controlling stake. The stated target? Physical AI.

The best foundry on earth is now co-building Sony's sensors for the exact wave Ace is a preview of.

So the market prices $SONY as a memory constrained game console maker at ~16x forward earnings, down ~17% on the year and 50% from November alone.

What you're getting is 50% of the market in the eyes for robotics, and a near pure margin cut on 7/10 GTA copies sold until PC enters the mix.

English

Asymmetrical Bets retweetledi

SemiAnalysis guys after crashing photonics and buying back 40% off.

Serenity@aleabitoreddit

Be SemiAnalysis: - Post a scathing piece on CPO delays + optical company valuations, causing a crash. Which $NVDA, analyst desks, and major optical companies refuted - Launch an institutional photonics ETF after optical names dropped 40-60%.

English

Americas birthday is in two days and you’re bearish on defense?

$AVAV $AVEX $KTOS

Michael Sikand@michaelsikand

Wow I really called the bottom on defense huh? $AVAV is surging 14.5% today on a $500M contract from the U.S. Department of Defense for counter-unmanned aerial systems. The stock is up 39% in just 5 sessions. This follows a blockbuster earnings report with a big beat on EPS and revenue. Funded backlog now $1.2B, up from $727M a year ago. Note: $AVAV is the largest position in my defense themed "Modern Warfare" on @joinautopilot, finally flipping green up 16% now since my original entry.

English

Asymmetrical Bets retweetledi

English

Hegseth appointed Marc Andreessen to the Pentagon's Defense Policy Board.

We just published a piece calling the bottom on defense stocks and this appointment is exactly the kind of signal that supports the thesis.

A16z holds positions in Anduril, Skydio, Shield AI, Saronic, and Applied Intuition. Anduril alone just took a $20B Army enterprise agreement in March, the deal that pushed its valuation to $61 billion. The same venture network that's spent years arguing the Pentagon should buy more commercial autonomy and software from startups instead of legacy primes.

Now one of its loudest voices sits on the board that advises Pentagon leadership on force structure and modernization.

This is the same dynamic playing out across our entire drone and counter drone basket. FY2027 budget requests $53.6B for Drone Dominance and $20.6B for counter-UAS.

Jamie Dimon is reportedly pushing $10B into firms essential for national security. Defense sentiment is at a low while the budget tailwind is accelerating.

Andreessen's appointment is a confirmation of where the policy and capital are both heading.

full breakdown of our top defense and drone picks in the article. link below.

Asymmetrical Bets@AsymmetricBets_

On Monday, we made $AVAV the largest position in our defense portfolio, it's up ~ 40% since. After their earnings, we officially called the bottom on defense. Yesterday the Pentagon awarded AeroVironment a $500M counter-UAS contract. $AVAV is up 15%+ on the news with our other favorites following such as $AVEX +10%. The money is flowing exactly where we said it would. Thesis playing out in real time.

English